JD.com Reports Q3, October Industrial Production & Retail Sales, Asia Trade Deal RCEP Signed

3 Min. Read Time

Key News

The Regional Comprehensive Economic Partnership (RCEP) was signed over the weekend by ten countries including China, Japan, South Korea, Australia, Indonesia and Thailand. The agreement removes tariffs on goods sold between the countries. The jury is out on the economic impact though it reminded me of the Thunderbird School of Management’s motto from Dr. William Lytle Schurz: “Borders frequented by trade seldom need soldiers.” The countries represent approximately 1/3 of the world’s GDP and population. India did not participate as some speculate it views China’s manufacturing as a rival.

We continue to monitor the situation on the Executive Order banning US investors from investing in 31 Chinese companies. It is worth noting most of the companies are private. The most notable company is China Mobile, which is listed in Hong Kong and the US. I believe a lawsuit will be filed challenging the order, similar to what we saw with TikTok. A legal challenge could postpone the January 11th deadline until after Biden’s January 20th inauguration. At that point, Biden will unwind the Executive Order. Logistically speaking, the order is without precedent as to what happens to the China Mobile ADR. This was very similar to last night’s 60 Minutes coverage of Tik Tok as no evidence was given that the Chinese government has access to user data outside of China. Where is the evidence? It is a bizarre world where you can make unsubstantiated claims that are taken as gospel.

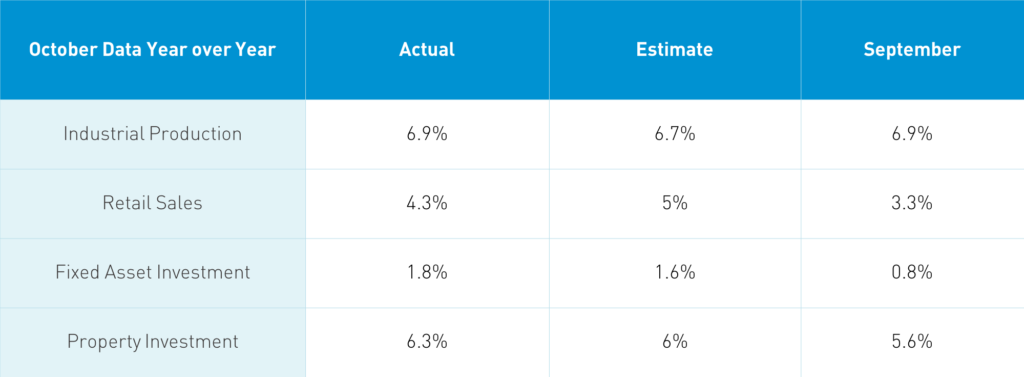

Takeaway: Copper’s 2% gain tells you everything you need to know about the Industrial Production release. Looking at the product level data, one segment that jumped out was autos as motor vehicles +11.1%, cars +7.5% and EV +94.1%. The retail sales data supported this as auto sales rose +12%. The restaurant category finally entered into positive territory at +0.8%. All in all, a solid release that helps explain an element of the market’s strong performance today.

E-commerce giant JD.com reported strong Q3 results that beat analyst expectations across the board before the US market open. These are very good results, but they had to be as JD’s stock is up +161% year-to-date as of Friday. There was also broker chatter that JD’s user data indicated that rival Pinduoduo was taking market share. The company reported that JD Health has submitted its information pack to the Hong Kong Exchange in preparation for a listing.

- Revenue +29.2% to $25.7B (RMB 174.2B) versus estimate RMB 174B

- Active customers +32.1% to 441mm from 334mm

- Adjusted Net Income +80.1% to $800mm (RMB 5.6B) versus estimate RMB 4.217B

- Adjusted EPS $0.50 (RMB 3.42) versus estimate RMB 2.72

- Cash $18.7B (RMB 126.7B)

