JD Health’s IPO Has “The Right Stuff” To Fly, Hong Kong Value “Bought the Farm” And Underperformed

5 Min. Read Time

Key News

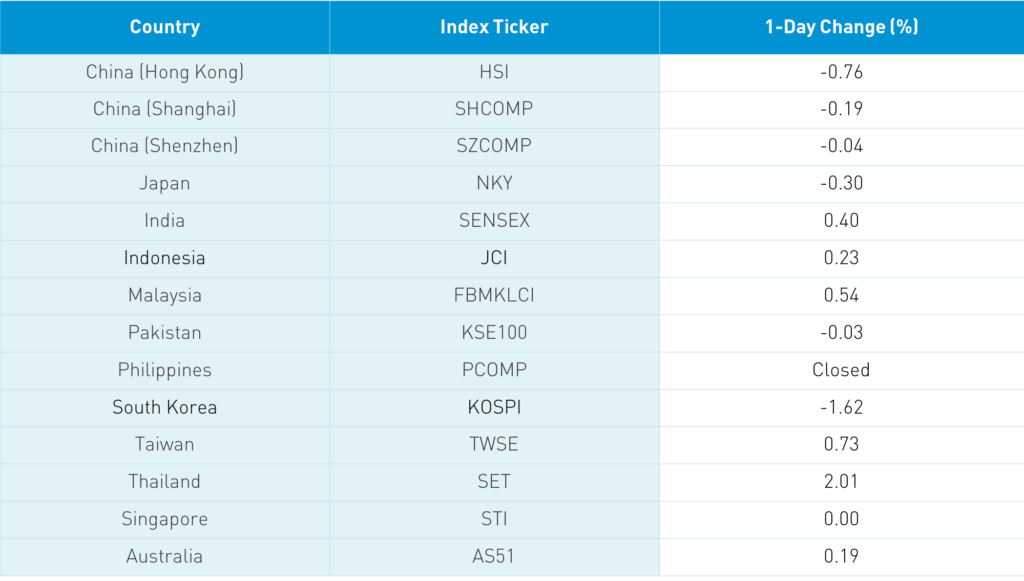

Asian equities were mostly off on plunging/light volumes. Taiwan outperformed while Korea took a hit after yesterday’s strong performance. The Hang Seng was off by -0.76% on US-China political rhetoric and tightening social distancing measures, though the real culprit was a very weak day for value within the index. Sectors such as financials, energy, and real estate lagged while growth stocks outperformed. According to Chuck Yeager’s autobiography, “bought the farm” was the term used by test pilots trying to break the sound barrier when a fellow pilot died.

However, there were positives such as Goldman Sachs' announcement that it would buy out its local joint venture securities partner and Great Wall Motor's strong November car sales, which grew +26% year-over-year. The company's shares gained +11.7% and led to an auto sector rally. Foreign Minister Wang Yi’s commented on China’s commitment to the US trade agreement during a US-China Business Council webinar.

Of course, the big news was JD Health’s IPO (6618 Hong Kong), which ripped +55% on volume more than 3X the second most heavily traded stock. The company’s lead managers were BofA Securities, Haitong, and UBS, though the joint managers included many local and Asia-focused investment banks, which lead to healthy retail participation. We do a full deep dive on JD Health below as their IPO prospectus contained a wealth of information on China’s health care industry. Behind JD Health on the Hong Kong volume leaderboard were Xiaomi, which gained +4.77% amid heavy buying in Southbound Connect, Tencent, which fell -0.09%, Meituan, which rose +1.8%, Ping An, which fell -3.42%, Alibaba Hong Kong, which was flat, energy giant and assumed Executive Order target CNOOC, which dropped -3.91%, JD.com Hong Kong, which fell -1.81% despite owning a large slug of JD Health in a head-scratcher to me, though some said its seeing profit-taking from its pre-IPO rally, BYD, which rose +2.54%, and HSBC, which fell -3.61% on worries that its dividend may be reinstated by UK regulators.

Shanghai & Shenzhen bounced around the room to close -0.19% and -0.04% respectively as volume leader Kweichow Moutai rose +2.07% and BYD gained +1.53%, as liquor and autos outperformed. It’s worth noting that the Mainland stocks within the MSCI China All Shares Index, a total China index including US, Hong Kong, and Shanghai/Shenzhen stocks, gained +0.11% today. Foreign investors bought a healthy $1.022 billion of Mainland stocks today while the renminbi appreciated versus the US dollar.

Baidu (BIDU US) announced that it would raise its share repurchase program to $4.5B up from $3B. If US-listed Chinese stocks were going to be delisted, why would Baidu be spending money to buy the shares?

China reports November CPI and PPI tomorrow. I’m going to predict CPI will fall as pork prices have been falling, while PPI will rise based on higher commodity prices in November versus October.

