MSCI Index Rebalance Drives Volumes, Meituan & Autohome Deliver Strong Q3 Results

4 Min. Read Time

Upcoming Events

Sign up for KraneShares Model Portfolios to view our next webinar: Insights in Action – Asset Class Specialization in Emerging Markets and China is the Key to Differentiated Returns Tomorrow, December 1st, 11:00 am – 12:00 pm EST.

Click here to register!Key News

Asian markets ended a strong month with a thud as volumes exploded due to trading related to MSCI’s Semi-Annual Index Review (SAIR). The SAIR is one of two big rebalance days as companies are added and deleted and market capitalization-based weights are adjusted. However, we should take today’s market action with a grain of salt because passive investors sold only to match index changes. The MSCI-driven adjustments came as Hong Kong’s volume rose to double the 1-year average. Hong Kong stocks within the MSCI Emerging Markets Index were adjusted down due to the upgrade of Kuwait to Emerging Markets from Frontier Markets and an increase in India’s weight.

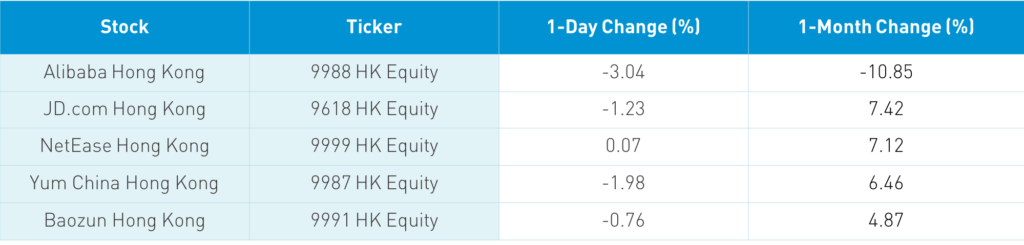

The Hang Seng drifted lower -2.06% despite a positive PMI release. Increased Hong Kong coronavirus cases led to expanded social distancing measures, spooking some investors. Reuters reported that Chinese energy giant CNOOC, which fell -13.97% overnight in Hong Kong, and Semiconductor Manufacturing (SMIC), which fell -2.7% overnight in Hong Kong, could both be added to Trump’s investment ban for US investors as the administration forces policies on Biden. Hong Kong volume leaders were Tencent, which fell -3.43%, Meituan, which fell -7.05% ahead of its Q3 earnings release, which occurred after market close, Ping An, which was off -0.76%, Xiaomi, which was up +1.73% as the company may benefit from Huawei’s misfortunes, China Construction Bank, which was off -0.33, Alibaba HK, which fell -3.04% on rumors that the chances of an Ant Group IPO in 2021 remain dim, and ICBC, which gained +1.03%.

Unsurprisingly, health care stocks were one of the few bright spots today. The Mainland was off a touch with Shanghai and Shenzhen down by -0.49% and -0.15%, respectively, as the PBOC injected liquidity into the banking system. Northbound Stock Connect trading was 2X the normal amount, driven by MSCI flows which led to a purchase of $750 million worth of Mainland stock purchases. Mid and small caps held up better than large caps today. Chinese bonds rallied today while CNY was stable.

It has been rumored that the House could vote Wednesday on the bill that would require US-listed Chinese companies to provide their audit books to the PCAOB or face delisting in two/three years. This long running issue has festered for seven years as the two sides are unable to find a middle ground. We do not know whether the lame duck session will take up the vote considering SEC Chairman James Clayton will retire at the end of the year. Some may prefer to see the decision deferred to the incoming Biden administration. US-listed Chinese companies should absolutely adhere to the global standard of allowing the PCAOB to view the auditor’s notes. However, playing chicken with $2 trillion worth of US investors’ savings is nonsensical. Nonetheless, even if the measure passes the SEC has provided a path to a resolution by allowing the Big Four auditors to verify the work of their Mainland subsidiaries. While hard liners have made it difficult to negotiate and find a resolution, a Biden administration presents an opportunity for a middle ground to be reached. That could be one reason the House eventually decides to push the issue to next year. No one wants to see US investors hurt by an issue beyond their control, which is why few believe the companies will be delisted.

