Copper Higher on Strong China Trade Data, Stocks Overshadowed by FTSE Complying with Executive Order

4 Min. Read Time

FTSE announced that it will remove eight Chinese companies' eleven stock (three companies have Hong Kong and Mainland China share classes) from their indices during their quarterly rebalance on Monday, December 21st due to the Executive Order. The stocks do not have significant weights in FTSE or MSCI indices. Once again, we should check our CNH, China's currency that trades during US hours, to gauge whether equity markets are overreacting to the news. CNH is basically flat in early US trading today, indicating that we should not trade emotionally based on headlines.

FTSE had to act as their pro forma for the rebalance is coming Up. Meanwhile, MSCI is likely to do the same as market liquidity could dry up with the holiday season approaching. In theory, they have time to see whether there will be a legal challenge to the Executive Order. FTSE-benchmarked asset managers will need to trade out of them by Friday, December 18th. The one index provider that has a dilemma is CSI as their CSI 300 Index has far more assets benchmarked to it within China than outside of China. This highlights why we chose to work with MSCI over seven years ago for China A exposure as they take the view of a foreign investor.

For asset managers, the Executive Order is not a significant issue though the implications for US and global financial companies make it a much bigger issue. Can a US financial firm's Hong Kong or Asia unit create structured products off the stocks? Are US firms allowed to trade Hang Seng Index futures as the value includes China Mobile? What happens to China Mobile's ADR in the US? So many questions, but so few answers. We should expect to see the scope of the Executive Order expanded to include a few more stocks.

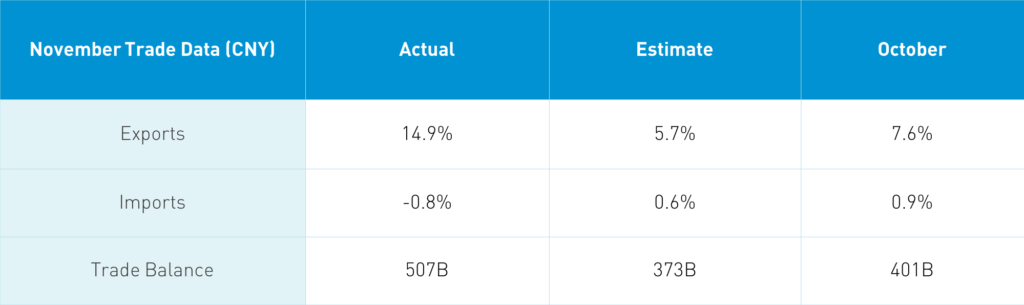

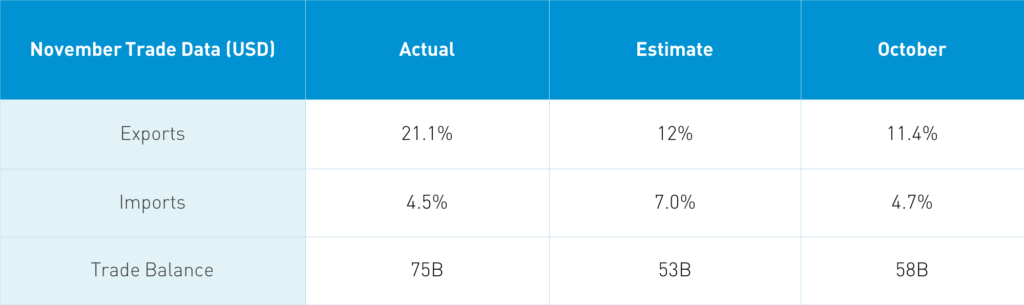

Takeaway: The strong data release was overshadowed by the FTSE announcement. Strong export growth was driven by demand for Chinese medical equipment and PPE, computers/laptops due to quarantine demand, and probably iPhones. Much attention has been given to the export data so I took a look at import data. Imports from the US surged 32.7% year over year and increased to $14.5 billion from October's $12.4 billion. Imports plummeted from the UK and Russia and slipped from Brazil. This would lead me to believe China's US agricultural purchases are still strong. Deteriorating China and Australia relations have garnered headlines, though Chinese imports from Australia increased +9.2% in November. While stocks were off today on light volumes, it is worth noting that Dr. Copper was up +0.28% in China trading based on the data.

