Telecom Stocks’ Cash Redeployed in Mainland China, Week In Review

4 Min. Read Time

Week In Review

- Asian equities ended the first trading session of the new year mostly higher as investors focused on multiple positives including the newly signed EU-China investment deal, potential beneficiaries of which include autos and clean energy.

- The New York Stock Exchange (NYSE) did a “360” this week with regard to its response to President Trump’s Executive Order banning trading in Chinese telecom stocks China Mobile, China Telecom, and China Unicom. The exchange announced Tuesday it would suspend plans to delist the stocks, but reversed course Wednesday saying it would go through with delisting after receiving more detailed guidance from the Treasury Department. The about-face is causing frustration among US holders of the stocks as multiple brokerages have warned that it may become difficult to liquidate the stocks if positions are not exited before Monday, when they will be delisted.

- While security at the US capitol was breached on Wednesday, it was leaked to the Wall Street Journal that the Department of Defense is considering banning trading in Alibaba and Tencent. However, it is extremely unlikely that these companies will be delisted because doing so would risk a substantial lawsuit from the US investment community, the E-Commerce and social media firms are not defense contractors, and a new administration is due to arrive in less than two weeks.

- 2021 is already shaping up to be another banner year for Hong Kong IPOs. Online car dealer Autohome, ride sharing platform Didi, and entertainment platform Bilibili are among the firms expected to pursue IPOs in the financial center this year. Autohome and Bilibili already listed shares in the US in 2013 and 2018, respectively.

Friday’s Key News

Yesterday, MSCI and FTSE both announced they would be removing three Chinese telecom companies Hong Kong listings from their indexes effective today following the Office for Foreign Asset Control’s (OFAC) updated Q&A that explicitly named the three telecom companies, both their US ADRs and Hong Kong listings, as banned securities. The fire drill led to a last-minute kick to the curb and mass exodus by asset managers overnight as China Mobile fell -4.16% (after opening -9.93%), China Telecom fell -3.45%, and China Unicom fell -0.9%.

Per our announcement released on Monday, we removed the telecom companies’ Hong Kong securities earlier this week based on our interpretation of OFAC’s previous Q&A. Hat tip to the team for being all over this one!

The money coming out of the three telecom stocks was put back to work in South Korea, Taiwan, and Mainland China. Mainland China saw $3.189 billion in inflows today via Northbound Stock Connect, the 2nd largest inflow of foreign capital ever in a single day. The move does one thing – it makes the Hang Seng Index uninvestable for US investors, which is not a big deal since there are no Hang Seng-benchmarked ETFs in the US. Due to the settlement cycle, technically US asset managers are not supposed to own the securities on Monday, but the whole process has been such a mess that no one is going to hold managers’ feet to the fire.

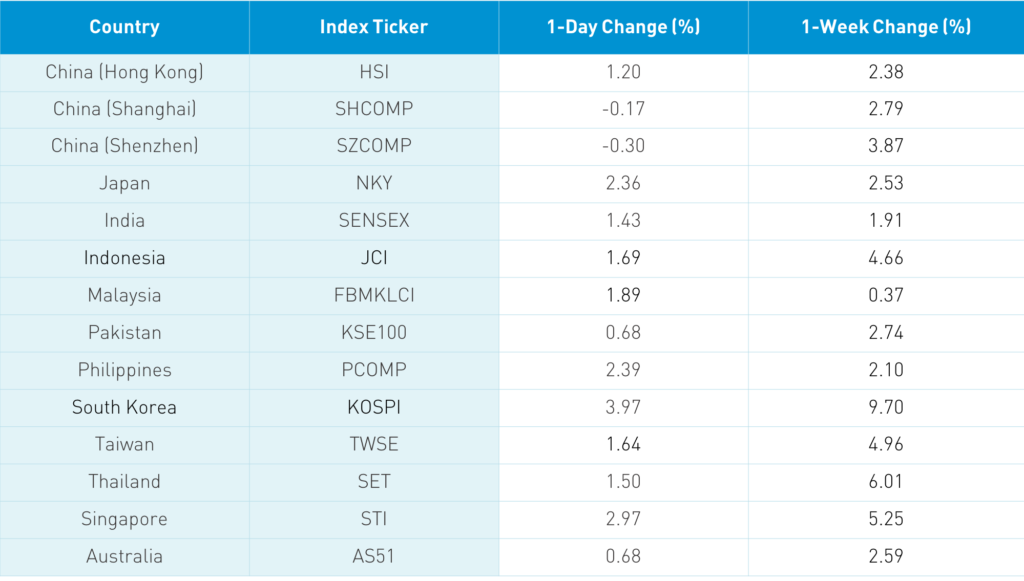

Asian equities ended a strong week on a positive note accompanied by strong volumes. Taiwan and South Korea were outliers to the upside and beneficiaries of positions in the telecom stocks being redeployed.

