Hong Kong Hits 30K Resistance Level, ByteDance Rival Kuaishou Prepares For IPO, Week in Review

4 Min. Read Time

Week in Review

- Asian equities ended the trading session mostly higher on Tuesday, reversing course from Monday’s losses. Hong Kong outperformed Mainland China as money poured into the city’s markets from the Mainland via Southbound Stock Connect following yet another positive economic release coming out of the world’s second largest economy. Southbound Connect volumes were 3x the 1-year average on Tuesday. According to Bloomberg, January 2021 is shaping up to be the busiest month on record for Asian equity trading.

- Alibaba investors rejoiced Wednesday at Jack Ma’s first public appearance since October. The billionaire entrepreneur made a brief statement via livestream in conjunction with a charity event. Ma’s return to the public spotlight came as the Ministry of Commerce announced that E-Commerce sales accounted for approximately one quarter of all retail sales in China in 2020.

- TAL Education kicked off earnings season for Chinese internet companies Thursday, announcing that revenue increased by +35% YoY in the fourth quarter, beating most estimates. Meanwhile, Chinese e-cigarette maker RLX Technology listed on the New York Stock Exchange.

Key News

Asia ended a strong week with a thud as India and Hong Kong underperformed. It was a relatively quiet night though the coronavirus flare-ups in Hong Kong and China did garner some attention. It was not surprising to see health care as the top performer in both Hong Kong and Mainland China overnight. With Chinese New Year a few weeks away, there will be a big push to snuff out these outbreaks as quickly as possible.

Shanghai’s tightening of restrictions on real estate purchases was also top of mind last night as real estate was off in both markets. The South China Morning Post had an article about a crackdown on couples faking divorces so they could apply for apartment purchases separately. China’s love affair with real estate is significant as continued urbanization has made it a no-brainer investment. The upside to tightening restrictions for equity investors, however, is that a higher percentage of savings are likely to be invested in the stock market.

MSCI announced today that they are going to drop energy giant CNOOC from their indexes due to the Executive Order. According to our friends at ACG Analytics, a DC-based political/capital markets research firm, the Executive Orders are unlikely to be rolled back in the short run though they could be at some point in the future.

There was some broker chatter that Ant Group’s valuation has fallen to ~$100B from $300B, which likely weighed on Alibaba HK overnight. Southbound Connect saw another big day for volumes though the buying spree has lost a little momentum with only $1.2 billion worth of purchases overnight. That being said, Southbound Connect accounted for a very healthy 16.3% of Hong Kong turnover versus a 1-year average of 10%.

