China Bank Regulator Warns of Foreign Equity Bubbles

4 Min. Read Time

Key News

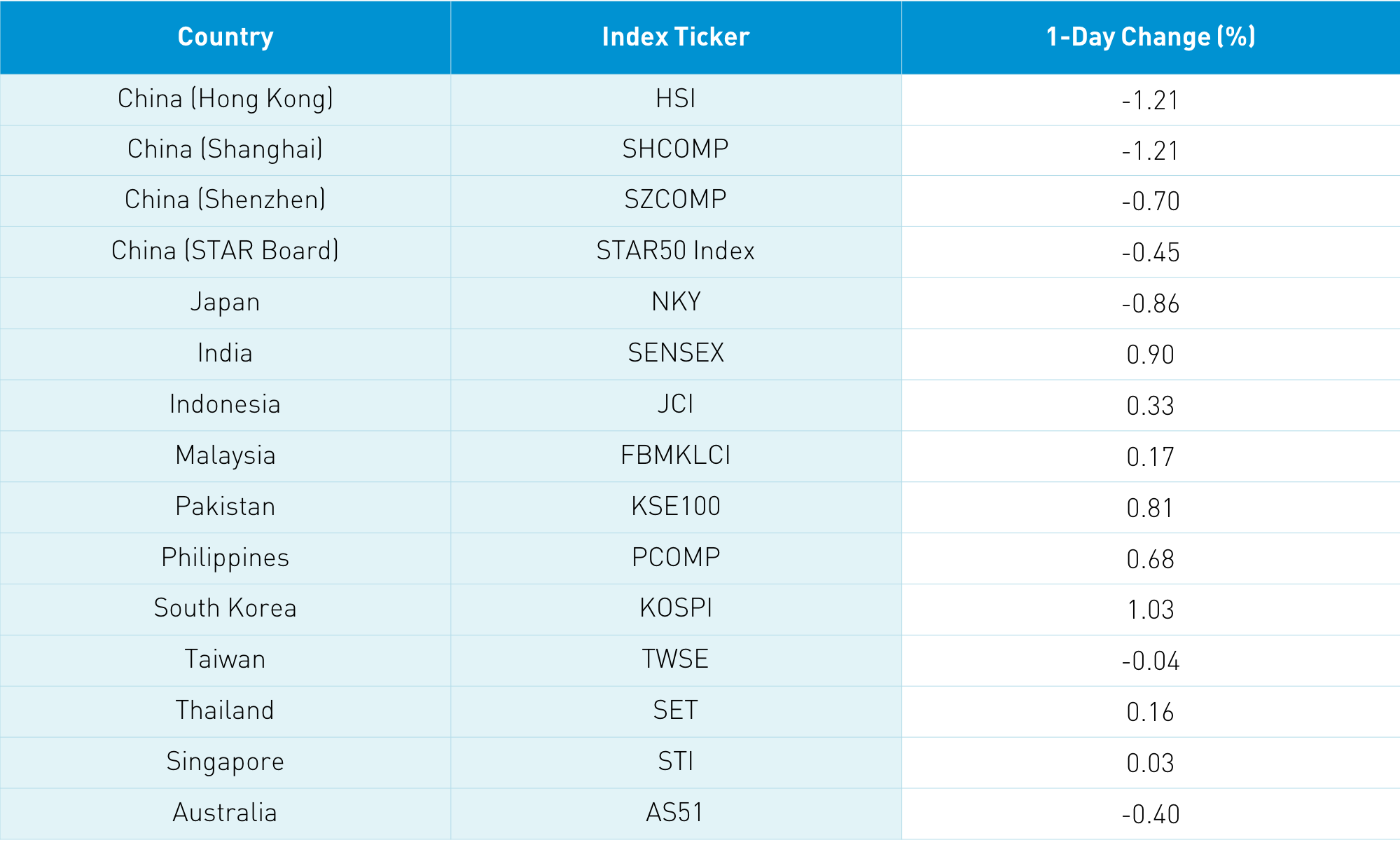

Asian equities were mixed as India and South Korea outperformed. The biggest catalyst was China Banking and Insurance Regulatory Commission Chairman Guo Shuqing's speech yesterday, in which he warned of bubbles in the US and European stock markets while voicing concern about property speculation in China. Reading the tea leaves, it is clear that China will take its foot off the monetary and fiscal stimulus gas pedal later this year. While no one believes China will raise interest rates, it may tighten liquidity to some extent.

Guo's comments took the wind out of Mainland Chinese equities as markets are forward-looking. It is critical to point out that this is not going to happen imminently but likely in the second half of 2021. The PBOC head said recently that there will be no “sharp turns”. It will be done incrementally versus pulling the proverbial Band-Aid.

Guo had positive comments on the internet banking space but said that companies need to adhere to the same rules traditional banks do. The net takeaway is that China’s policymakers are focused on reducing leverage, which is a good thing for long-term investors.

After last week’s taper tantrum sell-off, Hong Kong was off as authorities said the Hong Kong stamp tax will not be expanded. However, other taxes are feasible. The stamp tax increase news caught Mainland investors investing in Hong Kong flat-footed as they sold Hong Kong stocks today in a rare event. Both Tencent and Meituan seeing selling. Crypto names were off as Mongolia banned Bitcoin mining.

Cleantech names were up on new policies outlining China’s path to carbon neutrality will be released imminently. With less coal and more solar, wind and EV seems logical. The Hang Seng opened higher but quickly put the landing gear down, falling -1.21% to close at 29,095 with only 9 advancers and 43 decliners in a 180 from yesterday.

