PMIs Highlight Commodity Needs, Hang Seng Index Revamp Embraces New Economy

4 Min. Read Time

Key News

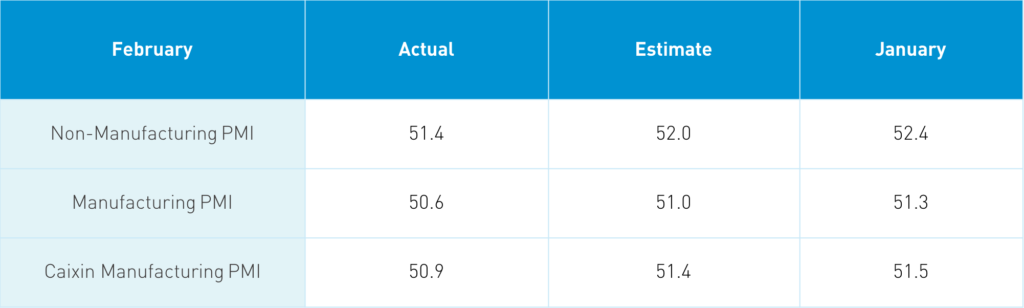

Takeaway: The “official” PMI’s, so-called as they are calculated and released by the National Bureau of Statistics, were released over the weekend. The Caixin Manufacturing PMI, which is calculated by IHS Markit, was released just after the market open. While the release came in light versus expectations, the market brushed it off as the Chinese New Year curtailed the number of workdays in the February calculation. The “official” PMI is a broad survey of large companies while the Caixin/IHS figure has a smaller number of survey participants that include private, medium, and small-sized companies. PMIs are diffusion indexes measuring month over month activity with a base level of 50. Above 50 means accelerating growth while under 50 means a contraction. There is a key nugget in the “official” as inventories of raw materials declined. Commodity price charts tell us that China needs more raw materials. This demand is reflected in higher input prices and thus higher output prices. Production and new orders increased in February. Meanwhile, employment and supplier delivery time were off their best levels. Within the “official” non-manufacturing index, construction dipped from 60 to 54.7. However, overall business confidence was very high. The release was not a market mover today.

Hang Seng announced the details of its revamping of the Hang Seng Index after the market close overnight. The revamp aims to make the index more representative of the economy. Historically the index was heavily weighted to Old Economy sectors such as financials, energy, materials, industrials, and real estate, all of which have been out of favor for the last decade.

Summary of changes:

- Holdings will increase to 80 by mid-2022 from the March rebalance of 55 holdings with a target of 100 stocks.

- Industry groups must have at least 50% of their market cap included in the index

- IPOs can be added within 3 months

- Weights are capped at 8% and current dual share class and weighted voting rights caps will be removed.

Takeaway: The weights of New Economy stocks will increase at the expense of Old Economy stocks, driven by the industry exposure requirement and the removal of the cap on dual share classes and weighted voting rights companies. Winners will include Alibaba HK, JD HK, NetEase HK, etc. as their weights in the index will go up. Financials will see their weights decline from 40% today to 32% at the 80 stock level and 26% at the 100 stock level. Tech will go from 26.9% to 28.6% and eventually reach 28.7%. The capping might reduce some volatility as the index. Just as fun will be the reaction from other index providers. Any look at MSCI China’s holdings recently? Tencent and Alibaba make up 29% of the index! I am a big advocate of the MSCI China All Shares as a better investable definition of China.