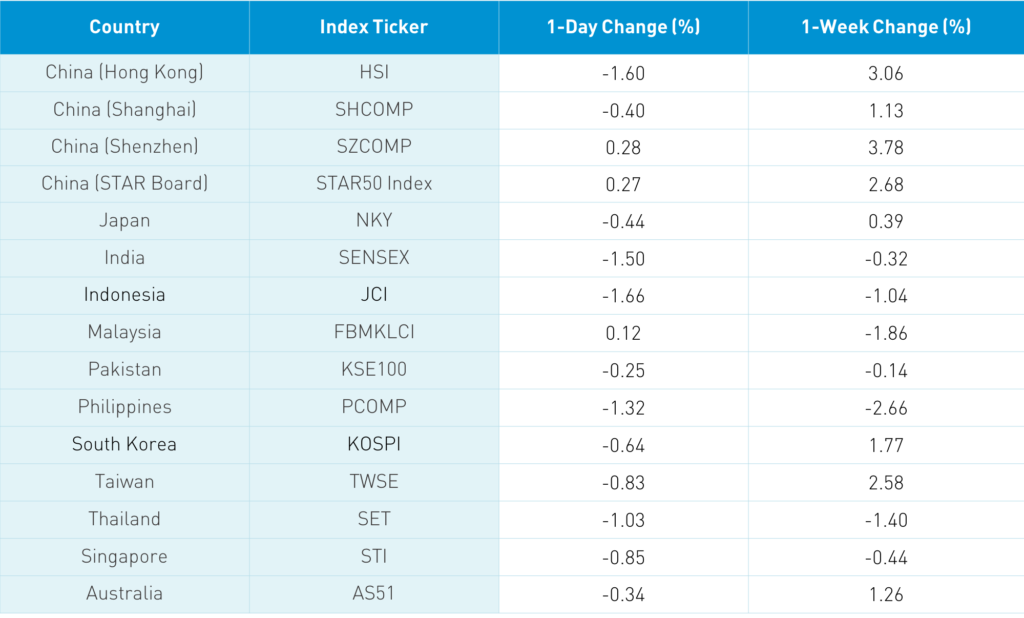

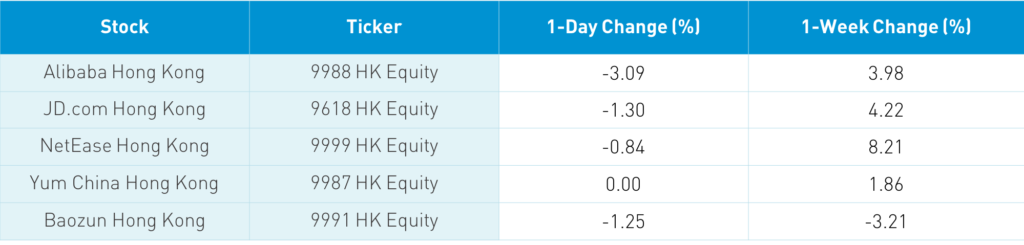

The Hang Seng drifted lower all day to close -1.6%/-479 index points at 29,447. However, the Chinese companies within the MSCI China All Shares Index were off only -0.46%. AIA weighed on the Hang Seng Index following a broker downgrade and HSBC was off in sympathy. Neither AIA nor HSBC are considered Chinese companies so not they are not in the MSCI China index, but rather they are in the MSCI Hong Kong index, which is part of developed markets. Hong Kong volume leaders included Tencent, which gained +1.25%, Alibaba HK, which fell -3.09%, Xiaomi, which fell -3.72%, Meituan, which gained +1.33%, BYD, which gained +2.5%, Semiconductor Manufacturing, which fell -2.68%, China Mobile, which fell -2.76%, CNOOC, which fell -5.57%, Ping An, which fell -2.99%, Hong Kong Exchanges, which fell -0.87%, and AIA, which fell -3.28%.

Shanghai and Shenzhen diverged -0.4% and +0.28%, respectively. Mainland markets were led by health care and discretionary sectors while clean energy plays had a strong day. Foreign investors sold $311 million worth of Mainland stocks via Northbound Stock Connect. However, they added $1.49 billion for the week, bringing the year-to-date inflow to approximately $7.22 billion. CNY was off a touch versus the US dollar.

The Wall Street Journal had a good article on the Hang Seng Index’s being overweight to “old economy” stocks, which has led to significant underperformance. While there are no Hang Seng Index ETFs in the US, the index is a big brand and popular in Asia. Not to pat ourselves on the back, but we were very focused on our “new economy” China ETFs eight years ago. I half-jokingly call ETF due diligence an oxymoron as very few people do it. A great deal of money is flowing into broad emerging market indexes as a way to play commodities’ strong performance. However, there is very little commodity exposure in broad Emerging Markets indexes. They now have a distinct growth tilt led by the largest holdings of Samsung, Taiwan Semiconductor, Alibaba, and Tencent.

ByteDance rival Kuaishou has locked in several big institutional investors for its IPO, which could happen Monday in Hong Kong, according to Bloomberg. The IPO could raise $6 billion for the company.

H-Share Update

The Hang Seng drifted lower all day to close -1.6%/-479 index points to close at 29,447. Volume was off -7.8% from yesterday, which is still 71% above the 1-year average while breadth was atrocious with only 5 advancers and 46 decliners. The 197 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index fell -0.46% led by health care +2.46%, communication +1.14% and utilities +0.93%. Meanwhile, energy -4.56%, materials -3.6%, financials -3.4%, real estate -2.33%, tech -1.32% and industrials -0.7%. Southbound Stock Connect volumes were still running at double the 1-year average as Mainland investors bought $1.208 billion worth of Hong Kong stocks today as Southbound Connect trading accounted for 16.3% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen diverged with the former falling -0.4% and the latter gaining +0.28% to close at 3,606 and 2,456, respectively. Volumes gained +2% from yesterday, which is 27% above the 1-year average. Meanwhile breadth left much to be desired with 1,037 advancers and 2,827 decliners. The 512 Chinese stocks within the MSCI China All Shares Index were off -0.2% led by health care +4.02%, discretionary +1.3% and materials +1.26%. Meanwhile, real estate -2.6%, financials -2.23%, energy -1.98%, utilities -1.55% and tech -0.92%. Northbound Stock Connect volumes were elevated as foreign investors sold -$311 million worth of Mainland stocks and Northbound Connect trading accounted for 6.2% of Mainland trading.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.48 versus 6.46 yesterday

- CNY/EUR 7.89 versus 7.86 yesterday

- Yield on 1-Day Government Bond 1.83% versus 1.97% yesterday

- Yield on 10-Year Government Bond 3.12% versus 3.13% yesterday

- Yield on 10-Year China Development Bank Bond 3.51% versus 3.52% yesterday