Mainland Investors’ Appetite for The “All You Can Buy” Hong Kong Stock Buffet Remains Insatiable

4 Min. Read Time

Key News

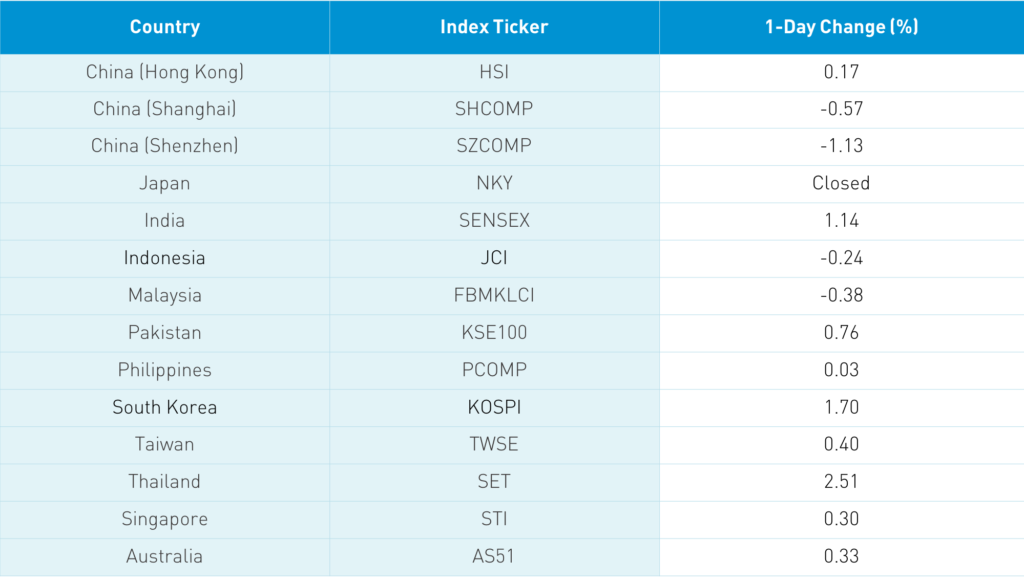

Asian equities started the week mixed on strong volumes. Japan was on holiday for Coming-of-age Day, which is a reminder to respect one’s elders.

The Hang Seng Index came off the day’s highs to close up +0.11% though technically US investors cannot own the Hang Seng due to its holding of US Executive Order banned stocks. The Chinese companies listed in Hong Kong and within the MSCI China All Shares Index fared better +0.58% led by communication, real estate financials and health care. Meanwhile, materials, staples and consumer discretionary underperformed. Hong Kong volume leaders were Tencent, which gained +3.14% on monster buying via Southbound Connect, Executive Order-banned security China Mobile, which gained +5.78%, Alibaba HK, which fell -1.43%, Geely Auto, which fell -2.56% after Baidu announced its electric vehicle joint venture, executive-order banned security Semiconductor Manufacturing, which gained +1.2%, Meituan, which fell -2.64%, Xiaomi, which gained +0.31%, energy giant executive order-banned CNOOC, which gained +0.56%, BYD, which gained +6.66%, and Ping An Insurance, which fell -1.62%.

Mainland investors bought $2.5 billion worth of Hong Kong stocks through Southbound Stock Connect, which is a very high number. Buying was focused on Tencent and China Mobile.

Shanghai and Shenzhen were off today -1.08% and -1.8%, respectively, as we had the first pullback since the two benchmarks punched above their resistance levels. The benchmarks were hit on profit taking as favored sectors were largely off except for electric vehicles (EV), which outperformed on news of NIO’s roll out of a competitor to Tesla, which was in the news for looking for a China design head. Can you imagine the resumes being sent to Tesla right now? Northbound Stock Connect volumes were elevated as foreign investors bought $137 million worth of Mainland stocks today. The dollar rallied a touch versus CNY while bonds were flat.

I could not help but notice that Investor Business Daily’s 2020 ETF performance recap included four of the KraneShares ETFs in the top ten best performing international ETFs, including the #1 performing ETF. I am dating myself by revealing my affinity for an actual paper that is delivered every Saturday morning as I love to spread it out on the kitchen table with a particular focus on the charts shown. My father worked in the paper industry so maybe I am just supporting the industry that put a roof over our head, food on the table, and paid for my college.

