Real Estate and Clean Tech Rise, Bilibili, Vipshop, and NetEase Report

4 Min. Read Time

Key News

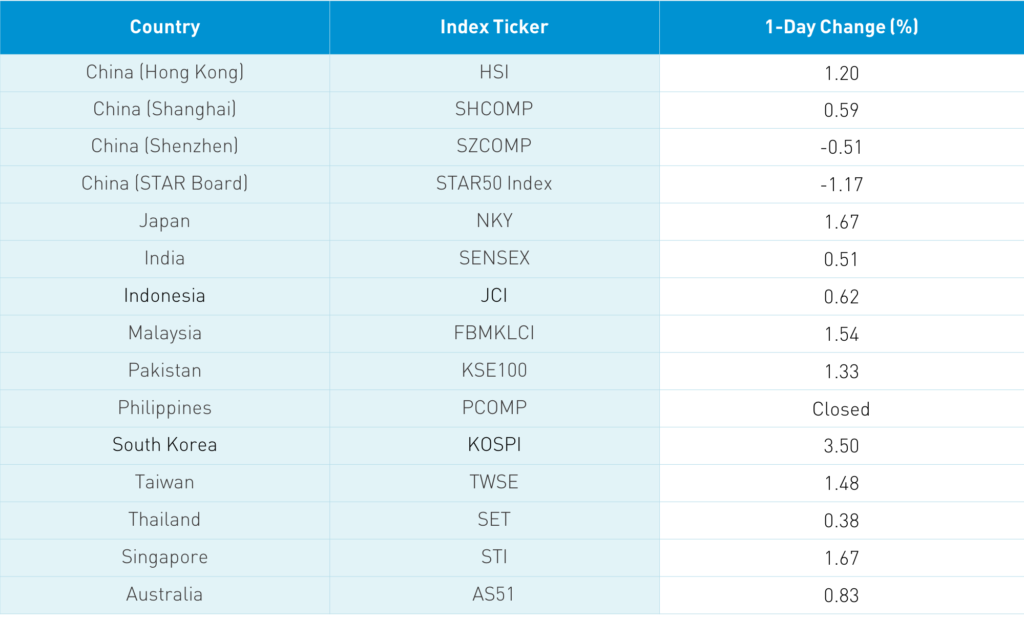

Asian equities rebounded overnight after the US market’s 180 reversal yesterday following Fed Chair Powell’s comments on the economy and inflation. Goldman Sach’s co-head of Asia-Pacific strategy, Tim Moe, called Hong Kong’s recent fall “a healthy correction” driven by the Hong Kong stamp tax increase as “over-extended positioning, some of the heavily-owned favorite stocks sold off” with “further upwards gains” possible.

Real estate stocks ripped on news that 22 cities will revamp how they auction off urban land for development. Brokers noted the low weight of real estate in investors’ portfolios and compelling valuations leading to sharp gains in Hong Kong (+9.06%) and in the Mainland (+7.43%).

Clean energy names had a strong day following confirmation that clean energy policies will be articulated in the coming policy meetings in March. Investors appear to be front-running the potential positive policies.

Health care had a good day as vaccine rollouts in China and globally continue.

Following their US equivalents, financials gained today as a steeper yield curve is advantageous. Banks pay depositors based on low short-term yields while lending at higher long rates.

The Hang Seng Index rebounded +1.2% while the broader Hang Seng Composite +1.69%. Hong Kong volume leaders were Tencent, which gained +0.66%, Hong Kong Exchanges, which fell -1.77% post-stamp tax announcement, Meituan, which rose +1.26%, Alibaba Hong Kong, which was up +0.25%, Ping An, which gained +2.63%, Xiaomi, which was flat, China Mobile, which was flat, GCL-Poly Energy, which gained +16.46%, BYD, which rose +1.89%, and HSBC, which gained +3.36%. Southbound Connect trading saw a net buying of $219mm of Hong Kong stocks with Tencent as a key beneficiary while Meituan was sold.

Mainland China diverged as Shanghai rose +0.59% but Shenzhen and STAR Board fell -0.51% and -1.17% respectively as real estate, commodity, and clean energy outperformed. Foreign investors sold a small amount of Mainland stocks -$113mm via Northbound Stock Connect. CNY appreciated a touch versus the US dollar, bonds sold off while copper continued its hot streak higher.

The Wall Street Journal had an article about Vanguard’s efforts in China, highlighting their robo partnership with Ant Group.

Tomorrow is the trading day for MSCI’s quarterly index review. Hang Seng’s announcement on index changes for the Hang Seng Index is also due for tomorrow and all eyes are on Kuaishou.

