Value Rotation Goes Global As Alibaba’s Singles Day Gains +38% to $56B of Goods Sold

5 Min. Read Time

Upcoming Events

We will be hosting a webinar today, November 11th at 11:00am EST.

Ant Group’s Future and Singles Day 2020 Recap

Happy Veterans Day in a hat tip to all that have served and sacrificed on our behalf. Thank you!

The State Administration for Market Regulation announced an examination of internet monopolies, which sounds eerily similar to the Congress’ move calling US tech CEOs a few months back. US and Hong Kong stocks have fallen dramatically, which is exacerbated by the recent vaccine-led rebound in old economy sectors at the cost of new economy sectors. The Ant Group IPO being pulled is not helping. Analysts have started to chime in on the potential for regulation, though we’ve seen no price target changes nor any downgrades. The proposed draft is going to target exclusivity issues that the bigger players (Tencent and Alibaba) force on their ecosystems. Want to use Tencent’s WePay on Alibaba’s Tmall e-commerce platform? No dice. Merchants who want to sell on Alibaba are not allowed to sell on rivals JD.com and Pinduoduo. This reminds me when Google was forced to allow access to other search engines such as Microsoft’s Bing. To paraphrase Milton Friedman, we are free to choose Bing, but it does not change the reality that it is an inferior product to Google search. Disallowing the exclusivity rules makes sense to me, but it isn’t going to stop great companies from being great companies. Who agrees with me? Institutional investors in China. Today was one of the biggest buy day of Hong Kong stocks in Southbound Connect history led by volume leaders Tencent and Meituan Dianping. Tencent had 7 to 2 buyers while Meituan 2 to 1 buyers. Did you see that Alibaba sold over $56B during Singles Day today? That’s 38% more than last year! Amazing. Another thought as all governments care about employment: Alibaba has 122,399 employees and Tencent has 70,756. Today is actually Tencent’s 22nd anniversary. I’m a buyer for what this company and its peers can do in the next 22 years!

The rotation into value/cyclical plays from growth/tech continues, though I’m skeptical in the medium-term/long-term. Remember when Trump was elected? US financial stocks ripped higher on deregulation. People funded the buying of financial stocks by selling their tech holdings. The trend lasted for a good four months before investors realized banks don’t grow as fast compared to tech companies. The value/growth disparity is very stretched as the rubber band is snapping back as investors buy YTD underperformers in a “dash for trash”. The value comeback requires a flawless vaccine introduction and everything “back to normal”. I hope this happens! I can’t ignore what I see around me, which is the northeast heading back into tighter quarantine rules. This latest “trash dash” is apt to be powerful and could last some time. From studying China, which is two quarters out of quarantine, the growth names delivered on earnings though many sectors didn’t come back as strongly. Confirmation will be over the next week as Chinese internet companies report Q3 earnings. On deck is Pinduoduo, which reports tomorrow morning.

Key News

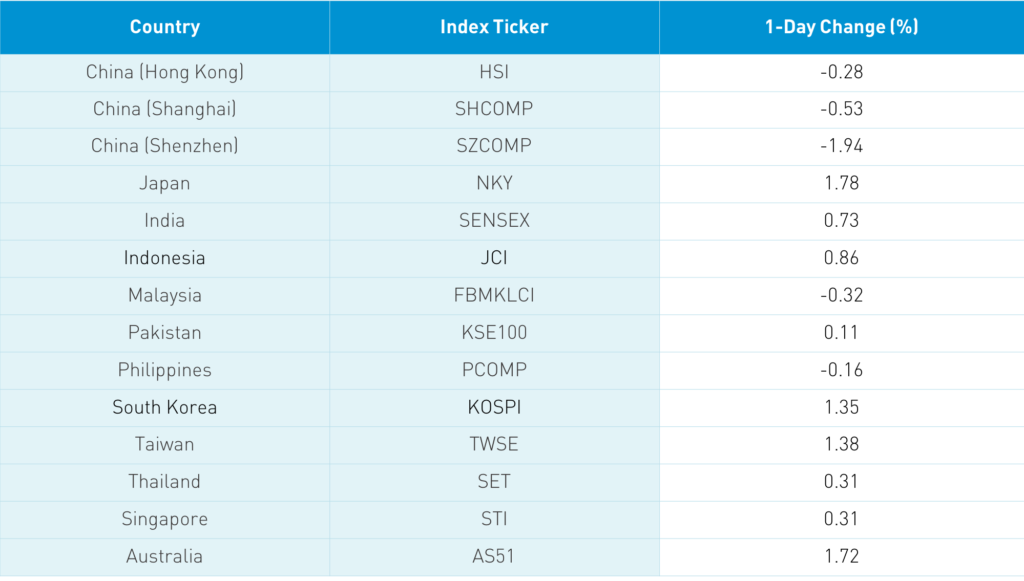

Asian equities were largely higher on high volumes as the value/cyclical rotation plays out globally. For instance, the Kospi rose +1.35% while the Kosdaq fell -0.11%, and Shanghai (value) was off modestly -0.53% while Shenzhen (growth) fell -1.94%. Hong Kong slipped into the close, but value sectors outperformed handily versus growth sectors. Hong Kong volume leaders were Tencent, which fell -7.39%, Alibaba Hong Kong, which was off -9.8%, Meituan Dianping, which was down -9.67%, Ping An Insurance, which rose +1.7%, Xiaomi, which fell -8.18%, JD.com Hong Kong, which was off -9.2%, BYD, which dropped -14.91%, AIA, which was flat at 0.0%, HSBC, which rose +4.11%, China Construction Bank, which was up +3.17%, and Hong Kong Exchanges, which dropped -3.99%. YTD winners were all clocked for YTD underperformers as evidenced by automaker BYD which was off and Hong Kong Exchanges which reported strong financial results mid-day. Didn’t matter! I do find that the Southbound Connect buying of Tencent and Meituan as clues that the ferocity of the rotation may have gone too far too fast. Shanghai & Shenzhen were off as tech/growth sectors hit harder. Foreign investors were buyers of Shanghai stocks while sellers of Shenzhen stocks. CNY was stable overnight.

