Hong Kong Growth ‘Jock’ Stocks Regain Their Popularity

4 Min. Read Time

Upcoming Events:

What’s Next for China in 2021? A-Share Inclusion and Macro Update with MSCI

Thursday, December 17th at 11 am EST

Click here to register

Key News

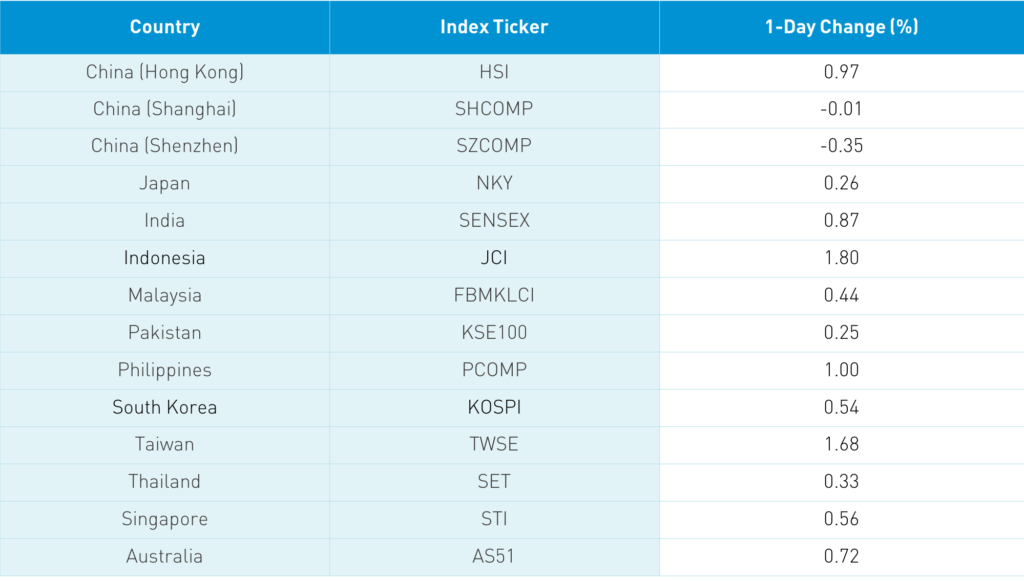

Asian equities were higher on US stimulus and vaccine roll out though volumes were light. The Hang Seng was up +0.97%, led by the internet names kicked to the curb earlier this week as investors appear to recognize that China’s new anti-monopoly law is unlikely to be seriously detrimental to the companies’ prospects. I jokingly call these growth stocks the jocks as they are popular, while value stocks are the nerds. Hong Kong volume leaders were Tencent, which rose +2.05%, laundry detergent company Blue Moon, which IPO'd +13.07%, Meituan, which rose +1.82%, Alibaba Hong Kong, which gained +2.03%, Xiaomi, which fell -0.85%, Semiconductor Manufacturing, which dropped -4.94% after MSCI’s announcement discussed below, JD.com Hong Kong, which rose +1.7%, Xinyi Solar, which fell -2.24% after announcing stock issuance, Ping An Insurance, which gained +0.86%, energy giant CNOOC, which was flat at 0.0%, and Geely Auto, which dropped -0.87%.

The best sector in Hong Kong and Mainland China was healthcare, driven by chatter that a new national drug procurement auction wasn’t going to see a dramatic price drop. China’s government started buying drugs in bulk for hospitals to negotiate a better deal, which makes sense though previous auctions had seen dramatic price drops in competitive bidding. Apple’s suppliers had a good day on a strong 2021 production outlook, with Sunny Optical gaining +1.56% and AAC gaining +3.02%. Shanghai and Shenzhen were off a touch -0.01% and -0.35% respectively, though as noted below, the Mainland stocks within the MSCI China All Shares Index were all up +0.35%, led by Kweichow Moutai, which rose +1.32%, and alcohol peer Wuliangye Yibin, which gained +1.3%. Bestechnic Shanghai, a Bluetooth audio chip maker, IPO'd +123% as today’s volume leader. Not a typo!

