No Rest For Hong Kong Investment Bankers As Kuaishou IPO Skyrockets

4 Min. Read Time

Week in Review

- The PBOC, China’s central bank conducted RMB 98 billion worth of open market operations Monday, easing fears of a liquidity crunch in February and contributing to the appreciation of growth stocks. However, the central bank tightened financial conditions slightly later in the week, affirming its neutral policy stance for 2021.

- Xiaomi filed a complaint against the executive order banning Americans from trading in its shares in a DC federal court Monday. The consumer technology company denies any affiliation with China’s military.

- Alibaba reported Tuesday that its revenues increased by 37% YoY to $33.88 billion in the fourth quarter of 2020, beating an estimate of $33.5 billion. However, the positive release was overshadowed by Jack Ma’s exclusion from a list of Chinese entrepreneurs published by the Shanghai Securities News.

- The Caixin Services PMI, which covers small and medium-sized enterprises, came in at 52.0 for January versus December's 56.3. The low release was likely influenced by seasonality, shutdowns, and an exceptionally cold winter in China this year, which poses difficulties for logistics.

Friday’s Key News

Tencent-backed ByteDance rival Kuaishou Technology (1024 HK) ripped +160% in its Hong Kong IPO today in the second-best IPO performance ever behind Alibaba’s +193% gain back in 2007 (BABA went private before going public again in 2014). The company raised $5.4B from investors. Yesterday we did a deep dive on the company, which you can access here.

The value traded in Kuaishou was nearly 3X the second most traded stock worth $4.84 billion as 119 million shares traded hands today. Several brokers noted the company’s market cap of $158 billion is more than three Hong Kong banks, HSBC, Standard Chartered, and Hang Seng, combined! The Hong Kong IPO frenzy is going to continue with rumors overnight that Tencent Music Entertainment is working on a Hong Kong IPO along with Baidu. Bloomberg noted that ByteDance might want to take advantage of the valuation given to Kuaishou and pursue an IPO itself, similar to when Uber went public after seeing Lyft’s success at doing so.

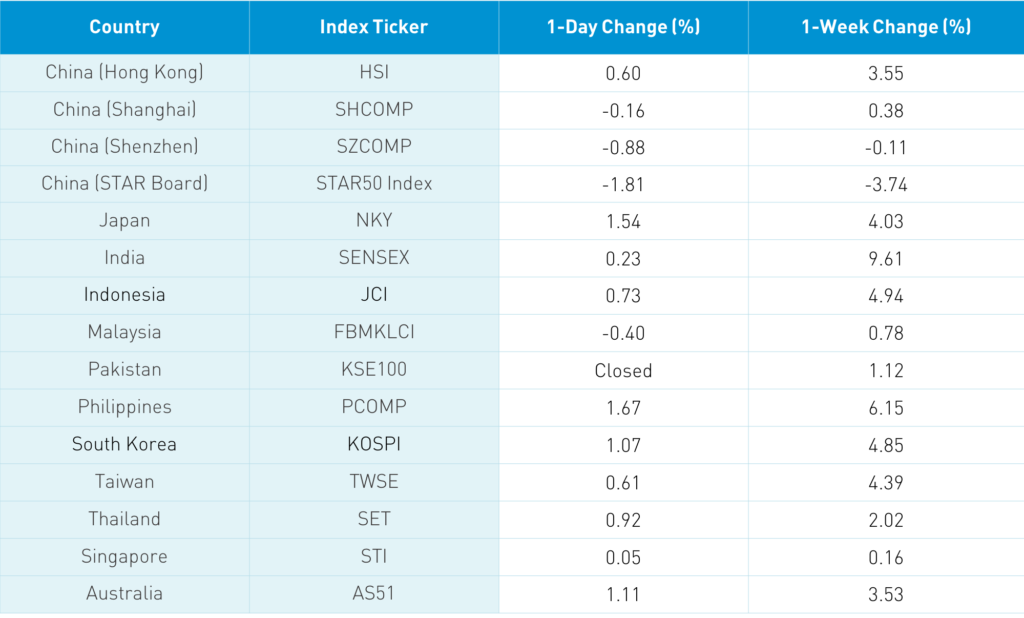

Asian equities were largely higher today though Mainland China was off, continuing a similar pattern all week. However, if you look below, the Mainland was flat for the week. A Mainland bond broker noted the unusual phenomenon of both Mainland stocks and bonds going down this week, indicating some profit-taking/cash being raised in advance of Chinese New Year next week. Health care had a strong day on reports demand for PPE is leading to rising prices.

The Hang Seng Tech Index and the STAR Board were off today as Semiconductor Manufacturing was off -4.77% in the Mainland and -10.62% in Hong Kong. The company reported that net income doubled in Q4 though its revenue in Q1 2021 of 5% to 9% disappointed investors. The company cited its inability to buy US technology as problematic. However, many investors were spared the pain of today’s drawdown as they cannot hold the stock anyway due to the Executive Order.