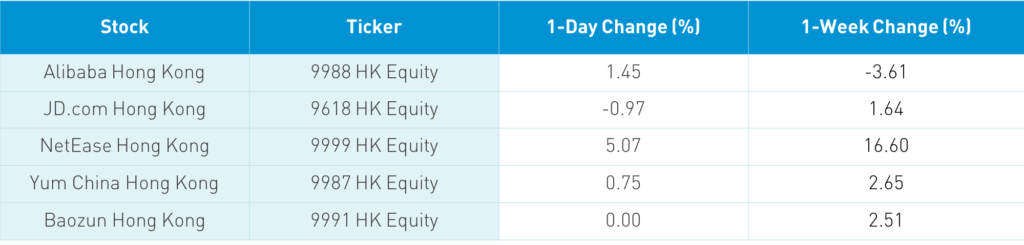

The Hang Seng gained +1.2%, led by Hong Kong volume leaders China Mobile, which fell -4.16% on 4X the average volume, Tencent, which gained +0.79%, Geely Auto, which gained +19.6% on Baidu’s EV partnership, Executive Order banned stock Semiconductor Manufacturing, which gained +10.62%, Xiaomi, which fell -0.16%, Meituan, which gained +3.25%, Alibaba HK, which gained +1.45%, China Telecom, which fell -3.45%, China Unicom, which fell -0.9%, and Hong Kong Exchanges, which gained +2.03%. It is worth noting that China Mobile was the most heavily purchased stock via Southbound Stock Connect today.

Shanghai and Shenzhen were hit with a bout of profit taking, easing -0.17% and -0.3%, respectively. Recently outperforming sectors were clipped as investors profit from the breakout we’ve been speaking about. Bonds and CNY were flat while copper had a strong day.

In one last parting gesture, the US will send UN ambassador Kelly Craft to Taiwan the week before the inauguration. I’m ready for the cult of personality to be over frankly.

December Foreign Reserves came in at $3.216 trillion versus an estimated $3.2 trillion and November’s $3.178 trillion Takeaway: Isn’t the narrative that China is blowing out of their US Treasury positions? The data says otherwise.

There has been no further chatter on Alibaba and Tencent being added to a “ban” list. As we mentioned yesterday, such a move would result in a massive pushback from the US financial industry. Even if we get a headline, I just do not see it happening. One Mainland media source noted that the media heat being applied to Alibaba is coming down.

H-Share Update

The Hang Seng Index gained +1.2%/+329 index points to close at 27,878. Volume increased +18%, which is 2X the 1-year average while breadth was stellar with 37 advancers and 14 decliners. The 200 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index gained +1.45% led by discretionary +4.17%, industrials +2.5%, tech +2.02%, staples +1.9%, real estate +1.36% and utilities +1.06%. Meanwhile, energy was off -0.61%. Southbound Stock Connect volumes were moderate.

A-Share Update

Shanghai and Shenzhen bounced around the room to close -0.17% and -0.3% at 3,570 and 2,419, respectively. Volume was off -6.45% from yesterday, which is still 33% above the 1-year average while breadth was mixed with 1,949 advancers and 1,835 decliners. The 513 Mainland Chinese stocks within the MSCI China All Shares Index fell -0.42% led by communication +3.63%, real estate +1.32%, energy +1.12%, and utilities +0.64%. Meanwhile, staples -2.58%, industrials -0.68% and financials -0.14%. Northbound Stock Connect volumes were very high as foreign investors bought $3.189 billion worth of Mainland stocks today.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.46 versus 6.48 yesterday

- CNY/EUR 7.93 versus 7.94 yesterday

- Yield on 1-Day Government Bond 0.89% versus 8.45% yesterday

- Yield on 10-Year Government Bond 3.15% versus 3.13% yesterday

- Yield on 10-Year China Development Bank Bond 3.54% versus 3.53% yesterday