Hong Kong Investors Shrug Off Yesterday’s Growth Selloff

4 Min. Read Time

Key News

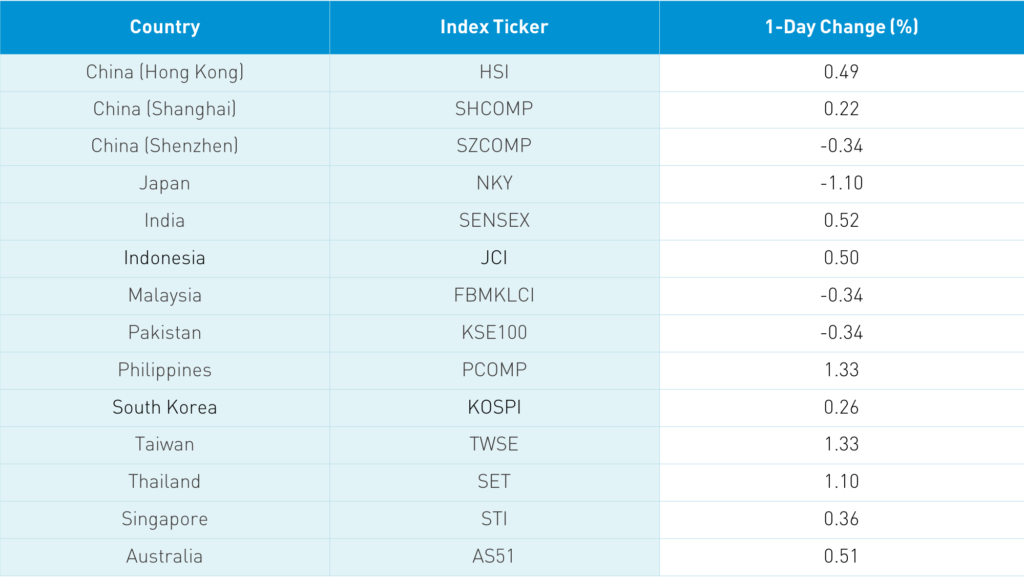

Asian equities had a mixed night and largely shook off yesterday's growth selloff in the US. Japan was an outlier to the downside while Taiwan was an outlier to the upside. The Hang Seng Index gained +0.49%, led by volume leader Tencent, which gained +1.29%, as Southbound Connect buying continues. Meanwhile, Meituan Dianping, which has been seeing selling via Southbound Connect after it was announced that the stock will be included in the index, fell -0.99%, Alibaba HK gained +0.08%, Ping An Insurance gained +1.54%, AIA gained +0.73%, Geely Auto gained +6.87%, JD.com HK fell -0.53% despite several analyst price target upgrades, China Mobile fell -0.74%, Xiaomi fell -0.41%, and BYD gained +3.64%.

It is worth noting that Asian investors mostly shook off the Wall Street Journal article stating that the SEC would push ahead with rules requiring US-listed Chinese companies to submit their audit papers to the PCAOB or face delisting in 2022. Why the shoulder shrug? The Journal notes that SEC Chair Jay Clayton is leaving at year end, which means that the drafting and implementation of the rules would fall under a Biden SEC head. Additionally, a more communicative approach to China under a Biden administration could see the issue resolved. I did some digging and found that last July the SFC, Hong Kong’s regulator, signed an agreement with the CSRC, the mainland regulator, and the Ministry of Finance to allow it to inspect the audit papers of Chinese companies listed in Hong Kong. It doesn’t appear to have been implemented as of yet, but it provides a path for compliance as many US-listed Chinese companies are also listed in Hong Kong.

Mainland China was mixed as the Shanghai Composite gained +0.22% led by brokerage firms and the financial sector while Shenzhen was off a touch, -0.34%. The value/growth disparity has become a global phenomenon, though, in the case of post-quarantine China, the economic data shows a broadening in the recovery as cyclical stocks play catch-up. To fund that the catch-up, growth names are being sold as evidenced by the fact that ChiNext, a growth index of mainly mid and small caps, was off -1.41% overnight.

