The Plot Thickens on NYSE ADR Delisting Reversal as Mainland China Rallies On

3 Min. Read Time

Key News

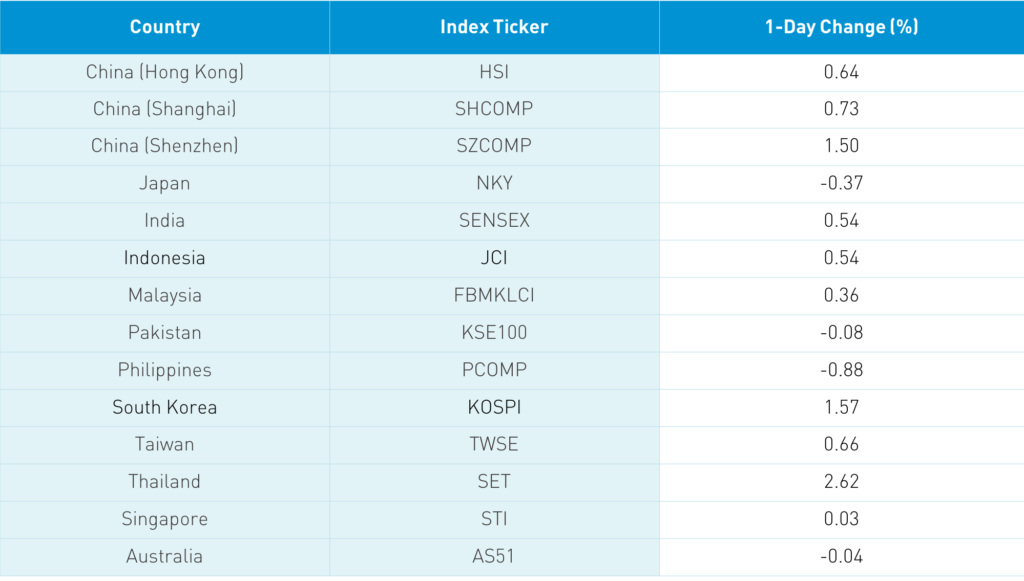

Asian equities were largely higher except for Japan, which was off. The mid-morning announcement that the NYSE would not be delisting the three US-listed Chinese telecom companies reversed early morning losses as both Hong Kong and China booked gains on strong volume.

As we mentioned yesterday, Shanghai and Shenzhen, which are predominantly owned by investors in China, have punched through resistance levels that have held several times since late June/early July. Hong Kong stocks, which are mainly owned by foreign investors, have been fairly choppy in comparison though are now making some headway.

Today was the trade date for MSCI Indexes’ removal of Executive Order stocks.

The Hang Seng gained +0.64%, led by Hong Kong volume leaders Tencent, which had another very day of Southbound inflow gaining +1.92%, Semiconductor Manufacturing, which fell -9.61% as it was removed from MSCI indexes, China Mobile, which was up +5.13% from massive buying from Southbound Connect, Alibaba Hong Kong, which fell -2.02%, Xiaomi, which gained +0.14%, energy giant CNOOC, which was up +0.14%, Meituan, which rose +1.37%, Wuxi Biologics, which fell -1.25% after a share sale, Hong Kong Exchange, which gained +3.44%, and BYD, which was up +2.87%.

Shanghai and Shenzhen gained +0.735 and +1.5%, respectively, on strong volume as growth names outperformed. It is interesting to note that MSCI deletion/Executive Order banned stock Hikvision went up +10% today as foreign investors sold -$687 million worth of Mainland stocks, which was likely driven by foreign investors removing the MSCI deletion stocks due to the Executive Order. Alcohol stocks had a good day as there was chatter that prices may be increased while health care picked up as Mainland China deals with a number of small outbreaks of coronavirus. Bonds rallied somewhat, CNY was flat, and copper pulled a James Bond gaining +0.07%.

I find the “missing” Jack Ma stories ridiculous. He is likely down in Hainan Island, China’s Hawaii, on vacation for the holidays.

For the last two years, I have pleaded with investors to avoid investing based on headlines and utilize a data-driven lens when examining China. We put forth our theory that US-China political rhetoric was a lot of shouting and showmanship, but there was little bite to the political barking. We also put forth our US-China political rhetoric gauge CNH, China’s currency that trades during US trading hours, as an indicator to watch intra-day to assess whether a given political headline had any bite to it.

Now I am going to don my face paint and conspiracy theater mask to participate in pure theatrics. Why would the NYSE reverse its decision on delisting today? The rational answer is that they had a change of heart and simply reversed their decision. For conspiracy theorists, an alternative, though unlikely, explanation is that US companies doing business in China would soon be required to reveal how much business they do with the US military. Such an announcement would have been a tit-for-tat retaliation to the US policy requiring Chinese companies to state their ties to the Chinese military. What US company does a lot of business both in China and with the US military? While simultaneously employing thousands of workers, and without China would be serious in trouble? Boeing. Could the CEO of Boeing have lobbed a call over to NYSE? Do I believe this? No, but it makes for good fun.

There is chatter that US-listed Bilibili (BILI US) will announce a Hong Kong relisting soon.

PWC is expecting nearly 500 IPOs in Mainland China this year, which will raise RMB 480B ($75B). This would be a significant increase from the 395 IPOs in 2020, which raised $72B.

I am debating whether or not to stop using the Hang Seng as a proxy for Hong Kong as, first, 50 stocks do not capture the size of the China opportunity set, and second, the MSCI China All Shares Index is a total China index including Hong Kong, Shanghai and Shenzhen, and US stocks. Let me know what you think!

H-Share Update

The Hang Seng opened lower but gained to close +0.64%/+177 index points at 27,649. Volume was up 17% from yesterday, which is 66% above the 1-year average while breadth was positive with 34 advancers and 16 decliners. The 204 Chinese companies listed in Hong Kong within the MSCI China All Shares Index gained +0.91%, led by staples +3.69%, communication +2.24%, health care +1.43%, and discretionary +0.5%, while tech fell -0.45%, materials -0.11%, and financials -0.11%. Southbound Stock Connect volumes were very high as Mainland investors bought $1.385 billion of Hong Kong stocks today as Southbound Connect trading accounted for 13% of Hong Kong turnover.

A-Share Update

Shanghai & Shenzhen gained +0.73% and +1.5% closing at 3,528 and 2,422 respectively. Volume was up 8.97% from yesterday, which is 48% above the 1-year average while breadth was off with 1,532 advancers and 2,266 decliners. The 521 Mainland Chinese companies within the MSCI China All Shares Index gained +1.8%, led by staples +4.53%, tech +3.55%, materials +2.35%, health care 1.87%, discretionary +1.22%, industrials +1.12%, and real estate +0.24%, while communication fell -0.87%, financials -0.83%, energy -0.8%, and utilities -0.8%. Northbound Stock Connect volumes high as foreign investors sold -$687mm of Mainland stocks today as Northbound Connect accounted for 7% of Mainland turnover.

Last Night's Exchange Rates & Yields

- CNY/USD 6.46 versus 6.46 yesterday

- CNY/EUR 7.92 versus 7.93 yesterday

- Yield on 1-Day Government Bond 0.65% versus 0.63% yesterday

- Yield on 10-Year Government Bond 3.13% versus 3.18% yesterday

- Yield on 10-Year China Development Bank Bond 3.53% versus 3.57% yesterday