More Bark Than Bite: SEC Provides Resolution to PCAOB Issue Despite House’s Delisting Vote

5 Min. Read Time

The House will vote today on a bill that will require US regulators to review the audit books of US-listed Chinese companies or face delisting if they do not come into compliance within three years. While headlines around this bill have emphasized the potential delisting component, they have not highlighted the substantial progress the SEC has made in providing a framework for resolving the issue. Based on the President’s Working Group on Financial Markets, the SEC recently proposed allowing a “co-audit” in which the US auditors of Chinese companies listed in the United States, with whom the SEC has a long-term working relationship, would be able to validate their Mainland subsidiaries’ work.

There is speculation that the SEC's proposal could have been developed in cooperation with their Chinese counterpart, the CSRC, in order to resolve the long-running issue that Chinese law does not allow US-listed Chinese companies’ audit books to be reviewed by the Public Company Accounting Oversight Board (PCAOB), which is a US regulator that sets accounting and reporting standards for publicly-traded companies.

The vast majority of US-listed Chinese companies are audited by the "Big Four" US accounting firms: PWC, Deloitte, Ernst & Young, and KPMG. While skeptics may question the quality of the audit work done by these firms, the Big Four apply the same auditing methodology in China as they do in the US, Europe, and the rest of the world.

It is critical to note that enforcement of the law will be handled by the SEC, which is likely to follow the guidelines outlined during the working group. There are over $2 trillion in US savings invested in US-listed Chinese companies such as Alibaba, Baidu, and JD.com. While it is important to ensure these companies are following PCAOB standards, we believe the SEC is likely to do so in a measured and transparent manner to protect shareholders. Furthermore, a wholesale delisting could jeopardize the US’ status as the world’s financial center.

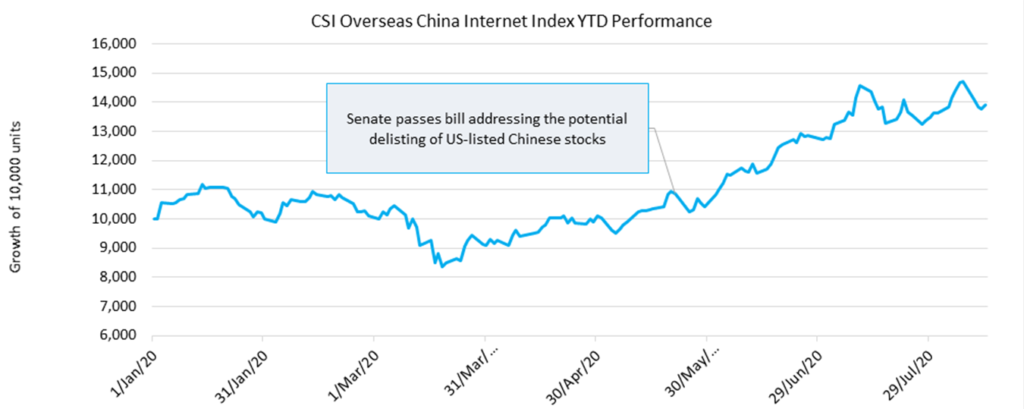

Yesterday, US-listed Chinese companies were weak though our measure of political risk CNH, China’s currency that trades during US trading hours, was up! This is a rare event! As we have written numerous times, it is always a good idea to check CNH before making any trade based on headlines as stocks are far more volatile than China’s currency. Time and time again, headlines can lead to stock volatility that that is not validated by CNH. We saw this earlier this year when the Senate passed its delisting bill. Stocks went down, but only temporarily!

There has been significant emphasis placed on the risk associated with investing in Chinese equities and little examination of the rewards. We believe the aggregate rewards associated with investing in many of these companies may outweigh the unfortunate “bad apples”. Many would be surprised to learn that NetEase, a US-listed Chinese gaming company that listed back on June 29, 2000, has returned 13,335% since its IPO versus Amazon’s 8,573% return. Alibaba alone has generated hundreds of billions of dollars for its shareholders.

One reason I am constructive on a positive outcome from the PCAOB bill is that numerous new Chinese companies have listed in the US in 2020 including Beike and Lufax Holdings. Clearly these companies and their investment banks believe that de-listing is unlikely.

Additionally, there has been a positive change in Chinese regulators’ tone on this issue. On November 20th, a CSRC spokesperson was asked by a reporter at a press briefing about this issue. The spokesperson noted that “Chinese companies listed on U.S. stock exchanges follow U.S. laws and regulations for financial reporting and information disclosure. Otherwise, their securities cannot be registered with the U.S. regulatory authorities.” The spokesperson then stated “On 4 August 2020, after thoroughly considering the concerns of the U.S. regulators, the CSRC sent the fourth version of the proposal for joint inspection over audit firms to the U.S. Public Company Accounting Oversight Board (PCAOB). The PCAOB confirmed the receipt of the proposal and suggested that it would examine the proposal in due course. We look forward to starting a meaningful dialogue with the U.S. regulator on the details of the proposal.”