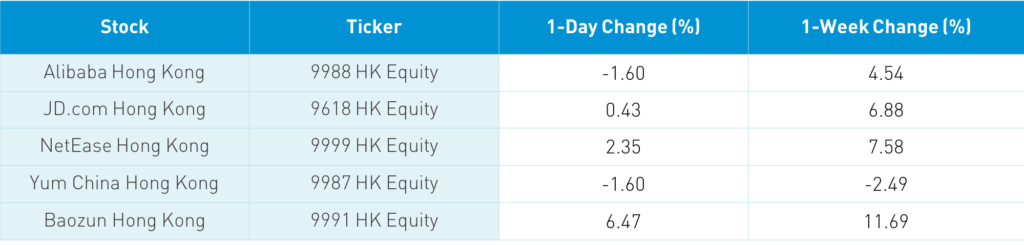

The Hang Seng rose +0.6% while the Hong Kong-listed Chinese companies within the MSCI China All Shares Index pulled a James Bond gaining +0.07%. Hong Kong volume leaders were Kuaishou, which gained +160%, Tencent, which fell -0.34% despite more buying from Mainland investors via Southbound Connect, Xiaomi, which fell -1.27% on Southbound selling and chatter about issues running Google apps on their smartphones, Semiconductor Manufacturing (SMIC), which fell -10.62%, Alibaba HK, which fell -1.6%, Meituan, which gained +0.1% on modest Southbound buying, GCL-Poly, which fell -2.15%, Hong Kong Exchanges, which gained +1.17% after buying 7% of the Guangzhou Futures Exchange, Ping An Insurance, which fell -0.65%, and Macau casino Galaxy Entertainment, which gained +6.29%.

Shanghai and Shenzhen sold off into the close to finish -0.16% and -0.88% lower, respectively, on Mainland profit-taking. Meanwhile, STAR Board was off -1.81% due to SMIC. Chatter on the PBOC pulling liquidity has died down as the PBOC is simply not injecting as much liquidity as it did pre-Chinese New Year. Travel restrictions are likely to dampen the historical travel frenzy at this time of the year due to coronavirus flare-ups. It was a big day for foreign investors as they bought $1.297 billion worth of Mainland stocks via Northbound Stock Connect. Foreign investors bought a total of $3.915 billion worth of Mainland stocks this week, a big one for inflows. CNY was a touch weaker, bonds were off, and copper was up.

Alibaba’s bond deal is going well, demonstrating that enthusiasm for the company has not diminished as the company received $30 billion worth of orders for its $5 billion offering. The strong demand pushed yields down significantly, which is great for the company. The offering begs the question of why does the company need the cash? It believes its shares are undervalued and has earmarked lucrative investments, for which it needs capital.

The Hong Kong Exchanges deal with the Guangzhou Futures Exchange is interesting to me as the exchange operator has begun listing MSCI-benchmarked futures in Hong Kong. I believe listing MSCI China A futures would be difficult in Hong Kong but makes sense to do on the Mainland. Bond investors can hedge the currency risk of their Chinese bonds if they are held in China. Why not allow investors to go long single stocks and hedge market risk via an MSCI China A futures in China? This makes sense to me as it would prevent naked shorting on the Mainland.

H-Share Update

The Hang Seng gained +0.6%/+175 index points to close at 29,288. Volume was flat/-0.1%, which is 68% above the 1-year average while breadth was decent with 30 advancers and 21 decliners. The 196 Chinese companies within the MSCI China All Shares Index pulled a James Bond gaining +0.07% led by real estate +1.6%, staples +1.06%, and financials +0.51% while tech -0.88%, industrials -0.58%, and communication -0.35%. Today’s Southbound Connect volumes were high from a historical basis, but have begun to come down. Mainland investors bought a healthy $1.053 billion worth of Hong Kong stocks today as Southbound trading accounted for 14.6% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen fell into the close, off -0.16% and -0.88% to close at 3,496 and 2,332, respectively. Volume was off -5.61% from yesterday, which is still 1% above the 1-year average. The 511 Mainland Chinese companies within the MSCI China All Shares Index were off -0.18% with health care +2.52%, real estate +1.88%, and financials +1.34%. Meanwhile, materials -4.22%, energy -1.83%, tech -1.65%, industrials -1.51% and communication -0.85%. Northbound Stock Connect volumes were elevated as foreign investors bought a very healthy $1.297 billion worth of Mainland stocks and Northbound Connect trading accounted for 6.7% of Mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.47 versus 6.47 yesterday

- CNY/EUR 7.77 versus 7.75 yesterday

- Yield on 1-Day Government Bond 2.01% versus 2.10% yesterday

- Yield on 10-Year Government Bond 3.22% versus 3.23% yesterday

- Yield on 10-Year China Development Bank Bond 3.68% versus 3.68% yesterday

- China’s Copper Price +0.47% overnight