FTSE’s Index Rebalance Drives Asian Equity Volumes, Week in Review

5 Min. Read Time

Week in Review

- Growth stocks in Hong Kong saw selling Monday on the heels of a new antitrust legislation that prohibits internet giants from financing loss-generating subsidiaries.

- The Central Economic Work Conference (CEWC) began on Tuesday. The conference is an important policy event in China as lawmakers review the first draft of the all-important 14th Five Year Plan, which is due to be released in the spring of 2021.

- The IPO of Bestechnic Shanghai, a Bluetooth audio chip maker, on the Shanghai Stock Exchange rocketed +123% Wednesday. Meanwhile, a rotation into growth occurred in Hong Kong as investors' fears over the new antitrust law were tempered.

- Healthcare was one of the best performing sectors in Thursday trading on the Mainland as the National Drug Procurement Auction now appears more favorable than expected to pharmaceutical companies' bottom lines. Meanwhile, foreign investors bought a whopping $1.2 billion worth of Mainland stocks, bringing the year-to-date cumulative inflow to nearly $25 billion.

Friday's Key News

Today represents the last true trading day of the year as most of Wall Street will punch out after today. Quad witching is the expiration of index futures, single stock futures, equity index options and single stock options. New portfolio weights for FTSE Russell, S&P Dow Jones and Nasdaq indexes starting Monday requires passive managers to trade their portfolios today at the close so their portfolios match the new index on Monday. Tesla does not technically enter the S&P 500 until Monday, but we'll come off as a smarty pants and won't make friends if we correct people.

Asian equities ended a strong performance week softer on higher volume due to the FTSE index rebalance trades. Markets liked the Wall Street Journal article on the US Treasury pushing back on the State Department's effort to ban US investors from investing in 35 Chinese companies. However, the positive sentiment faded as a Reuters reported that the Commerce Department will be adding more Chinese companies to a technology export ban.

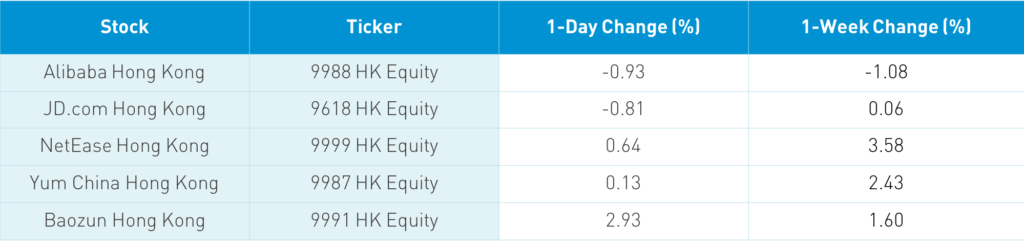

The Hang Seng Index was off -0.67% though the broader Hang Seng Composite Index was off -0.36% and the Chinese companies listed in Hong Kong and within the MSCI China All Shares Index were off -0.34%. Australians have a saying: "the tall poppy gets cut" i.e. markets tend to deflate egos. I may have jinxed my Hong Kong growth stocks today by writing about how well they were doing as Hong Kong volume leaders were all off with Tencent down -0.51%, Alibaba HK down -0.93%, Meituan down -2.32%, Ping An Insurance down -2%, Xiaomi down -1.71%, JD HK down -0.8%, China Construction Bank up +0.17%, vaping company Smoore up +4.06%, and JD Health up +6.02%. The value nerds had a good day as materials, energy, and utilities outperformed.

It is worth noting that today saw the removal of a dozen Chinese stocks from FTSE and S&P indices. China Mobile rose +3.17% and Semiconductor Manufacturing fell -5.2%, likely due to the Reuters report. Today was a rare outflow day for Southbound Connect as Mainland investors sold -$110 million worth of Hong Kong stocks. They are likely taking some profits before year end. Tencent, Meituan, and Xiaomi all experienced net selling today. There has been some chatter that regulators might tax internet companies for selling data on their users. I would assume their revenues are already taxed so a head scratcher to me.