Meituan (3690 HK) reported after the close in Hong Kong today. The results came in strong, beating analyst expectations as the company’s core food delivery business thrived. Remember that China is two full quarters post-quarantine. This is another indication that habits formed during quarantine are sticking. Percentage changes are year-over-year (Q3 2020 versus Q3 2019).

- Revenue +28.8% to $5.385B (RMB 35.401B) versus estimate RMB 34.047B

- Gross Transaction Value of Food delivery +36% to RMB 152.2B

- Daily average number of food deliveries +30.1% to 34.9mm

- Operating margin increased to 19% from 5.3%

- Adjusted EBITDA $406mm (RMB 2.675B) versus estimate RMB 1.99B

- Adjusted Net Profit $312mm (RMB 2.054B) versus estimate RMB 1.053B

- Profit $961mm (RMB 6.321B) from RMB 1.333 in Q3 2019

Online car sales company Autohome (ATHM US) also reported before the US market open this morning.

- Revenues $341mm (RMB 2.315B) from Q3 2019’s RMB 2.170B

- Operating Profit $109mm (RMB 744mm) from Q3 2019’s RMB 640mm

- Net Income $129mm (RMB 847mm) from Q3 2019’s RMB 643mm

- EPS $1.04 (RMB 7.09) versus analyst estimate RMB 6.49 and Q3 2019’s RMB 5.43

- Q4 revenue forecast $364mm to $365mm

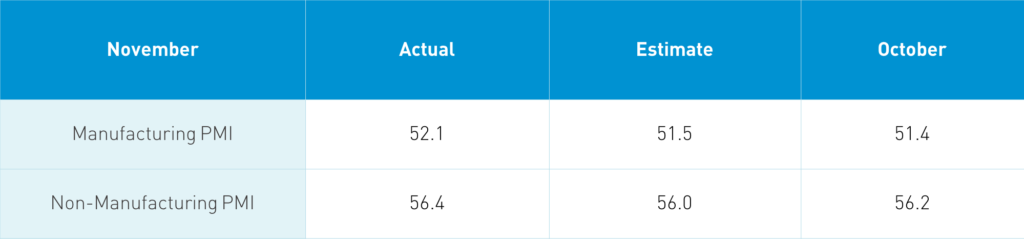

Takeaway: Today’s “official” PMIs are further evidence of China’s V-shaped recovery. However, the strong release had no noticeable market impact.

H-Share Update

The Hang Seng slid south at the open to end up closing down by -2.06%/-553 index points at 26,341. Volume jumped +113% from Friday, which is 195% of the 1-year average, while breadth was awful with five advancers and 44 decliners. The 204 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index fell -2.51% with health care +1.02% and tech +0.45%. Meanwhile, energy -9.34%, discretionary -4.98%, communication -3.29%, staple -2.08% and industrials -1.68%. Southbound Stock Connect volumes were elevated as Mainland investors bought $644 million worth of Hong Kong stocks and Southbound trading accounted for 7.8% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen slid in the afternoon to close -0.49% and -0.15% at 3,391 and 2,249, respectively. Volume increased +31% from Friday, which is 114% of the 1-year average though breadth was off with 1,430 advancers and 2,262 decliners. The 518 Mainland Chinese companies within the MSCI China All Shares Index fell -0.34% with communication +2.03%, tech +0.61%, and health care +0.33%. Meanwhile, staples were off -1.74%, utilities -0.86% and real estate -0.86%. Northbound Stock Connect volumes were high as foreign investors bought $750 million worth of Mainland stocks today and Northbound Connect trading accounted for 10.6% of Mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.58 versus 6.58 Friday

- CNY/EUR 7.88 versus 7.86 Friday

- Yield on 1-Day Government Bond 1.20% versus 0.88% Friday

- Yield on 10-Year Government Bond 3.25% versus 3.30% Friday

- Yield on 10-Year China Development Bank Bond 3.70% versus 3.75% Friday