Online video and entertainment company Bilibili (BILI US) reported Q4 results after the US close yesterday. Investors are likely to focus on the strong top-line revenue growth and increase in the number of users. As a growth company trying to gain market share, investors may overlook the reality that the company is unprofitable. Kuaishou’s recent IPO likely helps the company from a comparative perspective. If you want to feel old, take a look at this company! Bilibili is focused on Gen Z+, those born between 1995 and 2009, providing short video, anime, and online video games. My colleague Derek, who is from China, in their demographic focus, and a fan of the company’s offerings, says that Bilibili is not a company, but a culture.

Percent change is year over year (Q4 2020 versus Q4 2019).

- Revenue increased 91% to RMB 3.840.1B ($588.5mm) versus analyst expectations of RMB 3.674B

- Revenue breakdown: Mobile Games +30% to $173.1mm, Live Broadcasting +30% to $191mm, Advertisting +149% to $110.7mm, E-commerce +168% to $113.5mm

- Monthly active users +55% to 202mm while mobile monthly active users 61% to 186.5mm

- Cost of Revenues increased 80% to $443.8mm

- Gross profit +137mm to RMB 944.1mm ($147.7mm)

- Total Operating Expenses +126% to RMB 1.847.5mm ($283.1mm)

- Adjusted Net loss RMB -665mm versus an estimated loss of RMB 730mm

- Adjusted EPS was a loss RMB 1.88 ($0.29) versus an estimated loss of RMB -2.06

- Q1 2021 revenue forecast between RMB 3.7B and RMB 3.8B

Online discount retailer Vipshop (VIPS US) reported Q4 financial results before the US market open. The results look very strong to me as the company grew both top line and bottom line. The icing on the cake was a strong Q1 forecast. The company was able to grow without increasing expenses. Hat tip to management!

Percent change is year over year (Q4 2020 versus Q4 2019).

- Revenue increased +22% to RMB 35.8B ($5.5B) versus analyst estimate of RMB 34.8B

- Gross merchandise Value +25% to RMB 59.3B from RMB 47.6B

- Active customers +37% to 53mm from 38.6mm

- Gross profit +12.1% to RMB 7.8B ($1.2B)

- Operating Expenses were flat YoY at RMB 5.4B ($830mm)

- Adjusted Net Income +33.4% to RMB 2.6B ($394mm) versus analyst estimates of RMB 2.143B

- Adjusted EPS RMB 3.51 versus analyst estimates of RMB 3.12

- Q1 Revenue forecast is between RMB 27.2B and RMB 28.2B which would be an increase between 45% to 50% YoY

Online gaming company NetEase (NTES US, 9999 Hong Kong) reported earnings before the US market opened this morning. The company’s spin-off Youdao (DAO US) helped the top line but hurt the bottom line. Analysts will strip out DAO’s effect on NTES, which will make the results more favorable than they appear at first look. Most important for Netease is the strong growth in its core gaming business.

Percent change is year over year (Q4 2020 versus Q4 2019).

- Revenues +25.6% to RMB 19.8B ($3B) versus analyst estimates of RMB 19.673B

- Mobile games accounted for 72.4% of revenue

- Gross margin was flat YoY at 63.1%

- The company’s tax rate increased

- Adjusted Net Income RMB 1.597B ($244mm) versus analyst estimates of RMB 1.7B

- Adjusted EPS RMB 2.34 ($0.36) versus analyst estimates of RMB 2.49B

- The company will a dividend of $0.06 a share while the board approved a stock repurchase plan.

H-Share Update

The Hang Seng Index gained +1.2% closing at 30,074. Volume was off -27% from yesterday, though still 173% of the 1-year average while breadth saw 37 advancers and 13 decliners. The 196 Chinese companies listed in Hong Kong within the MSCI China All Shares Index gained +1.75%, led by real estate +9.06%, materials +3.73%, energy +2.56%, utilities +2.32%, financials +1.9%, health care +1.87%, industrials +1.66%, discretionary +1.23%, tech +1.05%, and communication +0.7%. Southbound Connect volumes were elevated though off from the hyper levels pre-Chinese New Year. Mainland investors bought $219mm of Hong Kong stocks today as Southbound trading accounted for 13.5% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen had a choppy session as the former gained +0.59% and the latter fell -0.51% closing at 3,585 and 2,335 respectively. Volumes were off -12.5% which is 106% of the 1-year average. The Mainland Chinese stocks within the MSCI China All Shares Index gained +0.24% led by real estate +7.43%, financials +1.55%, utilities +0.95%, energy +0.71% while staples -1.29%, tech -1.09%, and communication -0.57%. Northbound Stock Connect volumes were elevated as foreign investors sold -$113mm of Mainland stocks today as Northbound trading accounted for 6.6% of Mainland turnover.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.46 versus 6.46 yesterday

- CNY/EUR 7.89 versus 7.83 yesterday

- Yield on 1-Day Government Bond 1.61% versus 1.42% yesterday

- Yield on 10-Year Government Bond 3.27% versus 3.26% yesterday

- Yield on 10-Year China Development Bank Bond 3.74% versus 3.74% yesterday

- Copper price +2.50% overnight