Southbound Connect Expansion Will Not Include Dual Share Classes, Value Rotation Goes Global

3 Min. Read Time

Upcoming Events

Sign up for KraneShares Model Portfolios to view our next webinar: Insights in Action – Asset Class Specialization in Emerging Markets and China is the Key to Differentiated Returns on Tuesday, December 1st, 11:00 am – 12:00 pm EST.

Click here to register!Key News

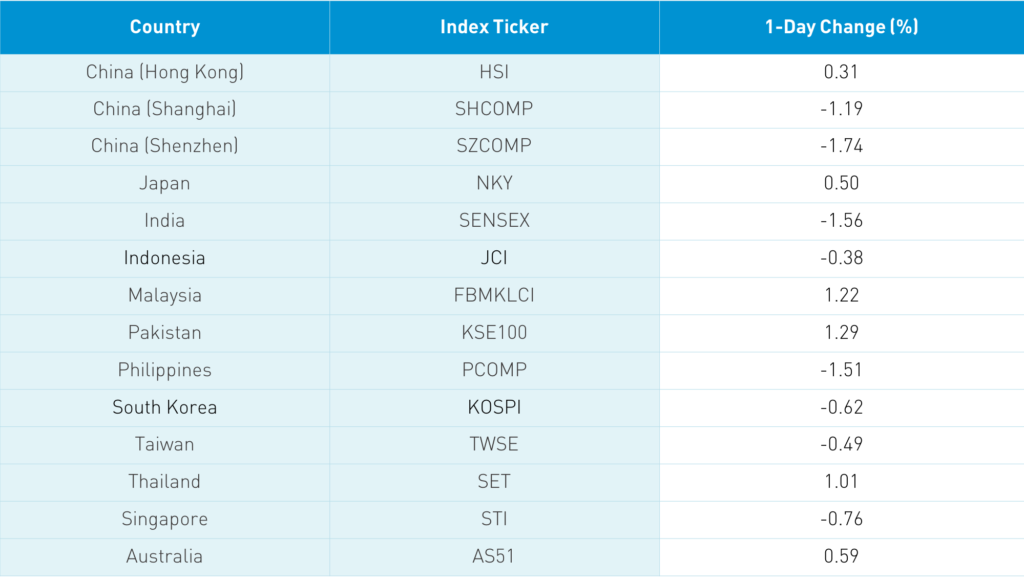

Asian equities seemed to question US stock euphoria in light of rising global coronavirus cases as markets were off on high volumes. High volume days are important clues on what big investors are thinking as these investors utilize them to shift their portfolios. What did today tell us? The value catch trade is a global phenomenon just as the growth outperformance over the last decade has been a global phenomenon. The 50 stock Hang Seng Index was up today masking an ugly day as the 400+ stock Hang Seng Composite was down -0.69% and the Chinese companies listed in Hong Kong within the MSCI China All Shares Index were down -1.36%. A significant driver of growth stock weakness was Carrie Lam’s financial reform speech that didn’t include Hong Kong dual share classes becoming part of Connect as the market anticipated. No Bueno! STAR Board stocks will be added to Northbound Connect while biotech stocks will be added to Southbound Connect. Helping value stocks are rumors that HSBC’s dividend could be reinstated.

Hong Kong volume leaders were Tencent, which fell -1.88% and had a rare selling day by Mainland investors via Southbound Connect, Xiaomi, which was off -3.68%, Alibaba Hong Kong, which dropped -1.11%, Meituan, which fell -3.23%, Ping An, which rose +2%, HSBC, which gained +6.54%, Hong Kong Exchanges, which fell -2.3%, BYD, which was off -3.55% and AIA, which rose +0.74%. Shanghai and Shenzhen were off -1.19% and -1.74% respectively despite Premier Li’s positive statements about the economy during the “1+6” Roundtable with the World Bank, WTO, OECD, Financial Stability Board, and IMF. Not helping growth stocks was India increasing the number of banned Chinese apps, including Alibaba’s international e-commerce unit. Growth names and YTD outperformers, which tend to be mid and small caps, were off on profit-taking. Concerns that President Trump will not go gentle into the night had technology stocks off on concerns that the technology ban could be expanded. A smaller EV player is falling under regulator scrutiny, leading to all things auto being taken to the woodshed on profit-taking. Foreign investors got in on the value rotation with net buying of Shanghai stocks while Shenzhen stocks were sold for an outflow of -$238mm via Northbound Connect. CNY was stable overnight.

JD.com Hong Kong was off overnight despite progress on its JD Health spin-off IPO making progress. The company will sell 381mm shares between HKD 62.80 and HKD 70.58, which would raise around HKD 3.5B. The company has lined up several prestigious investors according to Bloomberg including PE/HF giant Hillhouse, Singapore sovereign wealth fund GIC, and BlackRock. The company is expected to list next week or the week after.

H-Share Update

The Hang Seng came off the day’s high closing up +0.31%/+81 index points at 26,669. Volume surged +24% from yesterday, which is 145% of the 1-year average. Breadth was positive with 30 advancers and 18 decliners. The 204 Chinese companies listed in Hong Kong within the MSCI China All Shares Index fell by -1.36%, led by energy +2.96% and financials +1.11%, while materials fell -3.95%, discretionary -3.36%, staples -3.08%, healthcare -2.73%, tech -2.62%, and industrials -1.69%. Southbound Connect volumes were moderate/high as Mainland investors bought $89mm of Hong Kong stocks as Southbound Connect trading accounted for 10.4% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen opened higher but slid the entire day, closing -1.19% and -1.74% at 3,362 and 2,254 respectively. Volume was up +4% from yesterday, which is 105% of the 1-year average. Breadth was awful with only 729 advancers and 3,052 decliners. The 518 Mainland stocks within the MSCI China All Shares Index fell by-1.56%, led lower by materials, -3.02%, staples -2.56%, healthcare -2.4%, industrials -1.97%, communication -1.79%, and discretionary -1.03%. Northbound Stock volumes were moderate as foreign investors sold -$238mm of Mainland stocks as Northbound Connect trading accounted for 5.9% of Mainland turnover.

Last Night's Exchange Rates, Prices, & Yields

- CNY/USD 6.58 versus 6.59 yesterday

- CNY/EUR 7.83 versus 7.82 yesterday

- Yield on 1-Day Government Bond 1.10% versus 1.30% yesterday

- Yield on 10-Year Government Bond 3.27% versus 3.29% yesterday

- Yield on 10-Year China Development Bank Bond 3.74% versus 3.77% yesterday