Tale of Two Chinas As Mainland and Hong Kong Markets Diverge

4 Min. Read Time

Key News

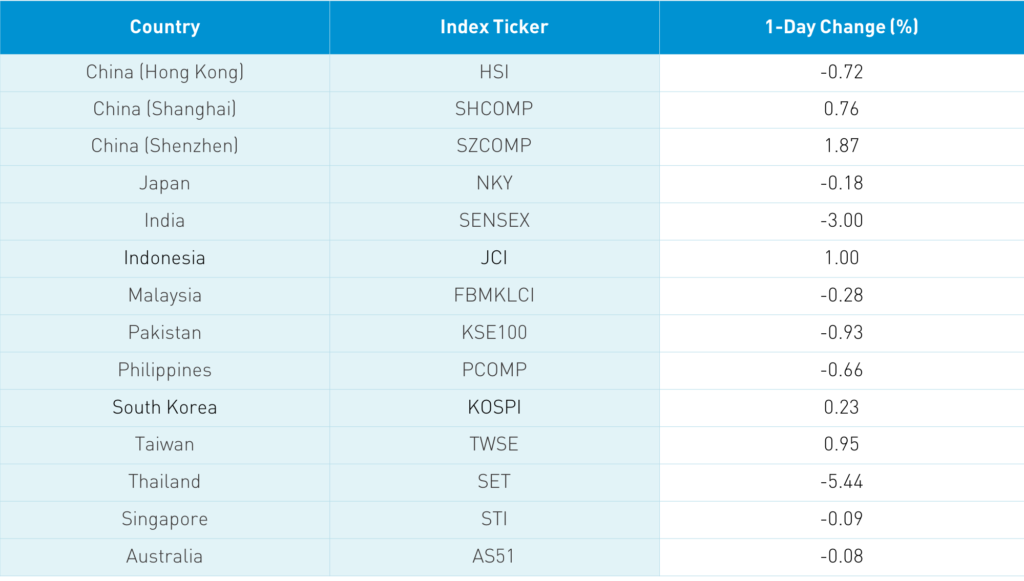

Asian equities were largely off with India and Thailand underperforming. Chief among investors’ concerns were increased global coronavirus cases and the uncertain fate of stimulus in the US. It was a tale of two Chinas today as Hong Kong was off on an expanded US technology export black list and President Trump’s signing of the US bill requiring US-listed Chinese companies to provide their audit books to the PCAOB or face delisting after three years. Meanwhile, Mainland markets were up as investors focused on the Central Economic Work Conference's commitment that supportive economic policies will not be removed hastily.

Remember that Hong Kong is the definition of China for foreign investors who react to media headlines. On the other hand, the vast majority of the Mainland stock market is owned by domestic investors. It is not so much that Mainland investors are unaware of the news, but rather they do not find it important. We have written extensively on why we do not believe the delisting law is a significant concern as enforcement is done by the SEC, which drafted the policy response allowing for US-listed Chinese companies' Big Four auditors to validate their Mainland subsidiaries’ work.

Hong Kong volume leaders were JD Health, which rose +12.24% after Hang Seng announced it would be added to the several indices including broader Hang Seng Composite, the Hang Seng Tech Index, and the index that is used for Southbound Connect eligibility. As we noted last week, JD Health has been designated a Consumer Discretionary stock by the Global Industry Classification System (GICS). Other volume leaders were Xiaomi, which gained +1.74%, Tencent, which fell -1.38%, BYD, which gained +11.68% on a deal to sell electric buses in Colombia, Hong Kong Exchanges, which gained +2.28% as the US law, which I fondly call the Hong Kong Investment Banker Employment Act, Meituan, which was flat as co-founder Wang Huiwen retires, Alibaba HK, which fell -2.19%, Semiconductor Manufacturing, which fell -3.63% after being added to tech export ban, Xinyi Solar, which gained +12.96% after announcing a share sale, and China Mobile, which fell -3.07%.

While Hong Kong was off a touch, Shanghai and Shenzhen were up +0.76% and +1.87%, respectively, led by a positive interpretation of the Central Economic Work Conference (CEWC) policy statement. The market exhaled that policy makers are not going to pull stimulus all at once. Rather, they will do so incrementally as the economy rebounds. While growth names were off in Hong Kong, they were strong on the Mainland. LONGi Green Energy was up +10.01% after prestigious private equity firm Hillhouse Capital announced a stake and brokers had a strong day. Real estate was off as the policy that "housing is for living and not speculating" was reiterated.

The big news overnight was another strong day of buying from foreign investors via Northbound Stock Connect as a very healthy $1.2 billion worth of Mainland stocks was bought today. CNY was off a touch as the dollar strengthened.

The 1 and 5-Year Loan Prime Rates were left unchanged at 3.85% and 4.65%, respectively, as expected.

After Friday's close Nike (NKE US) released fiscal Q2 financial results. The company’s $11.2 billion in quarterly revenue beat analysts’ estimate of $10.55 billion, driven by a +24% year over year gain in Greater China versus Asia Pacific & Latin America 0%, Europe/Middle East & Africa +17%, and North America +1%.

The CEWC mentioned the goals of reaching peak carbon output 2030 and carbon neutrality by 2060. The ambitious goals led to some speculation that China will implement a carbon cap and trade system. Starting a program for electrical utilities would make sense as their appetite for coal is a significant contributor to pollution.

The Wall Street Journal reported that Jack Ma tried to sell a piece of Ant Group to the government in an effort to allow the company to be listed. The article blows up the theory that Ant Group’s IPO was denied due to Ma's comments about regulators at a conference. We had previously suspected that this was not true.

Pinduoduo announced a stock sale to an undisclosed investor worth $500 million based on the closing price over the last five trading days.

Tesla did rise on Friday though it is worth noting that Indian equities fell today as after their weight increase in FTSE Russell indexes. It will be interesting to see if Tesla follows a similar path.

H-Share Update

The Hang Seng Index sold into the close -0.72%/-191 index points to close at 26,306. Volume was -13% from Friday, which is 13% higher than the 1-year average. Breadth was off with 10 advancers and 40 decliners. The 203 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index fell -0.3% with discretionary +1.42% and industrials +1.23%. Meanwhile, communication -1.57%, real estate -1.43%, and utilities -0.79%. Southbound Connect flows were moderate/light as Mainland investors bought $17 million worth of Hong Kong stocks and Southbound trading accounted for 12% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen grinded higher all day to close +0.76% and +1.87% at 3,420 and 2,304, respectively. Volume was up +12% from Friday, which is 2% higher than the 1-year average. Meanwhile, breadth was positive 2,524 advancers and 1,189 decliners. The 521 Mainland stocks within the MSCI China All Shares Index gained +1.21 led by discretionary +2.99%, industrials +2.74%, materials +1.95%, tech +1.79%, and health care +1.4%. Meanwhile, real estate +0.88%, utilities -0.78% and energy -0.73%. Northbound Stock Connect volumes were moderate as foreign investors bought $1.2 billion worth of Mainland stocks and Northbound trading accounted for 6.5% of Mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.55 versus 6.54 Friday

- CNY/EUR 8.00 versus 8.00 Friday

- Yield on 1-Day Government Bond 0.65% versus 0.73% Friday

- Yield on 10-Year Government Bond 3.27% versus 3.29% Friday

- Yield on 10-Year China Development Bank Bond 3.64% versus 3.68% Friday