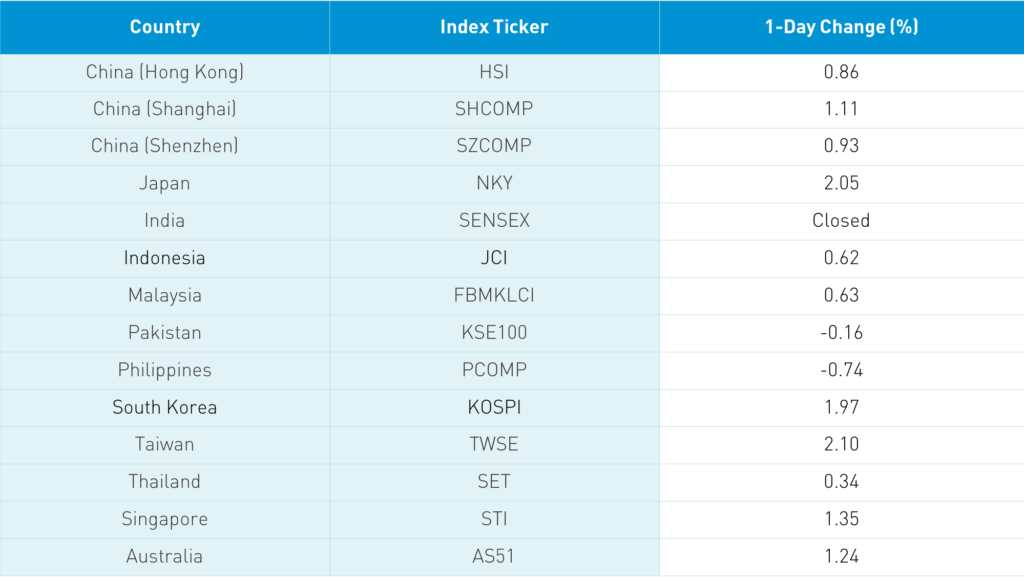

Asian equities gained today on nice volumes as the RCEP and China economic release lifted sentiment across the region. The Hang Seng gained +0.86% led by Hong Kong volume leaders Tencent, which fell -0.83%, Alibaba HK, which fell -1.17%, Meituan Dianping, which gained +4.12%, China Mobile, which fell -3.7%, Xiaomi, which gained +3.92%, JD.com HK, which gained +5.63%, and BYD, which fell -1.15%. We also saw a bit more of the value catch up overnight. Macau casino stocks performed well as the market is anticipating the easing of travel restrictions. Mainland China had a strong night with Shanghai +1.11% and Shenzhen +0.93% in a broad rally today. CNY rallied back below the 6.60 level to 6.58.

H-Share Update

The Hang Seng ended near the day’s high +0.86%/+2224 index points at 26,381. Volume was off -4% from Friday though still at 121% of the 1-year average while breadth was positive with 31 advancers and 17 decliners. The 204 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index gained +0.47% led by materials +4.17%, discretionary +3.15%, tech +2.17%, energy +1.68%, staples +1.22% and health care +1.14%. Laggards were communication -1.1% and real estate -2.17%. Southbound Stock Connect volumes were moderate/light as Mainland investors bought $279 million worth of Hong Kong stocks as Southbound trading accounted for 10.7% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen went from the lower left to the upper right to close +1.11% and +0.93% at 3,346 and 2,289, respectively. Volume was up +10.5% from Friday though 99% off the 1-year average. Breadth was positive with 2,610 advancers and 1,168 decliners. The 518 Mainland-listed Chinese companies within the MSCI China All Shares Index gained +1.44% led by materials +4.08%, energy +3.09%, staples +2.63%, financials +1.38%, health care +1.37%, industrials +1.31%, real estate +1.31%, and communication +1.11%. Tech and discretionary lagged, falling -0.24% and -0.17%, respectively. Foreign investors bought $393 million worth of Mainland stocks today as Northbound Connect trading accounted for 6.7% of Mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.58 versus 6.61 Friday

- CNY/EUR 7.79 versus 7.81 Friday

- Yield on 1-Day Government Bond 1.73% versus 2.00% Friday

- Yield on 10-Year Government Bond 3.27% versus 3.27% Friday

- Yield on 10-Year China Development Bank Bond 3.71% versus 3.72% Friday