Bilibili Q3 Gets Jiggy, JOYY Goes On the Offensive

5 Min. Read Time

Upcoming Events

Sign up for KraneShares Model Portfolios to view our next webinar: Insights in Action – Asset Class Specialization in Emerging Markets and China is the Key to Differentiated Returns on Tuesday, December 1st, 11:00 am – 12:00 pm EST.

Click here to register!Key News

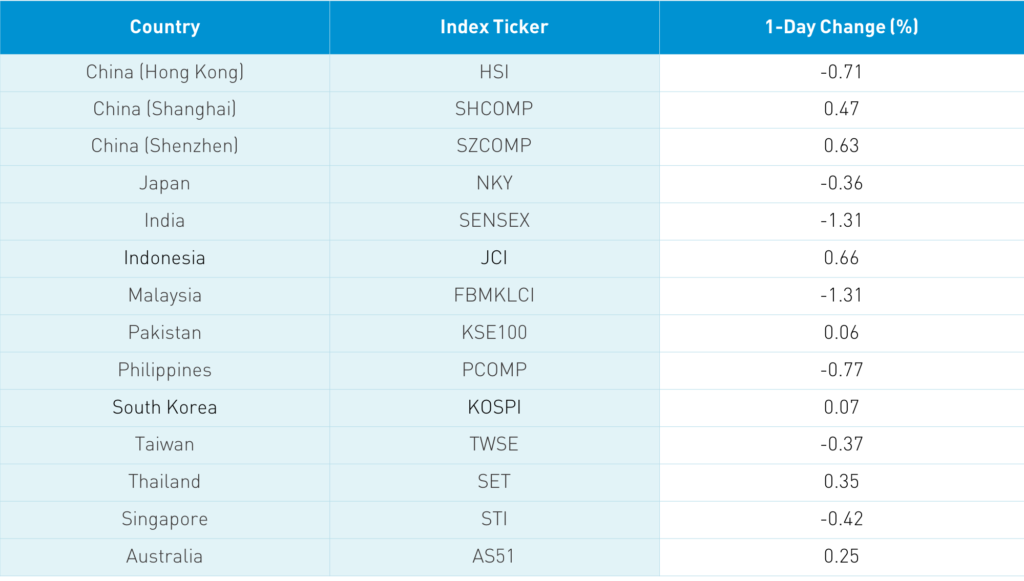

Asian markets had a mixed performance as coronavirus cases appear to be rising globally, weighing on sentiment against the backdrop of vaccine hopes and implementation timelines. The Hang Seng was off -0.71%, while the broader Hang Seng Composite was off -0.68%. Hong Kong volume leaders were Tencent, which fell -2.72% despite another round of Mainland buying Stock Connect, Meituan Dianping, which was off -2%, Xiaomi, which rose +5%, Alibaba Hong Kong, which dropped -1.92%, Geely Auto, which gained +0.44%, real estate management spin-off Sunac IPOed, which was up +21.9% and AIA, which was off -1.84%.

Internet names were off after yesterday’s sell-off in the US after a short-selling firm accused JOYY (YY) of fraud following Baidu’s (BIDU US) proposed acquisition of the company’s Chinese online streaming business. JOYY’s stock was hit falling -26% yesterday, though analysts are skeptical of the allegations and defending the company. YY had previously sold Tencent its HUYA business line, which raises skepticism on the allegations. Additionally, the company issued a press release refuting the claims this morning and announced that it will step up its stock purchase plan. If one looks at YY’s independent and audit board members, they have impressive resumes leading to skepticism on my part. It is a good thing that short-selling firms are out there to keep fraudsters at bay, though this allegation doesn’t appear to have merit.

Mainland China had a stronger day with Shanghai up +0.47% and Shenzhen up +0.63%. The primary driver was the news of Premier Li’s speech on China’s “dual circulation” policy. The first circulation was global -focused, while the second circulation will be nationally-focused, emphasizing raised domestic consumption. Tea leave readers drove up the prices of home appliances and automakers as they are favored sectors. Home appliance makers Midea gained +5.27%, Gree rose +1.81% and Haier was up +3.52%. EV maker BYD was off -3.22%, though many traditional auto-plays were up.

Healthcare had a decent day on coronavirus flare-ups, though Mainland media sources noted five Chinese vaccines are in Phase 3 trials in China and also the UAE, Brazil, Pakistan, and Peru. The South China Morning Post noted that 1mm Chinese citizens have taken Sinopharm’s vaccine. Wow! Brokers were off on news that the regulator was examining a broker that issued a bond from a company that defaulted. China’s bond market sold off overnight as credit spreads widened though this looks like a heck of an entry point for medium/long term investors.