There have been a few notable defaults in China’s bond market recently, but there is really very little to worry as China’s bond market has a value in the trillions of dollars versus a few hundred million dollars of defaults. CNY depreciated slightly versus the USD, as the exchange rates fell -0.08% to 6.5623 from yesterday’s 6.5568. I noted the wide disparity between US-listed Chinese companies, which were down, and CNH, which appreciated, on Twitter yesterday. (For intra-day updates I can be followed at @ahern_brendan.)

Yesterday I wasted two hours watching SEC Chair Jay Clayton’s testimony to the US Senate Committee on Banking, Housing and Urban Affairs. I was hoping for some clarity on the unprecedented Executive Order barring US investors from investing in 13 Chinese stocks listed in the US, Hong Kong, and Mainland China. What is going to happen to China Mobile’s ADR listed here in the US? Will foreigners still be able to access it while Americans cannot? Unfortunately, China didn’t come up at all! Clayton’s prepared 29-page statement does mention the President’s Working Group (PWG) paper titled “Significant Risks from Chinese Companies” from back in July. It states “I welcome congressional action to address these issues” outlined by the PWG paper, but that is it. How do you not address this? After watching two Senators absolutely rip into Clayton on various issues, I suppose one has to commend him for his service to our country though I am sure he is excited to get back into private practice.

A future positive pivot in US-China relations may also be driven by the China side as the country prepares for the 2022 Beijing Winter Olympics. The reality is that the last thing China wants is a boycott of the Olympics driven by any number of issues. This is pure speculation on my part, but the rationale behind it makes sense.

A Mainland media source noted that prestigious private equity/hedge fund Hillhouse Capital increased its allocation to healthcare in Q3. According to the Yicai article, it also increased investments in Chinese electric vehicle companies. It always feels good to be on the same side of smart investors such as Hillhouse.

Pinduoduo (PDD US) announced that it will be issuing $1.75 billion worth of convertible notes and 28.7 million new shares to be sold at $125. Yesterday’s close was $132 million, which is apt to put some pressure on the stock. Regardless of the short-term pressure, investors are apt to stay focused on the company after its strong Q3 results, the highlight of which was the +89% increase in revenue year over year.

Online streamer Bilibili (BILI US) will report after the close today in the US.

H-Share Update

The Hang Seng rallied in the afternoon +0.49%/+129 index points to close at 26,544. Volume was -6.8% from yesterday which is 105% of the 1-year average while breadth was positive with 30 advancers and 17 decliners. The 204 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index gained +0.78% with staples +1.5%, real estate +1.26%, communication +1.08%, financials 1% and discretionary +0.81% while heath care -0.54%, utilities -0.48% and energy -0.24%. Southbound Stock Connect flows were light/moderate as Mainland investors bought $232 million worth of Hong Kong stocks today. Southbound Connect trading accounted for 9.8% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen bounced around the room to close +0.22% and -0.34% at 3,347 and 2,261, respectively. Volume was off -4% from yesterday, which is 101% of the 1-year average while breadth was positive with 2,206 advancers and 1,473 decliners. The 518 Mainland stocks within the MSCI China All Shares Index fell -0.16% with financials +1.64% and real estate +0.99%. Meanwhile, health care -1.3%, staples -0.94%, -0.92% and tech -0.66%. Northbound Stock Connect volumes were moderate as foreign investors sold -$2 million worth of Mainland stocks. Northbound Connect trading accounted for 6.1% of Mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.56 versus 6.56 yesterday

- CNY/EUR 7.79 versus 7.78 yesterday

- Yield on 1-Day Government Bond 1.40% versus 1.50% yesterday

- Yield on 10-Year Government Bond 3.32% versus 3.29% yesterday

- Yield on 10-Year China Development Bank Bond 3.74% versus 3.72% yesterday