Hong Kong Growth Gets Its Groove On

3 Min. Read Time

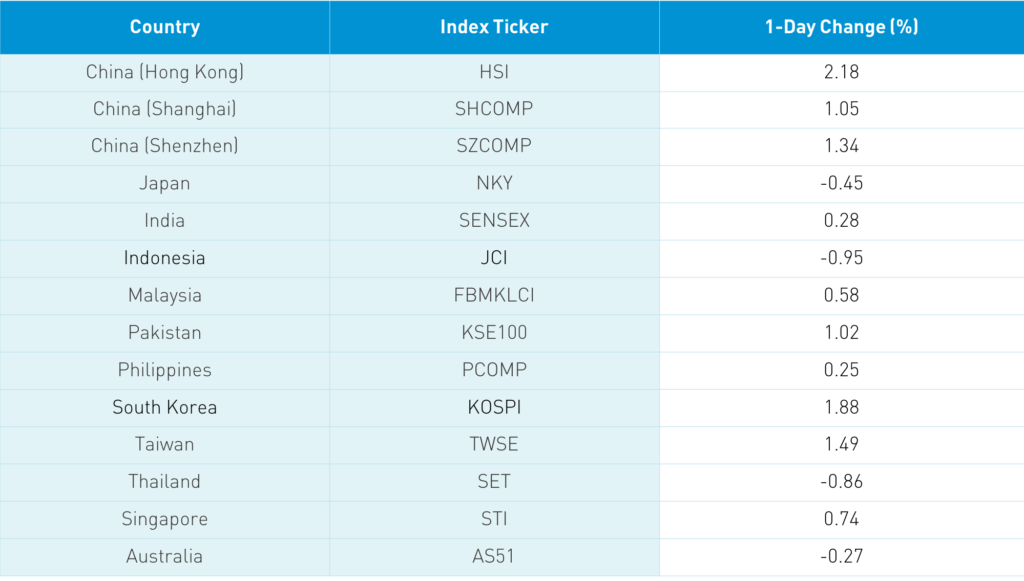

Key News

Asian equities were largely higher on light volumes as Hong Kong, China, and Korea outperformed. Growth stocks led gains in Hong Kong. Hong Kong volume leaders were Tencent, which rose +5.47%, Alibaba Hong Kong, which was up +6.4%, Meituan, which gained +5.27%, Xiaomi, which rose +0.46%, Semiconductor Manufacturing, which was up +11.96% on rumors of a deal with Dutch semiconductor company ASML, China Mobile and CNOOC, which were included in the Executive Order regarding Chinese companies with ties to China's military and fell -1.79% and -2.3% overnight, respectively, Hong Kong Exchanges, which rose +2.9%, BD, which gained +1.3%, and GCL Poly, which fell -12.03% after issuing new shares.

Healthcare stocks performed well on growing coronavirus cases globally. Shanghai and Shenzhen had a positive day, rising +1.05% and +1.35% respectively, driven by the PBOC continuing to add liquidity to the financial system going into year-end. Consumption names did well as rural consumption was highlighted in a speech by President Xi. Electric vehicles did well too as battery maker CATL gained +10.39% on a broker upgrade and the company’s investment announcement on growing their production capacity. Foreign investors bought a healthy $986 million worth of Mainland stocks via Northbound Stock Connect. Bonds had a very strong rally while CNY appreciated versus the US dollar.

There was no news overnight related to Alibaba, which is really about Ant Group. It does not appear that Ant will be broken up, though it will be regulated as a financial company, which may curtail its margins. Yesterday we discussed Baidu and Tencent’s past run-ins with regulators. I suspect something similar will play out with Ant Group over time.

The Office of Foreign Asset Control’s FAQ on how the financial industry should interpret the Executive Order banning US investors from investing in companies affiliated with China’s military brought up several issues. MSCI, FTSE Russell, and S&P Dow Jones will simply drop the stocks. No problem. For Asian index providers, on the other hand, the ban is problematic as they technically don’t fall under US jurisdiction, though their foreign investors might be. Thus far, local index providers including Hang Seng and CSI have not eliminated the stocks and are not expected to do so. There are no Hang Seng-based ETFs in the US, but there are in Europe. Hang Seng futures are quite popular as a hedge and for structured products. Will those hedges have to be unwound? Will structured products need to be unwound? There are ETFs listed in the US and Europe that follow CSI’s Mainland China indexes, i.e. A-Shares. One would assume the ETF providers will have to optimize the stocks out. The Q&A arguably creates more questions than answers, which makes us wonder how TikTok’s Gen Z users sued successfully to block an Executive Order after demonstrating the lack of evidence backing up the premise of the order. The US financial industry? Crickets.

The EU and China are close to signing an investment agreement that will provide European companies the opportunity to invest in a multitude of industries.

H-Share Update

The Hang Seng rose +2.18%/+578 index points to 27,147. Volume rose 10% from yesterday, which is 19% above the 1-year average while breadth was positive with 44 advancers and 7 decliners. The 203 Chinese companies listed in Hong Kong within the MSCI China All Shares Index rose +2.75%, led by communication +4.63%, health care +3.57%, and tech +2.56%, while energy fell -0.88%. Southbound Connect volumes were moderate/high as Mainland investors bought $758mm of Hong Kong stocks today as Southbound Connect trading accounted for 13.9% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen gained +1.05% and +1.34% to 3,414 and 2,288 respectively. Volume was off by -2%, which is just below the 1-year average while breadth saw 1,912 advancers and 1,772 decliners. The 523 Mainland Chinese companies within the MSCI China All Shares Index rose +1.61%, led by industrials +2.5%, staples +2.39%, discretionary +2.18%, health care +1.86%, and materials +1.27%. Northbound Stock Connect volumes were moderate/high as foreign investors bought $986mm of Mainland stocks as Northbound trading accounted for 5.9% of Mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.52 versus 6.53 yesterday

- CNY/EUR 8.01 versus 8.00 yesterday

- Yield on 1-Day Government Bond 0.37% versus 0.35% yesterday

- Yield on 10-Year Government Bond 3.12% versus 3.16%

- Yield on 10-Year China Development Bank Bond 3.53% versus 3.57% yesterday