I am politically agnostic as it isn’t what we are paid to do, though politics have been thrust upon investors. I think we can all agree this administration is not going quietly into the night. We have not seen a legal challenge to last week’s Executive Order on banning US investors from investing in companies' alleged ties (without evidence I should point out) to the Chinese military. A legal challenge could kick the enforcement deadline into a Biden administration. A rule forcing Chinese companies to release their audit books is likely coming. The companies should comply with the global standard, though doing so at the cost of $2 trillion of US investors’ savings seems like the wrong approach. No one wants to see the companies delist. I would suspect that the audit issue gets taken care of under the Biden administration. Of course, the issue could be put to bed if the Chinese law that prevents the companies from sharing their audit books was removed. I don’t Tweet often but for intra-day updates, I can be followed at @ahern_brendan.

Remember that Hong Kong represents what foreigners are thinking while Mainland China represents what the Chinese think of China. Rising coronavirus cases are a global issue though not in China. It could be interesting to see if the Mainland can ride out a downdraft.

There is chatter that JD.com’s spin-off, JD Health, could see a first week of December Hong Kong listing.

Online streamer/entertainment platform Bilibili (BILI US) reported after the US close yesterday. If there is a company that makes me feel old and out of touch, it is Bilibili. It is similar to Twitch, which allows viewers to watch other people play video games, but also focused on anime/comic book-like characters. The problem is not the company just Father Time’s effect as the company delivered outstanding topline growth, which beat analyst estimates. Costs, unfortunately, increased at a higher rate though investors are apt to give the company a bit of a pass it is a growing company trying to grab market share as evidenced by the user growth data.

- Revenue +74% to $475mm (RMB 3.225B) versus estimate RMB 3.064B

- Average Monthly Users +54% to 197mm; Daily Average Users +42% to 53mm; Paying Users +89% to

- Cost of revenues +63% to $362mm (RMB 2.464B)

- Gross profit +117% to $112mm (RMB 761B)

- Total Operating Expenses +138% to $271mm (RMB 1.844B)

- Adjusted Net Loss -$145mm (RMB -990mm) versus estimate RMB -901mm

- Adjusted EPS Loss -$0.41 (RMB 2.76) versus estimate RMB 2.45

- Q4 Revenue forecast between RMB 3.6B and 3.7B

This morning online gaming company NetEase (NTES US) reported Q3 financial results that beat to the upside, though expenses related to growing the business took a bite out of the bottom line.

- Revenue +27.5% to $2.7B (RMB 18.7B) versus estimate RMB 18.1B

- Gross Profit +25.6% to $1.5B (RMB 9.9B)

- Operating Expenses +54.7% to $1B (RMB 7B)

- Adjusted Net Income $540mm (RMB 3.7B) versus estimate 2.15B

- Adjusted EPS $0.16 (RMB 1.07) versus estimate RMB 2.62

- Announced a dividend

H-Share Update

The Hang Seng opened lower and stayed there off -0.71%/-187 index points at 26,356. Volume was off -1.3% from yesterday, which is 109% of the 1-year average while breadth was off with 14 advancers and 33 decliners. The 204 Chinese companies listed in Hong Kong within the MSCI China All Shares Index were off -1.19%, led by staples, which gained +1.54%, tech +0.56%, and healthcare +0.05%, while communication was off -2.39%, materials -2.37%, industrials -1.33%, financials -1.32%, and real estate -1.13%. Southbound Stock Connect volumes were light as Mainland investors bought $362mm of Hong Kong shares today as Southbound trading accounted for 9.4% of Hong Kong turnover.

A-Share Update

Shanghai & Shenzhen opened lower but grinded higher all day closing up +0.47% and +0.63% at 3,363 and 2,275 respectively. Volume was off -5.6% from yesterday, which is 95% of the 1-year average while breadth was positive with 2,012 advancers and 1,660 decliners. The 518 Chinese companies within the MSCI China All Shares Index gained +0.05%, led by tech +0.47%, staples +0.45%, and healthcare +0.29%, while materials -1.31%, energy -1.02%, and utilities -0.59%. Northbound Stock Connect volumes were moderate with Mainland investors buying $66mm of Mainland stocks as Northbound trading accounted for 5.5% of Mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.58 versus 6.56 yesterday

- CNY/EUR 7.80 versus 7.79 yesterday

- Yield on 1-Day Government Bond 1.50% versus 1.40% yesterday

- Yield on 10-Year Government Bond 3.35% versus 3.32% yesterday

- Yield on 10-Year China Development Bank Bond 3.35% versus 3.32% yesterday