Asia Corrects Overnight, Kuaishou IPO on the Horizon

3 Min. Read Time

Key News

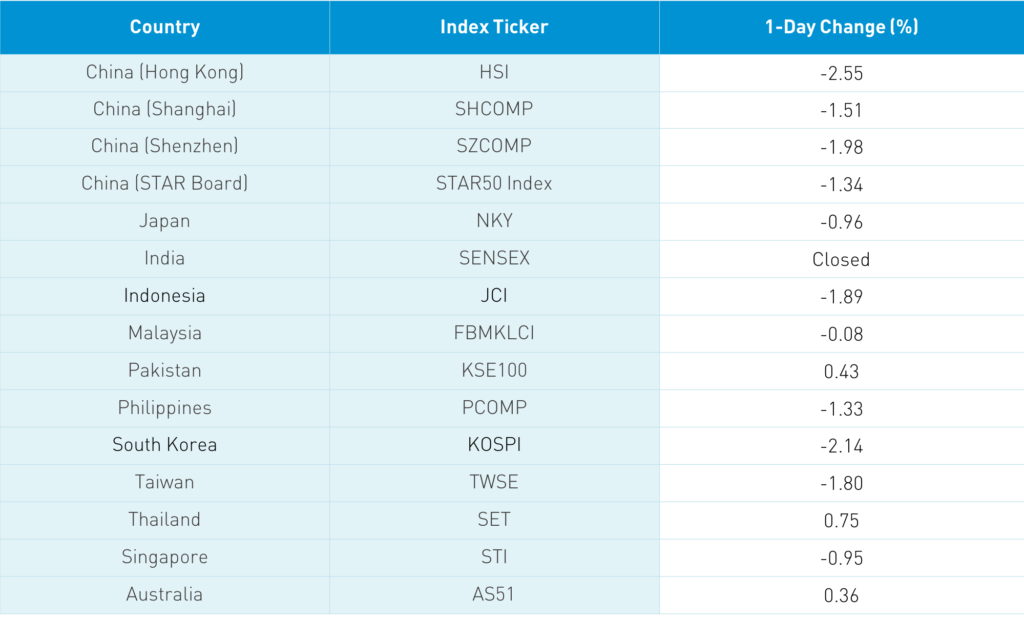

Asian equities were off in a good ol’ fashioned pullback/correction, though according to the nattering nabobs of negativity, it’s the end of the world. Yes – sell everything because the market was off today. Load up on SPAM and canned goods as well. Market corrections are painful both financially and emotionally, but ultimately a good thing. Concerns on US stimulus was cited as a factor, but warnings from PBOC advisor Ma Jun that there might be asset bubbles in China combined with an unexpected liquidity drain by the PBOC sent markets tumbling. The liquidity drain was unexpected but relatively minor. Ma Jun was likely speaking about the property market as tightening rules on real estate investment in Shanghai were reiterated.

Overlooked but far more important were comments from PBOC Governor Yi Gang, who spoke at the World Economic Forum yesterday. Gang stated that explicitly supportive policies won’t be pulled prematurely. “I think our monetary policy will continue.” Not helping was an analyst downgrade of Tencent after hitting an all-time high yesterday. We also had MSCI announcing that five more Chinese companies will be removed from their indices due to the previous administration’s Executive Orders (EO). What happened was a good ol’ fashioned bout of profit-taking after a very strong start to the year. Indexes such as the Hang Seng Index hit a big round number of 30,000, which is going to cause some selling/profit taking by those with a shorter time frame. Do most investors have exposure to these markets? I think not. Will a downdraft allow them to get invested? For sure! The market could go sideways for days, weeks, or months!

The Hang Seng Index was off -2.55% on high volumes in an inverse of yesterday when Tencent’s strong gain accounted for a healthy percentage of the index’s gain. Tencent and the Hong Kong Exchanges accounted for -196 and -114 of the index’s 767 point loss. Hong Kong’s volume leaders were Tencent, which fell -6.26%, energy giant/EO sanctioned stock CNOOC, which dropped -2.44%, Meituan, which fell -5.3%, Hong Kong Exchanges, which was off -7.23%, Alibaba Hong Kong, which fell -1.78%, China Mobile, which dropped -3.5%, Xiaomi, which was off -0.49%, BYD, which fell -6.11%, Geely Auto, which fell -1.18%, and Semiconductor Manufacturing, which gained +0.5%. It is worth noting that Tencent and to a lesser degree Meituan saw very heavy buying from Mainland investors via Southbound Connect. Clean energy was one of the few bright spots as outperforming sectors were the ones hit the hardest in Hong Kong and China. Shanghai & Shenzhen were off -1.51% and -1.98% respectively on volume off from yesterday but still high. Foreign investors sold -$547mm of Mainland stocks today while CNY appreciated versus the US $.

MSCI announced that it will drop five Chinese stocks from their indices. It is disconcerting that the anarchy and chaos imposed by the previous administration on the US financial industry hasn’t been addressed. I am aware of two global asset managers violating US sanctions by not selling the EO sanctioned securities in their ETFs.

President Xi’s comments at the World Economic Forum sounded like an olive branch offering to me as he noted the risks of a “new Cold War.” As the WSJ reported last Friday, China wants to send a senior diplomat to DC to facilitate a Biden-Xi summit. There are some easy wins out there, for instance on climate change.

Kuaishou’s IPO appears to be moving quickly as the order book will be filled tomorrow ahead of schedule.

Industrial profits will be reported tonight.

H-Share Update

The Hang Seng closed -2.55%/-767 index points at 29,391. Volumes were off -2.78%, which is still 2X the 1-year average while breadth saw 13 advancers and 37 decliners. The 197 Chinese companies listed in Hong Kong within the MSCI China All Shares Index were off -3.44%, with staples the only sector in the green +0.1%, while communication fell -6.14%, discretionary -4.1%, health care -3.26%, energy -2.3%, materials -1.84%, financials -1.67%, tech -1.56%, utilities -1%, and real estate -0.88%. Southbound Stock Connect volumes and flows were strong.

A-Share Update

Shanghai and Shenzhen were off -1.51% and -1.98% respectively to close at 3,569 and 2,414. Volume was off -16% from yesterday, which is still 16% above the 1-year average. The 512 Mainland Chinese companies within the MSCI China All Shares Index were off -1.83%, with utilities up +0.54%, energy +0.41%, and real estate +0.29%, while health care fell -3.01%, industrials -2.39%, tech -2.27%, communication -2.15%, discretionary -1.88%, financials -1.69%, materials -1.65%, and staples -1.24%. Northbound Stock Connect volumes were high as foreign investors sold -$547mm of Mainland stocks today.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.47 versus 6.48 yesterday

- CNY/EUR 7.85 versus 7.88 yesterday

- Yield on 10-Year Government Bond 3.16% versus 3.13% yesterday

- Yield on 10-Year China Development Bank Bond 3.55% versus 3.53% yesterday

- China's Copper Price -0.03% Overnight