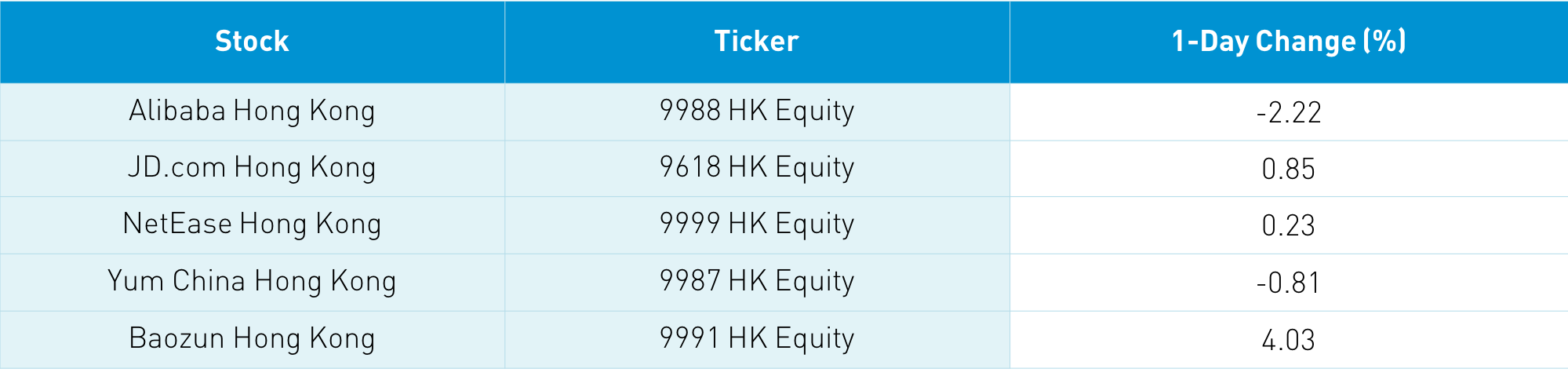

Hong Kong volume leaders by value traded were Tencent, which rose +0.14%, Meituan, which fell -1.2%, Alibaba Hong Kong, which fell -2.22%, GOME Retail, which was off -18.97% after selling shares, Hong Kong Exchanges, which dropped -0.41%, Semiconductor Manufacturing, which rose +3.74% on chatter that the US tech export ban might be lifted, Xiaomi, which gained +0.97%, energy giant CNOOC, which fell -3.39% after Monday’s announcement that its US share class will be delisted, BYD, which rose +0.75%, and China Mobile, which fell -2.4%. Shanghai, Shenzhen, and STAR Board were off -1.21%, -0.7%, and -0.45% respectively as Guo’s comments weighed on financials and real estate stocks.

Mega caps underperformed relative to mid and small caps due to the large weight of banks. One local broker noted some mutual fund redemptions from investors, though I’ve not seen any data on the topic. Kweichow Moutai was off -4.63% despite its parent company reporting strong results yesterday as foreign investors turned tail, selling -$1.049 billion worth of Mainland stocks. Bonds were off a touch as the specter of tighter monetary conditions could see yields rise while CNY was off a touch versus the US dollar along with copper.

I’ve mentioned that LI US, DQ US, and VNET US were added to MSCI indexes, requiring passive managers to buy the shares at the market’s close last Friday. VNET has a 1-year value of trading of $54mm. Last Friday, it traded $414mm versus Thursday’s $47mm. LI has a 1-year value traded of $579mm while last Friday it traded $1B. DQ has a 1-year value trading of $137mm while last Friday it traded $744mm.

Autohome (ATHM US) updated its filing for its Hong Kong dual share class listing while Baidu’s relisting is rumored to be next week.

Trip.com (TCOM US, formerly C-trip.com) will report after the US close tomorrow.

Asia e-commerce giant Sea (SE US) reported strong revenue growth beating analyst expectations, though its EPS loss widened. Brokers seemed more focused on the company’s conference call’s positive outlook.

The South China Morning Post reported that Ant Group Chairman Eric Jing will proceed with an IPO at some point though no time frame was given. While the Vince Lombardi speech was likely to improve morale, an IPO under the new rules would be feasible.

H-Share Update

The Hang Seng opened higher before falling -1.21%, closing at 29.095. Volume increased +115 from yesterday, which is 156% of the 1-year average while breadth had just 9 advancers and 43 decliners. The 200 Chinese companies listed in Hong Kong within the MSCI China All Shares Index were off -0.78%, with communication and real estate up +0.1% and 0.09% respectively, while staples fell -2.48%, energy -1.9%, health care -1.74%, discretionary -1.3%, materials -1.08%, tech -1%, financials -0.98%, and industrials -0.44%. Southbound Stock Connect volumes were elevated as Mainland investors sold -$234mm of Mainland stocks as Southbound trading accounted for 13.5% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen opened higher though slip-sliding -1.21% and -0.7% respectively to close at 3,508 and 2,332. Volume was up 5% from yesterday, which is just above the 1-year average while breadth had 1,181 advancers and 2,677 decliners. The 519 Mainland stocks within the MSCI China All Shares Index were off -1.37% with utilities up +1.18%, while staples fell -2.98%, materials -2.37%, health care -2.27%, communication -2.1%, financials -1.13%, real estate -0.78%, discretionary -0.56%, energy -0.51% industrials -0.35%, and tech -0.06%. Northbound Stock Connect volumes were elevated as foreign investors sold $1.049B of Mainland stocks as Northbound trading accounted for 7.5% of Mainland turnover.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.47 versus 6.47 Yesterday

- CNY/EUR 7.79 versus 7.79 Yesterday

- Yield on 1-Day Government Bond 1.60% versus 1.70% Yesterday

- Yield on 10-Year Government Bond 3.25% versus 3.25% Yesterday

- Yield on 10-Year China Development Bank Bond 3.71% versus 3.71% Yesterday

- China's copper price -1.27% overnight