CNY and Mainland China End Year Hitting 2 Year Highs, Week in Review

2 Min. Read Time

Week in Review

- On Monday, in response to the recent sell-off in its shares, Alibaba has increased its stock buyback program to $10 billion from $4 billion as the company believes its stock is undervalued.

- There was chatter on Tuesday that Ant Group will form a financial holding company similar to banks. This may provide a solution to regulators’ concerns.

- It was reported Wednesday that the EU and China are close to signing an investment agreement that will provide European companies the opportunity to invest in a multitude of industries.

Key News

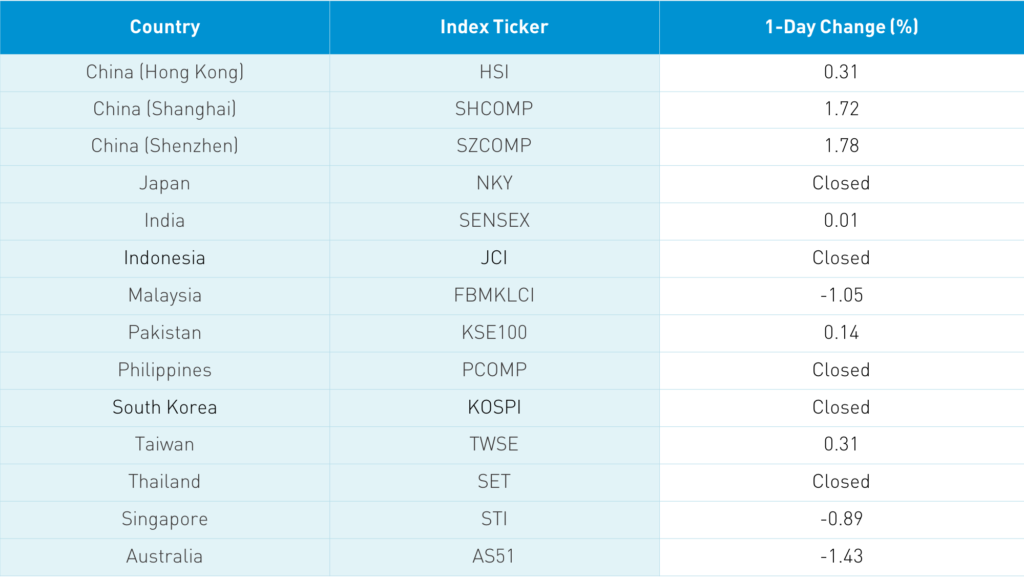

The Asian markets that were open were largely higher as China and Taiwan outperformed. News of a public rollout of a vaccine in China was a significant catalyst today for risk assets. There was also new further confirmation of the EU China investment deal, which includes a ban on forced technology transfer for access to China’s market. There was some chatter about further insurance annuities being allowed to raise their equity investment.

Hong Kong had a half-day session with the Hang Seng gaining +0.31%, led by volume leaders Tencent, which rose +0.8%, Semiconductor Manufacturing, which gained +8.33%, Meituan, which fell -1.52%, Alibaba Hong Kong, which fell -1.52%, Geely Auto, which rose +8.38%, Xiaomi, which gained +0.76%, ICBC, which was up +2.03%, energy giant CNOOC, which was off -0.42%, Ping An, which rose +1.01%, BYD, which gained +4.21%, and Greet Wall Motor, which rose +3.5%. The real action was in the Mainland with Shanghai & Shenzhen gaining +1.72% and +1.78% respectively, led by growth sectors in a strong risk-on day. Foreign investors bought $471mm of Mainland stocks while bonds rallied.

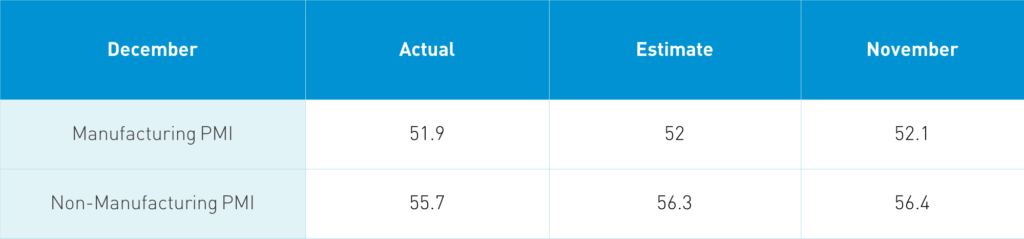

Takeaway: The “official” PMI is a large survey of predominately large companies conducted by the National Bureau of Statistics. Next week, the Caixin “private” PMIs will be released, which has its survey conducted by IHS Markit. The PMIs are a diffusion index with readings above 50 indicating growth month-over-month and under 50 a shrinking month-over-month. The Manufacturing and Non-Manufacturing PMIs look very strong across the board with new orders and export orders continuing to rise. The strong read was not a significant market mover as vaccine news and a few other events took center stage.

H-Share Update

The Hang Seng gained +0.31%/+84 index points to close at 27,231. Volume was off -31% from yesterday, which is strong considering the half-day session as only -19% below the 1-year average. Breadth saw 27 advancers and 23 decliners. The 203 Chinese companies listed in Hong Kong within the MSCI China All Shares Index gained +1.26%, led by real estate +2.49%, tech +1.88%, health care +1.72%, and industrials +1.26%, while utilities and energy were off -1.14% and -0.61% respectively. Southbound Stock Connect volumes were moderate.

A-Share Update

Shanghai & Shenzhen gained +1.72% and +1.78% to close at 3,473 and 2,329. Volume increased +13%, which is 11% higher than the 1-year average while breath was positive with 2,988 advancers and 767 decliners. The 523 Mainland Chinese companies within the MSCI China All Shares Index gained +1.96% led by discretionary +3.65%, financials +2.6%, and staples +1.9%, while utilities and energy lagged +0.26% and +0.29%. Northbound Stock Connect volumes were moderate with foreign investors buying $471mm of Mainland stocks today.

Last Night's Exchange Rates & Yields

- CNY/USD 6.53 versus 6.52 yesterday

- CNY/EUR 8.01 versus 8.00 yesterday

- Yield on 1-Day Government Bond 0.82% versus 0.37% yesterday

- Yield on 10-Year Government Bond 3.14% versus 3.12% yesterday

- Yield on 10-Year China Development Bank Bond 3.54% versus 3.53% yesterday