Kuaishou’s IPO Goes GameStop while CSRC Looks to Resolve Audit Issue, Week in Review

4 Min. Read Time

Week in Review

- On Monday, Kuaishou secured several high-profile cornerstone investors who are buying $2.45B of the $5.4B IPO. Investors include Capital Group (American Funds), Temasek and GIC (Singapore sovereign wealth funds), Invesco, Fidelity, CPPIB (Canadian pension fund), Morgan Stanley, and Abu Dhabi Investment Authority (sovereign wealth fund).

- Asian equities were off Tuesday in a good ol’ fashioned pullback/correction, which is not the end of the world. Concerns on US stimulus, warning of an asset bubble, and an unexpected liquidity drain by the PBOC are cited as factors.

- MSCI reversed its decision on Wednesday to drop five Chinese companies from their indexes as they will make an announcement today.

- Apple reported on Thursday outstanding quarterly results. What jumps out is the sharp increase in Greater China revenue from $13.578B to $21.313B – a 61% growth year-over-year!

Key News

Asian equities were off with South Korea, Japan, and Taiwan underperforming on chatter that foreign investors are turning extra cautious as US equity concerns reverberate globally. Hong Kong and China were not immune from this, though the bigger driver of market action intra-day were rumors that lending rates are going to be raised. The PBOC denied this rumor at the day’s end, which led to a small rebound in Mainland China. The PBOC finally injected liquidity into the financial system for the first time this week in advance of Chinese New Year. China will normalize (ie. remove/ease stimulus both monetary and fiscal) over the year, but I don’t see this as a significant headwind for stocks. It is expected that there won’t be as much travel this year due to coronavirus flare-ups in northern China. How do brokers know this? One mentioned studying Baidu’s version of Google Trends to ascertain the number of searches related to travel.

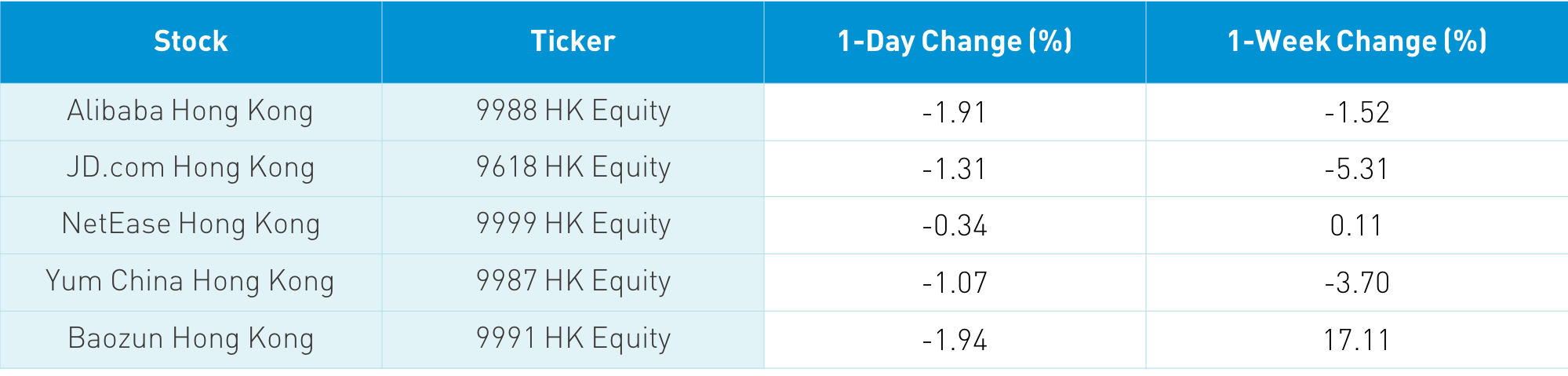

Southbound Stock Connect flows were strong (again) as Mainland investors bought a very healthy $1.607mm of Hong Kong stocks with Tencent gaining $657mm of inflow and Meituan $147mm of inflow. The Hang Seng Index was off -0.94% though the Chinese companies listed in Hong Kong within the MSCI China All Shares Index were off -0.55%. Hong Kong volume leaders were Tencent, who pulling a James Bond rose +0.07% in advance of Kuaishou’s IPO next Friday in Hong Kong, Alibaba Hong Kong, which was off -1.91% despite that earnings will be released next Tuesday before the US open, Meituan, which rose +0.06%, Geely Auto, which fell -3.9%, Xiaomi, which dropped -0.34%, Ping An Insurance, which fell -2.25%, Hong Kong Exchanges, which rose +0.81%, BYD, which gained +0.59%, China Mobile, which fell -1.25%, and Semiconductor Manufacturing. Which fell -0.94%.