Shanghai and Shenzhen ended a positive week slightly weaker off -0.29% and -0.3%, respectively. Financials were off as brokers sold off after their recent run. Meanwhile, materials and energy outperformed. CNY and bonds were both off a touch. Foreign investors sold -$206 million worth of Mainland stocks today, but, for the week, they bought a net $1.298 billion. Year-to-Date net foreign inflow is now at $26.85 billion.

I had a debate last night with my friend Ken who works in the institutional brokerage arm of a major Chinese bank in Hong Kong. It is funny that I have not met Ken in person but consider him a friend as we often chat about markets. Ken is an American raised in Brooklyn who went to an Ivy League school followed by a stint in Japan with a major Wall Street firm and now resides in Hong Kong. Ken believes that value stocks are due for a comeback, with which I do not necessarily disagree. Ken sees the demand for Hong Kong growth stocks and a robust IPO market as signals for a value comeback. My counter argument is that most US investors do not get overly granular in their non-US stocks as they simply buy broad emerging markets.

It is funny to me to read that investors should buy EM stocks because commodity prices are higher. What percentage do commodity-dependent countries make up in the EM index? Hardly any! Same for the sector weights. There is a strong argument for diversifying into non-US equities, which I believe will play out in 2021. As that happens, most of the money will go into broad EM ETFs, which means most of that money will go into China and its growth stocks. We will find out in 2021 whether I am right!

Pensions & Investments magazine is widely read by institutional investors. Yesterday, they had an article titled "More institutions segregating China A shares". The catalyst for the article appears to be a report from institutional consultant Willis Towers Watson, which stated: "Chinese risk assets should account for 20% of global investor growth portfolios over the next 10 years, compared with the current average exposure of 5%."

Here is my take on Tesla entering the S&P 500. Once S&P announced it was adding the stock, passive managers estimated exactly how many Telsa shares they would need to buy based on S&P's pro forma S&P 500 (pro forma is fancy way of saying estimated future index weights). Based on the size of their S&P 500 funds and Tesla's weight, the passive manager then tells their brokers how many shares they will need to buy at 3:59 today. Since the passive managers are the biggest asset managers globally, they are among the brokers’ best clients (high trading hedge funds are the other best clients). Brokers started buying Tesla a week ago, I would guess, and hedged their position in the options market. At 3:59 today they will sell their Tesla positions to their passive asset manager clients while unwinding their option hedge. Mama didn't raise no dummy! I think Tesla will go down today because so many people believe index funds have to buy shares today.

H-Share Update

The Hang Seng slid lower throughout the trading day to close -0.67%/-179 index points at 26,498. Volume increased +29% from yesterday, which is 31% higher than the 1-year average. Meanwhile, breadth was off with 22 advancers and 27 decliners. The 203 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index lost -0.34% with materials +2.02%, energy +1.76% and utilities +1.11% while financials -0.94%, tech -0.9%, discretionary -0.88% and staples -0.8%. Southbound Stock Connect volumes were light/moderate as Mainland investors sold $110 million worth of Hong Kong stocks today. Southbound trading accounted for 8.3% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen slipped in the afternoon to close -0.29% and -0.3% at 3,394 and 2,262, respectively. Volume was off -2% from yesterday, which is -9% below the 1-year average. Breadth was off with 1,309 advancers and 2,451 decliners. The 521 Mainland Chinese companies within the MSCI China All Shares Index fell -0.42% with energy +2.13%, communication +1.39% and materials +1.15% while financials -1.34%, staples -1.08% and real estate -0.99%. Northbound Stock Connect volumes were moderate with foreign investors selling -$208 million worth of mainland stock as Northbound trading accounted for 6.6% of mainland turnover.

Last Night's Exchange Rates & Yields

- CNY/USD 6.54 versus 6.54 yesterday

- CNY/EUR 8.01 versus 8.00 yesterday

- Yield on 1-Day Government Bond 0.73% versus 0.95% yesterday

- Yield on 10-Year Government Bond 3.29% versus 3.28% yesterday

- Yield on 10-Year China Development Bank Bond 3.68% versus 3.68% yesterday