The Financial Times interviewed the CIOs of ten large global asset managers on market opportunities and risks in 2021. Of the ten, only two explicitly named emerging equities equity (Amundi, Invesco) though, to be fair, one mentioned global health care and tech (BlackRock), one mentioned EM fixed income (HSBC), one mentioned global equities (UBS), and one mentioned non-US equities (Vanguard). As for US equities, the comments reminded me of former Citi CEO Chuck Prince’s comments that “You keep dancing while the music is playing.” However, US valuations are rich from a historical perspective. That being said, they are appealing versus US fixed income’s yield. Most noted that a cyclical/value comeback was likely. I have no idea when or if, but, at some point, US markets will find out if the E (earnings) justifies where the P (price) has gone.

This conversation stands in contrast to an Asia-focused institutional broker’s piece this weekend that highlighted Asia’s inexpensive valuations, how far from all-time highs many Asian markets are, and how small Asia’s largest companies’ market capitalizations are versus their US equivalents. As mentioned last week, US investors’ exposure to EM stocks is somewhere around 2%, which is why the market is apt to buy what is least owned. China will be a big beneficiary of EM flows considering its weight and the number of Chinese companies within EM’s top ten.

The Financial Times also had a piece on US financial firms having to unwind structured products linked to Executive Order stocks, which is something we noted several weeks ago.

A Mainland China broker noted that China has already administered 9 million coronavirus vaccines.

The last week of December is usually quiet though in asset management it is moderately busy as funds/ETFs pay out year-end dividends. This year was different as it was all-hands-on-deck navigating the Executive Order with our Capital Markets team, James, Georgia and Jeff, along with COO Jonathan and Legal Odette and Aakash, doing heroes’ work on ensuring our compliance. With the year-end EO rush, I failed to recognize the efforts of my colleagues Henry and Lena, who help make China Last Night feasible on a daily basis. They take my gibberish and turn into something coherent under the watchful eye of our Head of Marketing Joe. I suspect they have a Rosetta Stone to help them navigate my written word. Stepping back, it is an honor and a pleasure to work with such a great team.

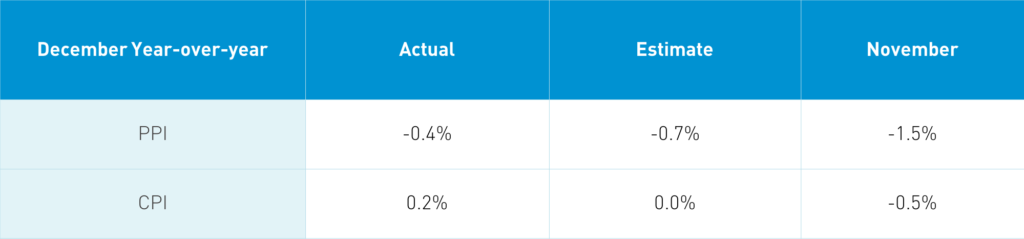

Takeaway: This was a fairly inconsequential release as far as markets are concerned. PPI was not as low as expected and China saw a pinch of CPI inflation in December after a negative CPI in November.

H-Share Update

The Hang Seng came off the day’s highs to close +0.11%/+30 index points at 27,908. Turnover was off Friday’s very high volume by -5.97%, which is still 92% above the 1-year average. The 197 Chinese companies listed in Hong Kong gained +0.58% led by communication +3.1%, real estate +2.93%, financials +0.82% and health care +0.52%. Meanwhile, materials -3.27%, staples -1.94%, discretionary -1.44%, and tech -1.24%. Southbound Stock Connect flows were high as Mainland investors bought $2.512 billion worth of Mainland stocks as Southbound Connect trading accounted for 14.7% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen sold off in the afternoon to close -1.08% and -1.8% at 3,531 and 2,375, respectively. Volume was up +7% from Friday, which is 41% above the 1-year average while breadth was dismal with only 724 advancers and 3,124 decliners. The 513 Mainland stocks within the MSCI China All Shares Index fell -1.25% led by communication +2.01%, discretionary +1.59%, and tech +0.45%. Meanwhile, energy -2.84%, materials -2.79%, staples -2.76%, industrials -2.23%, utilities -1.97% and health care -1.58%. Northbound Stock Connect volumes were high as foreign investors bought $137 million worth of Mainland stocks as Northbound Connect trading accounted for 7.1% of Mainland turnover.

Last Nights’ Exchange Rates & Yields

- CNY/USD 6.48 versus 6.47 Friday

- CNY/EUR 7.87 versus 7.92 Friday

- Yield on 1-Day Government Bond 1.14% versus 0.89% Friday

- Yield on 10-Year Government Bond 3.16% versus 3.15% Friday

- Yield on 10-Year China Development Bank Bond 3.54% versus 3.54% Friday