Mainland Moves Higher, Internet Companies Move Lower After Regulatory Slap on Wrist

3 Min. Read Time

Upcoming Events This Week:

What May Be Ahead for 2021: A Discussion with Quadratic Capital’s Portfolio Manager, Nancy Davis

Tomorrow, December 15th at 10 am EST

Click here to register

What’s Next for China in 2021? A-Share Inclusion and Macro Update with MSCI

Thursday, December 17th at 11 am EST

Click here to register

Key News

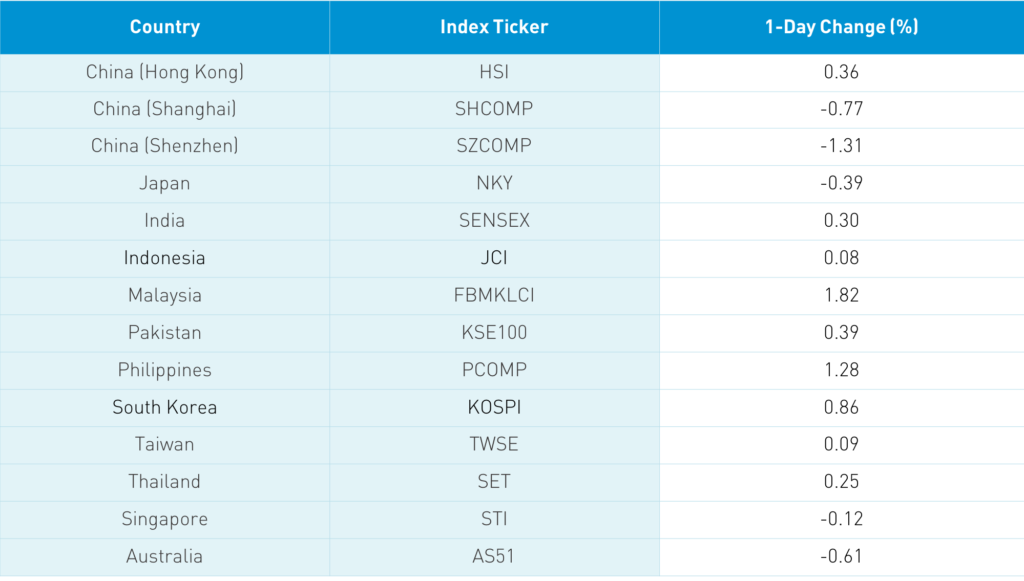

Asian equities were largely higher on lighter volumes. However, Taiwan and South Korea took a breather from their recent strong performance. The Hang Seng Index was off -0.44% led by internet names after Meituan, Alibaba, and Tencent-backed China Literature were each fined RMB 500,00 (USD 76,000) under the new anti-monopoly law that appears focused on prohibiting large companies from financing loss-generating subsidiaries, which crowds out smaller companies’ ability to compete. The slap on the wrist reminds me of the quote from Apocalypse Now on “handing out speeding tickets at the Indy 500”. The market appeared to shoot first rather than ask questions. Group buying, which is popular in China as the more buyers the lower the price, similar to what Groupon tried in the US, was highlighted in the Mainland media. The thought is that group buying might lower the price, which is adverse for competing vendors. However, one could easily argue the sales generated from group buying would not have occurred without it.

It is worth noting that Meituan cut its loss by half intra-day while Alibaba was off its intra-day low by 1%. Hong Kong volume leaders were Tencent, which fell -2.89% and Meituan, which fell -3.81% after experiencing a rare sell day via Southbound Stock Connect, Xiaomi, which gained +5.99% after announcing strong sales, Alibaba HK, which fell -2.63%, Ping An Insurance, which gained +0.92%, JD Health, which gained +7.87%, JD.com HK, which fell -1.56%, energy giant CNOOC, which gained +3.45%, China Mobile, which fell -0.23%, China Construction Bank, which fell -0.86%, Pop Mart, which gained +7.97%, and Geely Auto, which gained +2.05% as strong auto sales lift the sector.

Shanghai and Shenzhen outperformed gaining +0.66% and +1.07%, respectively, driven by President Xi’s comments on raising clean energy’s role while cutting carbon dioxide emissions. Policymakers’ reiterated support for domestic consumption, which lifted staples. Meanwhile, autos had a strong day, which lifted discretionary. The Mainland’s volume leader was Kweichow Moutai, which gained +0.49%. Health care also had a strong day. Foreign investors were net buyers of Mainland stocks via Northbound Stock Connect, buying $34 million worth as Shanghai stocks saw net selling and Shenzhen stocks saw net buying today. CNY appreciated slightly versus the US dollar.

Nasdaq Indices will remove four Chinese stocks due to the Executive Order barring investment from US investors in companies with alleged ties to China’s military. On Friday the CSI 300 Index, a Mainland China domestic benchmark, rebalanced and did not remove these stocks unlike FTSE Russell and S&P Dow Jones, which have announced the removal of these stocks. MSCI is expected to indicate whether and when they will remove the stocks shortly. The lack of removal from the CSI 300 index makes sense as the index is far more widely tracked within China than outside of China. However, CSI 300-benchmarked ETFs in the US will likely have to optimize the names out of their index. This highlights why we use MSCI over six years ago as our A-Share benchmark. MSCI views foreign markets from the perspective of a foreign investor.

November economic data releases for Industrial Production, Retail Sales, Fixed Asset Investment and Property Investment are expected tomorrow.

Barron’s EM reporter Reshma Kapadia wrote on the bill that would delist US-listed Chinese securities. I was able to provide a quote in the balanced article. It notes that the SEC, via the White House Working Group on Financial Markets, appears to provide a path for compliance by allowing the Big Four auditors to validate their Chinese subsidiaries’ work. This proposal would allow for compliance and for the companies to continue retain their US listings. This is on top of the potential increased dialogue between US and Chinese regulators, which did not occur under the current administration. I am constantly shocked that how little recognition this statement receives as click bait headlines do a disservice in ignoring it.

H-Share Update

The Hang Seng opened higher but slide to close -0.44%/-116 index points at 25,389. Volume increased +5% from Friday, which is +13% above the 1-year average while breadth was off with 17 advancers and 31 decliners. The 203 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index fell -0.73% with tech +3.44%, real estate +1.02%, and energy +0.78%. Meanwhile, communication -2.6%, discretionary -1.25%, health care -1.03% and industrials -0.43%. Southbound Stock Connect volumes were moderate/light as Mainland investors bought $12 million worth of Hong Kong shares as Southbound Connect trading accounted for 11.4% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen opened lower but grinded higher to close +0.66% and +1.07% at 3,369 and 2,247, respectively. Volume was off -14.8% from Friday, which is -16% below the 1-year average while breadth was positive with 2,414 advancers and 1,333 decliners. The 522 Mainland stocks within the MSCI China All Shares Index gained +0.95% led by staples +2.02%, discretionary +1.38%, health care +1.31%, real estate +1.06% and tech +0.79% while energy lagged -3.09%. Northbound Stock Connect volumes were moderate/light as foreign investors bought $34 million worth of Mainland stocks as Northbound trading accounted for 5.1% of Mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/EUR 6.54 versus 6.55 yesterday

- CNY/USD 7.96 versus 7.94 yesterday

- Yield on 1-Day Government Bond 1.35% versus 1.29% Friday

- Yield on 10-Year Government Bond 3,29% versus 3.29% Friday

- Yield on 10-Year China Development Bank Bond 3.70% versus 3.72% Friday