Key News

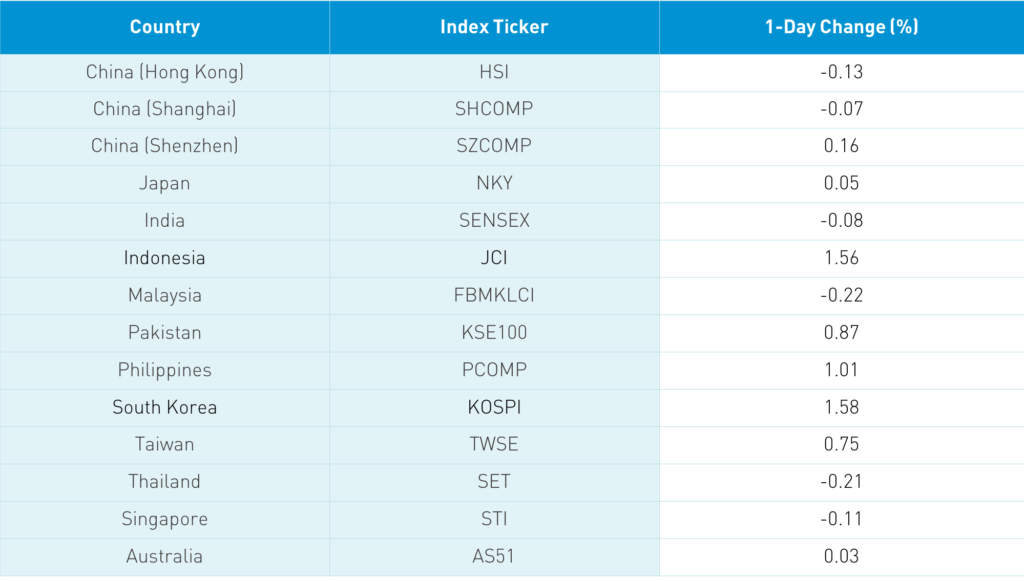

Asian equities had a lackluster night with Korea, Indonesia, and the Philippines outperforming. The news that President Elect Biden will not immediately eliminate tariffs did not come as a surprise to anyone. Meanwhile, growth investors had to raise cash for next week’s JD Health IPO, which led to value outperforming at the expense of growth.

The Hang Seng Index had a choppy session falling -0.13%. However, it was worse than it appeared as the broader Hang Seng Composite fell -0.62% and the Hong Kong-listed Chinese stocks within the MSCI China All Shares Index fell -1%. Xiaomi closed -7% on massive volume as it was almost 4X the next most heavily traded stock after announcing a 1 billion share issuance though came off its low of -11%. Mainland investors were significant buyers on today’s weakness via Southbound Connect trading. Some are questioning why Xiaomi is raising cash since it has so much on its balance sheet already. Meituan was off -3.94% following its earnings release, though I see the sell side coming to the rescue in defending the stock. On Friday, Meituan is being added to the Hang Seng Index so those puking up the stock today will likely be buying Friday. Other volume leaders were Tencent, which fell -0.69%, Ping An Insurance, which gained +0.8%, Alibaba HK, which fell -0.78%, BYD, which fell -7.89% after announcing a new share issuance, Geely, which fell -4.16%, and HSBC, which gained +3.66%.

The value rotation in Hong Kong was mirrored on the Mainland. Shanghai pulled a James Bond falling -0.07% while Shenzhen gained +0.16%. Construction equipment maker Zoomlion +9.98% as you need a way to get that copper out of the ground. Appliance makers had a good day with Gree +3.47% and Midea +2.26%. Several growth sectors saw profit taking such as auto/EV and solar names. Foreign investors sold -$613 million worth of Mainland stocks via Northbound Connect though it is worth noting the big inflows Monday and Tuesday. CNY appreciated slightly versus the US $ to 6.56 from 6.57.

Reports are saying that JD Health will list on December 8th.

It is funny to see Meituan weakness as the stock will be added to the Hang Seng Index on Friday at a 5% weight.

Online travel company Trip.com (TCOM US, formerly C-Trip.com) reported after the US close yesterday. While the company’s financials have been ravaged by coronavirus in the year over year comparisons, the company did experience a sharp uptick quarter over quarter. The company noted that the China domestic travel company actually achieved positive year over year growth in Q3.

- Revenue declined -48% to $805mm (RMB 5.5B) versus analyst estimate of RMB 5.211B

- Worth noting that revenue +73% increase from Q2 2020

- Sales & Marketing Expenses declined -54% while General & Administrative Expenses declined by 38%

- Operating margin 14% while adjusted operating margin 24% versus 25% in Q3 2019 and -6% in Q2 2020

- Net Income $234mm (RMB 1.581B)

- EPS $3.07 (RMB 20.86) versus

- Adjusted EPS $0.34 (RMB 2.32) versus analyst estimate of RMB 1.11

- Q4 revenue forecast a decline between -37% and -42% year over year

H-Share Update

The Hang Seng bounced around the room closing -0.13%/-35 index points at 26,532. Volume increased 18% which is 147% of the 1 year average while breadth saw 23 advancers and 20. The 203 Chinese companies listed in HK within the MSCI China All Shares were off -1.01% led by energy +0.61% and utilities ++0.11% while tech -3.31%, discretionary -3.03%, real estate -1.44%, health care -1.26% and communication -0.54%. Southbound Stock Connect volumes were moderate as mainland investors bought $566mm as Southbound trading accounted for 9.6% of HK turnover.

A-Share Update

Shanghai & Shenzhen traded in a narrow range as Shanghai pulled a James Bond -0.07% while Shenzhen +0.16%.Volume was flat +0.9% which is 105% of the 1 year average. The 522 mainland stocks within the MSCI China All Shares +0.1% led higher by real estate +0.98%, tech +0.71% and energy +0.4% while discretionary -0.4%, utilities -0.39%, communication -0.31% and financials -0.22%. Northbound Stock Connect volumes were moderate as foreign investors sold -$613mm of mainland stocks as Northbound Connect trading accounted for 6.1% of mainland trading.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.57 versus 6.57 yesterday

- CNY/EUR 7.93 versus 7.90 yesterday

- Yield on 1-Day Government Bond 0.97% versus 1.00% yesterday

- Yield on 10-Year Government Bond 3.29% versus 3.27% yesterday

- Yield on 10-Year China Development Bank Bond 3.74% versus 3.72% yesterday

- China's Copper Price +0.09%