Key News

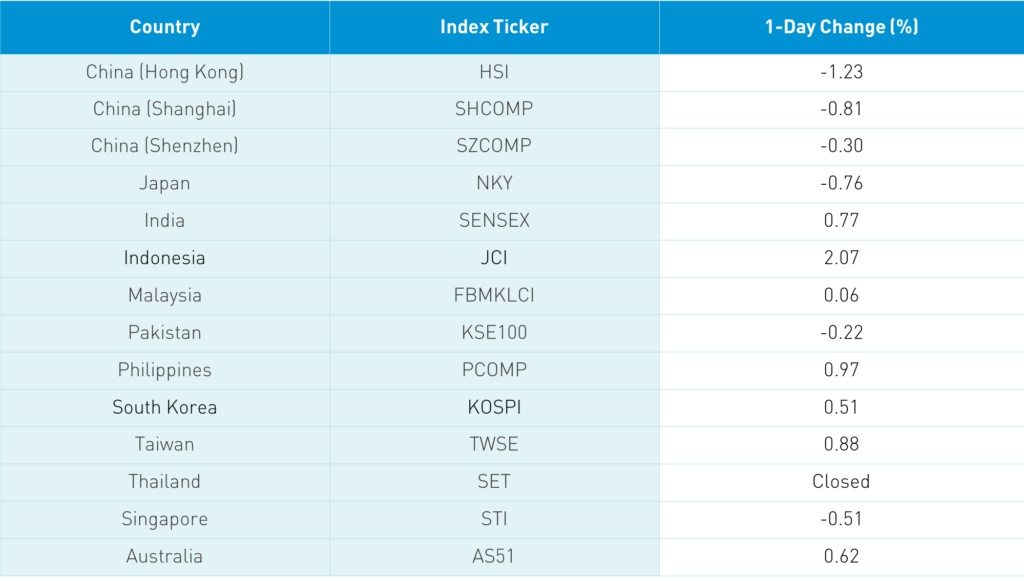

Asian equities had a mixed session on light volumes as Japan, Hong Kong, and China were hit with profit taking driven by the FTSE announcement. Meanwhile, Korea had a strong day. Hong Kong volumes were well off, which could indicate that we should not place too much emphasis on today's market action. It reminds me in the great World War I movie "1917", when the two British soldiers were commanded to deliver a messenger through German lines to tell the front-line trench commander that they want to go out of the trench and over the wire into German territory. He is in disbelief that they want to go into German territory, but ultimately says go for it! The FTSE news overshadowed the strong trade data released mid-morning.

Hong Kong volume leaders were Tencent, which fell -0.85%, Meituan, which fell -2.15%, Ping An, which fell -1.33%, Alibaba HK, which fell -2.27%, Xiaomi, which fell -0.79%, Executive Order removal stock CNOOC, which fell -3.11%, Semiconductor Manufacturing, which gained +3.57%, China Construction Bank, which fell -1.97%, and Sino Biopharma, which gained +4.63% after announcing an investment in a biotech company that is working on a coronavirus vaccine. Healthcare was a lone bright spot today as it was a fairly broad decline though volumes were light.

Mainland investors were net buyers of today's weakness via Southbound Stock Connect as Tencent and Meituan saw healthy buying. Mainland China was off a touch with Shanghai and Shenzhen -0.81% and -0.3%, respectively, as small and mid-caps held up better than large caps. Value plays such as financials underperformed today. Foreign investors sold Mainland stocks, though not in size, while CNY was stable overnight.

Barron's interviewed a Westport, Connecticut based CIO, who remarked on China's Five Year Plan and the rise of China's domestic consumption. When asked what the best investment opportunity post-Covid, she answered "Diversifying into China". No, the interview was not with me! But, it was with the iconic hedge fund Bridgewater Associates' Karen Karniol-Tambour. It was a great interview and is worth reading. Without giving too much away, I thought one of the most important aspects was Bridgewater's extensive use of data to come to their conclusions. There is so much conjecture and hyperbole when it comes to China with so little supporting data. It also touched on the feasibility of new metrics other than GDP being used to measure "human well-being," which was exactly what I heard at an event from ex-tech entrepreneur and Presidential candidate Andrew Yang.

JD Health will list tomorrow in Hong Kong under ticker 6618 HK and will raise about $3.5 billion by selling 381 million shares at HKD 70.58 each. I will do a full overview of the company tomorrow. Bloomberg is reporting that the IPO is oversubscribed over 400X. The stock should rip tomorrow based on indications and it is trading up nearly 30% at HKD 90 in over-the-counter trades.

H-Share Update

The Hang Seng slipped -1.23%/-329 index points to close at 26,506. Volumes were off -21% from Friday, which is 108% of the 1-year average while breadth was off with 12 advancers and 37 decliners. The 203 Chinese companies listed in Hong Kong and within the MCI China All shares Index fell -0.17%, led by heath care +0.93%. Meanwhile, materials -2.76%, financials -1..86%, discretionary -1.83%, real estate -1.82%, energy -1.69%, and staples -1.56%. Southbound Stock Connect trading volumes were light/moderate as Mainland investors bought $267 million worth of Hong Kong stocks today as Southbound Connect trading accounted for 10.7% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen were off -0.81% and -0.3% to close at 3,416 and 2,294, respectively. Volume was up 2.7% from Friday though that is only 92% of the 1-year average. Meanwhile, breadth was off with 1,178 advancers and 2,605 decliners. The 522 Mainland stocks within the MSCI China All Shares Index fell -0.65% led by staples, which gained +0.61% and tech, which gained +0.3%, while financials -2.19%, real estate -1.94%, energy -1.76% and utilities -1.58%. Northbound Stock Connect volumes were moderate as foreign investors sold $177 million worth of Mainland stocks as Northbound Stock Connect trading accounted for 6% of Mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.53 versus 6.53 Friday

- CNY/EUR 7.93 versus 7.93 Friday

- Yield on 1-Day Government Bond 1.02% versus 1.32% Friday

- Yield on 10-Year Government Bond 3.27% versus 3.27% Friday

- Yield on 10-Year China Development Bank Bond 3.72% versus 3.72% Friday

- China Copper Price +0.28% overnight