MSCI released its pro-forma for the month end Semi-Annual Index Review. While China’s numerical count of stocks rose from 715 to 722 within MSCI Emerging Markets, the percentage declined from 42.4% to 42.1%. Pretty much every EM country saw a percentage decline due to Kuwait’s upgrade from Frontier Markets to EM as seven stocks are included with a country weight of 0.6%. We also see an expansion of India’s Foreign Ownership Limits, which raised the country’s weight from 8.3% to 9.1%. Two previously designated Hong Kong domiciled stocks, which are considered part of development markets, were reclassified as Chinese stocks. I would think that other companies want to follow suit.

Online video companies Huya and DouYu both reported Q3 financial results this morning. In a nutshell, both were a touch light on revenue, but beat on net income. Deep dive mañana!

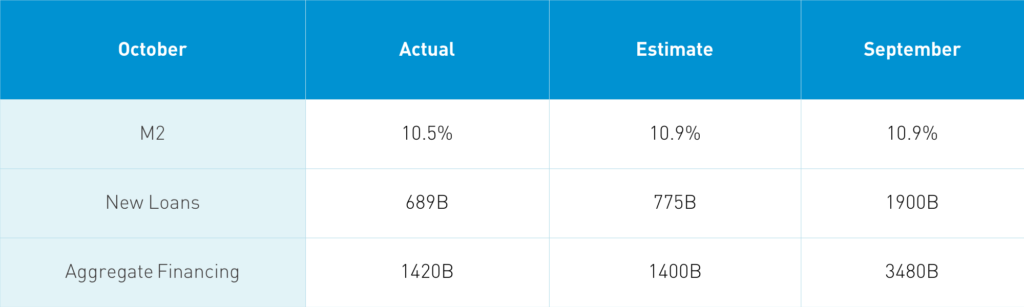

Takeaway: The release occurred after the Mainland close though no one focused on it. Aggregate financing was strong, which is a positive. Loan growth cuts both ways since it’s that good debt levels aren’t rising too quickly. However, it could be concerning that access for companies struggling post-quarantine aren’t receiving adequate support.

Tencent Music Entertainment (TME US) released Q3 financial results post the US close yesterday. The results look good to me as the company exceeded analyst expectations across the board.

- Revenues rose +16.4% to $1.12B (RMB 7.58B) versus estimate RMB 7.48B

- Mobile Online Music MAU fell -2.3% to 646mm

- Paying Online Music Users rose +46% to 51.7mm

- Cost of Revenues rose +19.1% to $362mm (RMB 2.46B)

- Gross Margin 32.4%, which is -1.6%

- Adjusted Net Income $198mm (RMB 1.35B) versus estimate 1.187B

- Adjust EPS $.012 (RMB 0.80) versus estimate RMB 0.71

H-Share Update

The Hang Seng bounced around the room to close off -0.28%/-74 index points at 26,226. Volume increased 14% from yesterday, which is 227% of the 1-year average while breadth was positive with 33 advancers and 15 decliners. The Chinese companies within the MSCI China All Shares Index fell -2.62%, with utilities up +4.16%, energy +3.93%, real estate +3.49%, materials +3.32%, and financials +2.39%, while discretionary was off -8.49%, communication -5.93%, tech -5.14%, health care -2.84%, and staples -1.33%. Southbound Connect volumes were very high. Mainland investors bought $1.195B of Hong Kong stocks today as Southbound trading accounted for 10% of Hong Kong turnover.

A-Share Update

Shanghai & Shenzhen slid into the close off -0.53% and -1.94% at 3,342 and 2,263 respectively as volume fell -11% from yesterday, which is 107% of the 1-year average. Breadth was off with 1,100 advancers and 2,232 decliners. The 518 Mainland stocks within the MSCI China All Shares Index dropped -1.47%, led by real estate +0.98%, utilities +0.79%, and energy +0.68%, while tech was off -3.82%, health care -2.78%, discretionary -2.59%, communication -2.21%, industrials -1.05%, staples -0.99%, and financials -0.54%. Northbound Stock Connect volumes were moderate/high as foreign investors sold -$140mm of Mainland stocks as Northbound Connect trading accounted for 5.8% of Mainland turnover.

Last Night's Exchange Rates & Yields

- CNY/USD 6.63 versus 6.62

- CNY/EUR 7.79 versus 7.82 yesterday

- Yield on 1-Day Government Bond 1.91% versus 1.91% yesterday

- Yield on 10-Year Government Bond 3.24% versus 3.22% yesterday

- Yield on 10-Year China Development Bank Bond 3.71% versus 3.70% yesterday