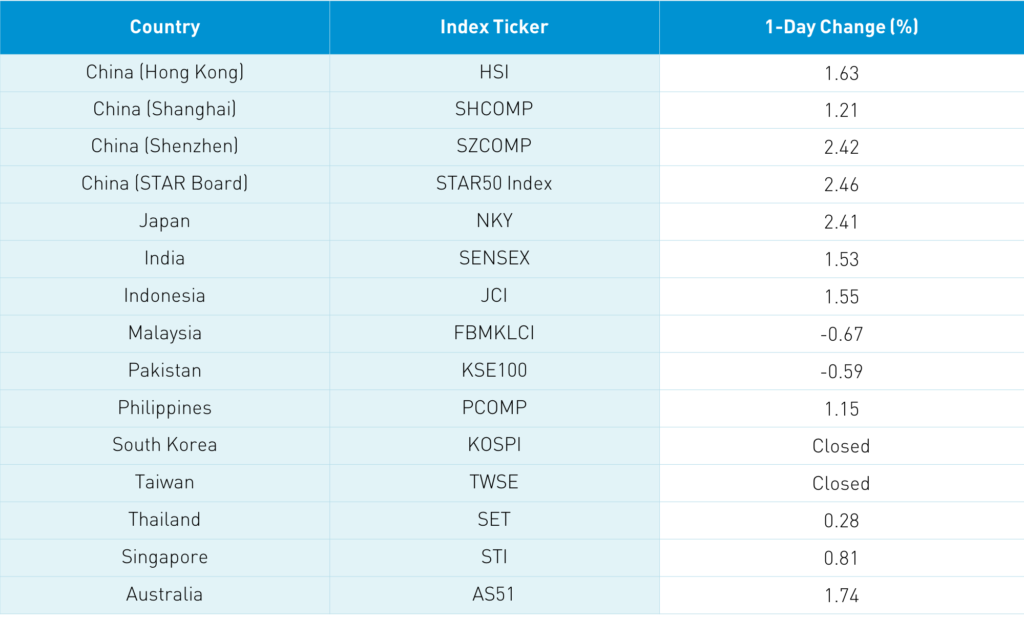

Asian equities rebounded strongly after last week’s taper tantrum debacle with South Korea and Taiwan missing out on the fun due to market holidays. Australia’s central bank bought long-dated bonds in early Asian trading, which gave stocks a tailwind that central banks might collectively rein in rising bond yields. Names kicked to the curb last week rebounded strongly as the Hang Seng gained 1.63% though the Chinese companies listed in Hong Kong and within the MSCI China All Shares Index gained 3.37%. Hong Kong volume leaders included Tencent, which gained +5.21%, Meituan, which gained +7.88%, Alibaba HK, which gained +0.95%, HK Exchanges, which gained +3.47%, GCL-Poly Energy, which ripped +7.37%, energy giant CNOOC, which fell -1.08% as the NYSE will delist its US listings, BYD, which gained +8.01%, Xiaomi, which gained +1.98%, and Wuxi Biologics, which gained +6.51%. Shanghai, Shenzhen, and STAR Board gained +1.21%, +2.42%, and +2.46%, respectively, as there were 3,417 advancing stocks and just 442 decliners. 7 to 1 advancers to decliners is amazing! Rare earth stocks had a strong day after the Ministry of Industry said it will increase its mining quota by 27%. Financials were off a touch as a rare down sector. Foreign investors bought $585 million worth of Mainland stocks today. Meanwhile, CNY appreciated versus the US dollar slightly while bonds rallied and copper eased.

I have commented in the past that NYC’s Penn Station has a hidden gem: a Tim Horton’s donut shop tucked in the bowels of the building. I usually go there to treat myself to a very good donut. Tencent participated in Tim Horton’s latest funding round, which was aimed at bolstering its China efforts. The company boasts 150 stores, which will be raised to 200 by year-end with an end goal of 1,500 stores. It is not hard to imagine Tim’s spinning off its China operations at some point, following in the footsteps of Yum brands.

The most important policy meetings of the year will take place in China this week as the CPPCC begins Thursday with the NPC on Friday. The “Two Sessions” will review the 14th Five Year Plan through the draft gives us a great insight into where economic policy is headed. Domestic consumption will be a big focus along with curbing pollution and technological self-sufficiency. The beneficiaries are easy to figure out: e-commerce, 5G, semiconductors, electric vehicles, and cleantech plays such as solar and wind.

H-Share Update

The Hang Seng opened higher and then bounced around the room to close +1.63% at 29,452. Volume was off -34% though was still 140% of the 1-year average. Meanwhile, breadth was mediocre with 25 advancers and 27 decliners. The 200 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index gained +3.37% led by discretionary +6.47%, communication +5.07%, health care +4.75%, tech +3.4%, staples +2.83%, industrials +2.28%, materials +1.63% while real estate and financials were off -0.12% and -0.13%, respectively. Southbound Connect volumes were moderate as mainland investors bought $10 million worth of Hong Kong stocks and Southbound Connect trading accounted for 15.1% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen gained +1.21% and +2.42% to close at 3,551 and 2,349, respectively. Volume was off -3.9% from Friday, which placed it right at the 1-year average while breadth saw 3,417 advancers and 442 decliners. The 519 Mainland Chinese companies within the MSCI China All Shares Index gained +1.56% led by communication +3.31%, industrials +3.03%, materials +2.79%, tech +2.65%, discretionary +2.63%, health care +1.33% and staples +1.24% while utilities and financials were off -0.37% and -0.43%. Northbound Stock Connect flows were elevated as foreign investors bought $585 million worth of Mainland stocks today as Northbound Stock Connect trading accounted for 6.8% of Mainland turnover.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.47 versus 6.48 Friday

- CNY/EUR 7.79 versus 7.85 Friday

- Yield on 1-Day Government Bond 1.70% versus 1.71% Friday

- Yield on 10-Year Government Bond 3.25% versus 3.28% Friday

- Yield on 10-Year China Development Bank Bond 3.71% versus 3.75% Friday

- China's copper price -2.31% overnight