The PBOC injected liquidity into the financial system to offset liquidity drying dry up as financial firms close their books for 2020. While autos took a breather, home appliance stocks were strong. The Central Economic Work Conference could provide a catalyst for several sectors as the policy is drafted in alignment with the new 14th Five Year Plan. We created a new way to invest, so reach out if interested! Foreign investors bought $293mm of Mainland stocks via Northbound Connect today, which brings year-end investment to $25.8 billion. I suspect that many active managers will need to add Chinese Mainland stocks to their portfolios as part of year-end window dressing, as they’ll need to show their holdings at month-end. CNY appreciated slightly versus the US dollar while bonds were flat.

Foreign Direct Investment increased by 5.5% in November year-over-year. Not a market-moving release, but doesn’t the data run counter to the narrative of supply chains coming out of China? Factories are in China and Asia because 4 billion live there versus less than 400mm in the US representing a massive customer base. Where would you put a factory? As we’ve stated, according to the NY Fed, US-owned factories generated $375 billion of revenue in 2017 for US companies. China has paid a severe environmental consequence for being the world’s factory. I don’t think anyone wants a coal smelter in their neighborhood. “Bring it back” is a joke.

MSCI announced that it will be dropping 10 Chinese companies’ Hong Kong and Mainland stocks from its indexes on January 5th. The stocks don’t make up a large percentage of indices, so this drop is no big deal. Brokers are estimating just over $1B of stock will need to be sold, which sounds like a lot but in reality, is a blip. MSCI’s press release says that other stocks might be added based on clarity from the Office of Foreign Asset Control (OFAC). The MSCI release alludes to a lack of clarity on the issue. We’ve heard that there is no clarity from OFAC, which isn’t surprising since they didn’t write the Executive Order.

The WSJ has an editorial titled “Congress Punts on China Stocks”, which correctly points out enforcement of the soon to be law comes from the SEC. The editorial focuses on the legislation’s line that the SEC should not delist the companies if not less than “one-third of the company’s total audit is performed by a firm beyond the reach of the PCAOB inspection”. I believe the more important line comes from the White House’s Working Group on Financial Markets August release. This states that as long as the Big Four will validate the audit work of their Mainland subsidiary, it is considered compliant. The WSJ does point out the legislation would have included US companies doing business in China as their China operations audit is also done by the Big Four’s Mainland subsidiaries. Oops! Regardless it’s my belief the legislation is more bark than bite as the SEC approved the Chinese companies’ listings. These companies didn’t suddenly appear on US exchanges! They were approved to list here. US investors have $2 trillion invested in these companies. No one wants to hurt US investors’ savings during a recession.

iQIYI (IQ US) announced after the US close that it will raise $800mm through the sale of a convertible note and the issuing of 40 million new shares. The new share supply should weigh on the stock today.

H-Share Update

The Hang Seng opened higher and stayed there, closing up +0.97%/+253 index points at 26,460. Volume was off -10% from yesterday, which is 2% below the 1-year average while breadth was positive with 40 advancers and 7 decliners. The 203 Chinese companies listed in Hong Kong within the MSCI China All Shares Index rose +1.07%, led by healthcare +1.93%, communication +1.93%, discretionary +1.05%, real estate +1.02%, and industrials +0.69, while tech was the only negative sector that fell -0.15%. Southbound Connect volumes were light/moderate in mixed trading as Mainland investors $9mm of Hong Kong stocks today as Southbound trading accounted for 11.4% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen had a choppy day with a weak closing leading to a loss of -0.01% and -0.35% at 3,366 and 2,248 respectively. Volume was off -2%, which is -18% below the 1-year average while breadth was off with 976 advancers and 2,914 decliners. The 522 Mainland Chinese stocks within the MSCI China All Shares Index gained +0.35%, led by staples +1.39% and industrials +0.78%, while communication fell -1.16%, tech -0.76%, and discretionary -0.06%. Northbound Stock Connect volumes light/moderate as foreign investors bought $293mm of Mainland stocks today.

Last Night's Exchange Rates & Yields

- CNY/USD 6.53 versus 6.54 yesterday

- CNY/EUR 7.96 versus 7.95 yesterday

- Yield on 1-Day Government Bond 0.95% versus 1.35% yesterday

- Yield on 10-Year Government Bond 3.28% versus 3.28% yesterday

- Yield on 10-Year China Development Bank Bond 3.68% versus 3.68% yesterday