According to a Mainland media source, the Shanghai International Energy Exchange will list a renminbi-denominated copper future. As Bands Financial’s John Browning stated in the article “There is no reason why China, being such a big consumer, shouldn’t be the price-maker…and not the price-taker.” Valid point!

A Mainland media source quoted UBS Asset Management statement that “China’s bond yields are superior to those of major global economies”. In Europe and Asia, investors are throwing the kitchen sink at China’s bond market. Here in the US? Crickets! US-listed Chinese bond ETFs have seen inflows of $31mm YTD, despite the median return of +9.27%.

The WSJ is reporting that another judge has tapped the brakes on the Tik Tok ban after granting a “preliminary injunction that stops the Commerce Department from implementing restrictions”. It’s amazing to think that Tik Tok’s Generation Z users were able to come together and block the Executive Order, while the entire US financial industry can’t do the same with the EO stopping US investors from investing in a dozen Chinese stocks on claims they are affiliated with China’s military though no evidence was presented. I’m as guilty as the next though hopefully, someone steps up.

A hat tip in today’s headline to Chuck Yeager who passed away today. Reading Yeager’s autobiography as a teenager was an inspiring read that doing great things requires great courage. I will watch “The Right Stuff” with the family tonight. Today’s WSJ obituary is a worthwhile read.

JD Health listed today on the Hong Exchange, selling 381mm shares at a price of Hong Kong $70.58, which raised $3.5B. Let’s take a deeper dive into the largest online pharmacy and online medical consultant by revenue, according to the company.

- The online pharmacy has 72.5mm users for the 12 months ended June 30, 2020, and represented 87.6% of total revenue with the average user spending RMB 176.

- The company sold RMB 11.5B worth of goods through direct sales while another RMB 22.4B was sold through 9,092 third party merchants for the 6 months ended June 30, 2020.

- The company employs 138 doctors while leveraging access to another 21,319 external doctors.

- Average daily consultations increased from 14,835 to 86,100 in comparing the first six months of 2019 to the same period in 2020.

- Sales of pharma and healthcare represented 87.6% of revenue as it increased to RMB 7.693B from RMB 4,365B in comparing the first six months of 2020 to the same period in 2019.

- Gross profit increased 76% in the first six months of 2020 driven by product revenue increasing to RMB 1.154B from 716mm and service revenue increasing to RMB 1.062B from 614mm in comparing the first six months of 2020 to the same period in 2019.

- JD.com will own 68.73% of JD health post-IPO though before the greenshoe is allocated.

- The company had a loss of RMB 5.360B due to a convertible bond sale though on a non-GAAP adjusted basis would have generated RMB 370mm.

- China’s healthcare expenditures are expected to be RMB 7.254 trillion in 2020 up from RMB 4.097 trillion in 2015 while growing to 17.616 trillion in 2030.

- China’s population over the age of 65 is expected to rise from 12.6% in 2019 to 21.5% in 2030.

- Health care consumption is expected to account for 27.7% of per capita expenditure by 2030 rising from RMB 4,657 in 2019 to RMB 12,191 in 2030.

- Stroke and diabetes cases are expected to grow at 4.5% and 2.7% between 2019 and 2024.

- Only 2.4% of China pharma products were sold through non-hospital online retail pharmacies versus 25.8% of total retail sales of consumer goods sold online.

- For the last twelve months, I ran revenue which for JD Health was +32% to $1.57B versus Alibaba Health +88% to $1.8B and Ping An Healthcare and Technology’s +51% to $787mm.

H-Share Update

The Hang Seng opened lower and stayed there off -0.76%/-202 index points at 26,304. Volume was up +0.1%/flat, which is 108% of the 1-year average while breadth was off with 14 advancers and 26 decliners. The 203 Chinese companies listed in Hong Kong were off -0.24%, with tech up +3.13% and discretionary +1.82%, while energy was off -3.08%, financials -2%, real estate -1.3%, and industrials -1.13%. Southbound Connect volumes were light with Mainland investors buying $397mm of Hong Kong stocks today as South Connect accounted for 9.7% of Hong Kong turnover.

A-Share Update

Shanghai & Shenzhen bounced around the room off -0.19% and -0.04% at 3,410 and 2,293 respectively. Volume was off -8.7%, which is 84% of the 1-year average. The 522 Mainland stocks within the MSCI China All Shares Index gained +0.11%, led by staples +1.02%, materials +0.41%, and discretionary +0.32%, while real estate fell -0.48%, financials -0.45%, and energy -0.33%. Northbound Stock Connect volumes were light as foreign investors bought $1.022 billion of Mainland stocks today as Northbound Connect trading accounted for 5.3% of Mainland turnover.