Anti-Climactic Release of Anti-Monopoly Law Asks Where’s the Beef?

2 Min. Read Time

Key News

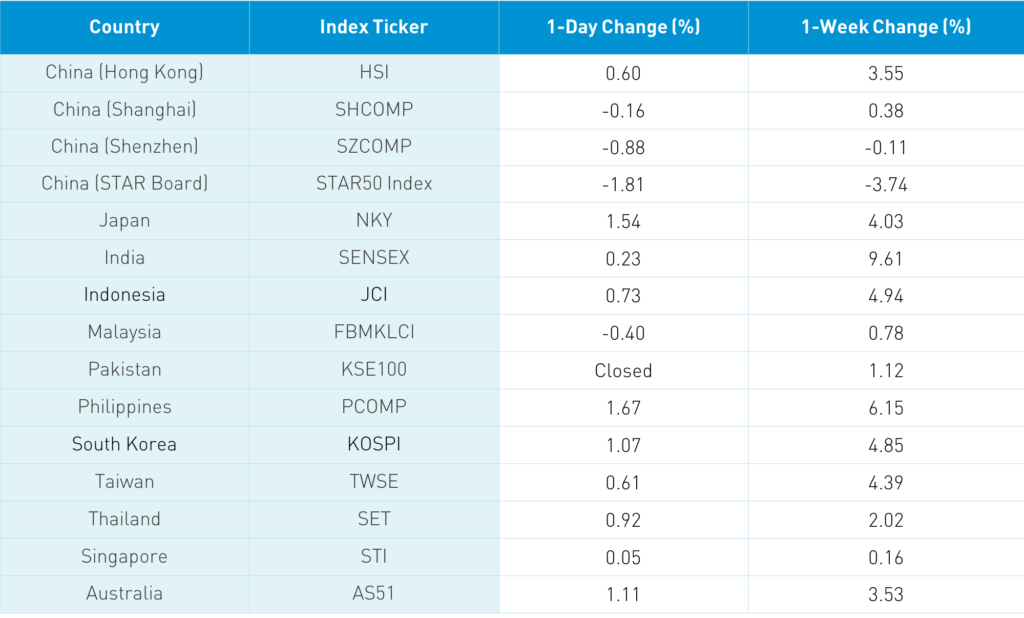

Asian equities had a strong day as Japan and India outperformed while Mainland China underperformed. Meanwhile, South Korea hiccupped on news that the country’s ban on short-selling ban will be extended until May. It was reported that the Bank of Japan’s equity ETF holdings now total $440 billion, a confirmation of the power of passive.

The weekend release of China’s anti-monopoly rules from the State Administration for Market Regulation (SAMR) was anti-climactic and few seem to be reporting on it. We knew from the November draft release that forcing exclusivity for merchants and mobile payments was coming to an end. As the old Wendy’s commercial asked, where’s the beef?

The PBOC released liquidity into the financial system in advance of Chinese New Year. Repo rates have come down as fears of illiquidity are alleviated. Foreign investors bought $1.228 billion worth of Mainland stocks today through the Northbound Connect trading venue. This was the third day of over $1 billion in inflow following three consecutive days of, on average, $500 million in inflows. Many investors have been underweight China due to US-China political rhetoric and, at the same time, many are underweight emerging markets. Broad emerging markets hold a lot of China. These flows might indicate these underweights are being raised.

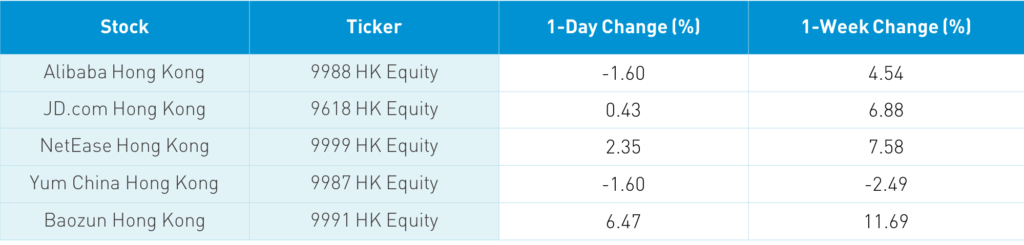

The Hang Seng Index opened higher and slowly slid to close up only +0.11% though the broader market did well as the Chinese stocks listed in Hong Kong and within the MSCI China All Shares Index gained +0.41%. Hong Kong volume leaders were Tencent, which gained +0.48%, Kuaishou Technology, which gained +1%, Meituan, which gained +1.25%, Xiaomi, which fell -0.18%, Alibaba HK, which fell -0.62%, vaping stock Smoore International, which fell -4.05%, Semiconductor Manufacturing, which fell -3.28%, Ping An, which fell -0.82%, Hengen Network, which gained a whopping +49.12%, and Hong Kong Exchanges, which gained +0.82%. However, trading was relatively quiet overnight as today was the last day for Southbound Stock Connect until February 18th. Shanghai, Shenzhen and the STAR Board gained +1.03%, +1.21% and +1%, respectively. Meanwhile, the Mainland stocks within the MSCI China All Shares Index gained +2.02%.

The Shenzhen Stock Exchanges announced it would merge its Small & Medium Enterprise Board with the main board.

There was continued chatter on the opening of China’s carbon emissions trading system, which led to a strong day in the space.

Bonds were off while CNY appreciated slightly versus the US dollar while copper had a strong day.

H-Share Update

The Hang Seng opened higher but eased off the day’s highs to close +0.11%/+30 index points at 29,319. Volumes were off -22% from Friday though 31% above the 1-year average while breadth was weak with 23 advancers and 25 decliners. The 196 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index gained +0.41% led by materials +3.69%, discretionary +1.44% and real estate +0.7% while utilities -0.82%, energy -0.47% and financials -0.33%. Mainland investors bought $1.494 billion worth of Hong Kong stocks today as Southbound Connect trading accounted for 16.9% of Hong Kong turnover.

A-Share Update

Shanghai & Shenzhen had a strong day, gaining +1.03% and +1.21% to close at 3,532 and 2,360, respectively. Volumes were off -9.4% from Friday, which is 92% of the 1-year average while breadth was decent with 1,947 advancers and 1,829 decliners. The 511 Mainland stocks within the MSCI China All Shares Index gained +2.12% led by materials +5.16%, industrials +3.66%, health care +2.37%, energy +2.29%, discretionary +2.1%, tech +1.45% and communication +1.19%. Northbound Stock Connect volumes were elevated as foreign investors bought $1.228 billion worth of Mainland stocks. Northbound Connect trading accounted for 7.1% of Mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.45 versus 6.47 yesterday

- CNY/EUR 7.77 versus 7.77 yesterday

- Yield on 1-Day Government Bond 1.90% versus 1.80% yesterday

- Yield on 10-Year Government Bond 3.24% versus 3.22% yesterday

- Yield on 10-Year China Development Bank Bond 3.70% versus 3.68% yesterday