Shanghai and Shenzhen were off -0.63% and -0.75% respectively, though the STAR Board gained +0.03%, and the Mainland stocks within the MSCI China All Shares Index gained +0.24%. CNY did strengthen versus the US $ overnight, which helped appreciate the value of renminbi-denominated stocks. Alcohol stocks were strong overnight as investors anticipate that Chinese New Year celebrations will benefit Kweichow Moutai, which rose +1.35%, and Wuliangye Yibin, which rose +1.8%. Travel and tourism stocks were strong as well. Growth sectors such as EV and semis were soft in profit-taking. Foreign investors were buyers of Mainland stocks today via Northbound Stock Connect buying +$394mm. For the week foreign investors sold $1.043B of Mainland stocks this week. Chinese bonds rallied today while copper was off.

China’s version of the SEC is the CSRC. They held their annual conference outlining their goals for 2021, which were on improving reporting, regulations, and opening up. It is important to note that they stated to “actively promote cross-border audit and supervision cooperation.” My interpretation of this is very clearly aimed at resolving the long-running PCAOB issue of reviewing the audit books of US-listed Chinese companies. Former SEC Chairman Jay Clayton provided a path for compliance for the companies as the vast majority of US-listed Chinese companies are audited by the Mainland arms of the Big Four US accounting firms. The China arms audit the China operations of US-listed companies. In November, the CSRC noted that they had reached out to the PCAOB in August to try to resolve this issue, but nobody called them back! At a bare minimum, there will be dialogue and communication going forward, which will allow this issue among others to be resolved.

Vice Foreign Minister Le Yucheng spoke at a conference yesterday extending an olive branch to resolve US-China political tensions. In his speech, he noted that President Biden has visited China four times, which I wasn’t aware of. He articulated four Rs needed to get the relationship back on track: respect, reversal, renewal, and responsibility.

Tencent-backed Kuaishou Technology (1024 Hong Kong) will list at the top of its listing range HK $115 apiece, raising US $5.417B and valuing the company at US $60.9B according to Reuters. Amazingly, the IPO is oversubscribed by 1,200 times with 1.4 million investors participating! Once the non-redacted IPO prospectus is released, I’ll do a deep dive.

I’ve started using Grammarly’s great spelling correct app. One downside: I’ve never used so many hyphens.

H-Share Update

The Hang Seng’s morning gains were faded in the afternoon, falling -0.94%/-267 index points to close at 28,283. Volume was off -11% from yesterday, which is still 72% above the 1-year average while breadth had only 9 advancers and 43 decliners. The 196 Chinese companies listed in Hong Kong within the MSCI China All Shares Index lost -0.55%, with industrials gaining +1.05%, healthcare +0.4%, and communication +0.02%, while utilities fell -2.59%, real estate -2.39%, energy -1.75%, financials -1.61%, materials -1.49%, and tech -0.35%. Southbound Stock Connect volumes were high but not insane as Mainland investors bought $1.607mm of Hong Kong stocks as Southbound Connect trading accounted for 14.8% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen were off -0.63% and -0.75% closing at 3,483 and 2,335 respectively. Volumes were up +3% from yesterday, which is 9% above the 1-year average while breadth had 1,007 advancers and 2,843 decliners. The 511 Mainland Chinese companies within the MSCI China All Shares Index gained +0.24%, led by staples +1.27%, discretionary +0.75%, healthcare +0.28%, and financials +0.18%, while energy fell -1.72%, real estate -1.18%, and tech -0.38%. Northbound Stock Connect volumes were high as foreign investors bought $394mm of Mainland stock as Northbound Stock Connect trading accounted for 7.2% of Hong Kong trading.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.43 versus 6.47 yesterday

- CNY/EUR 7.81 versus 7.83 yesterday

- Yield on 10-Year Government Bond 3.18% versus 3.20% yesterday

- Yield on 10-Year China Development Bank Bond 3.59% versus 3.61% yesterday

- China's Copper Price -0.09% Overnight