Market Correction Continues as Trip.com Results Deliver

4 Min. Read Time

Key News

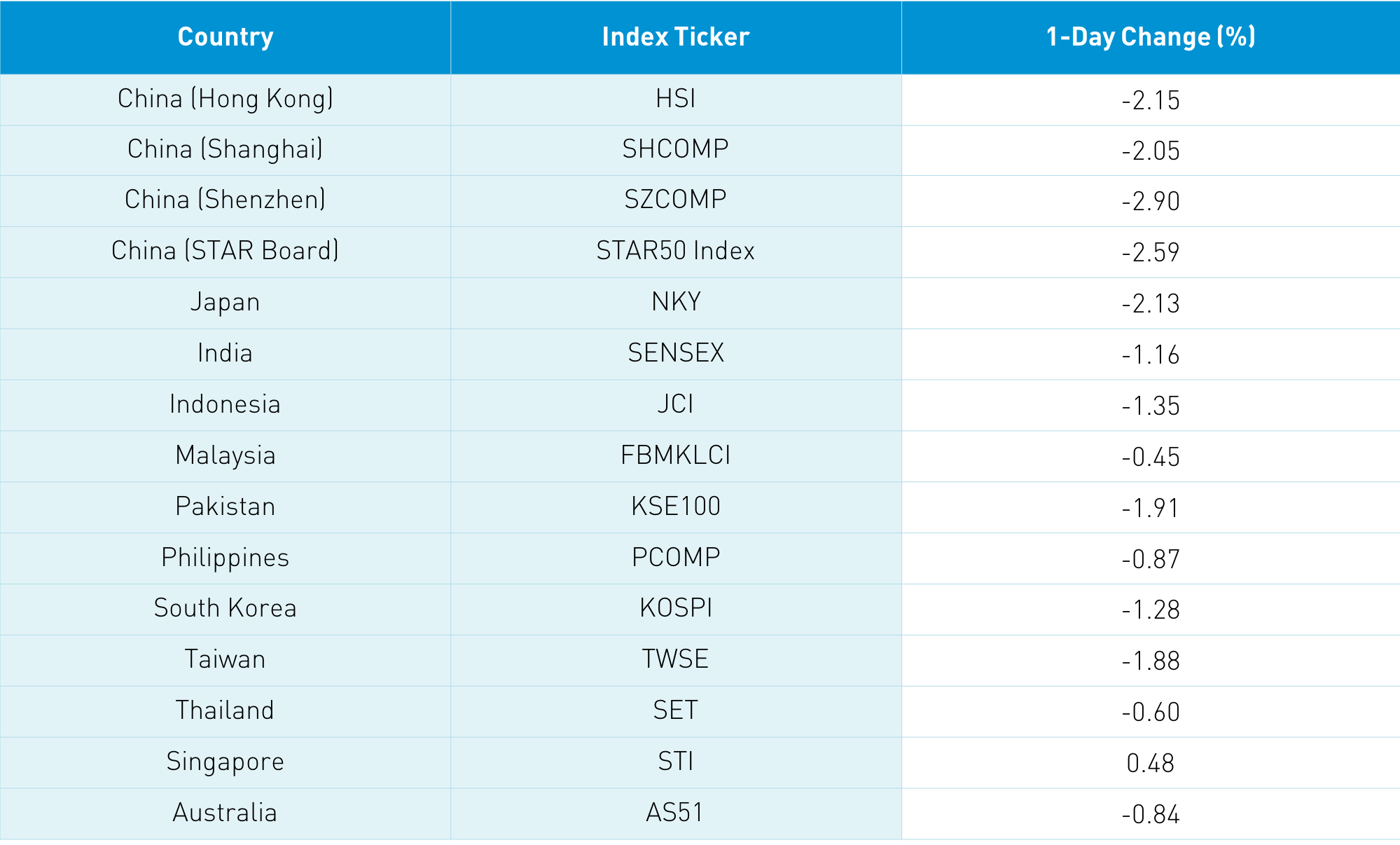

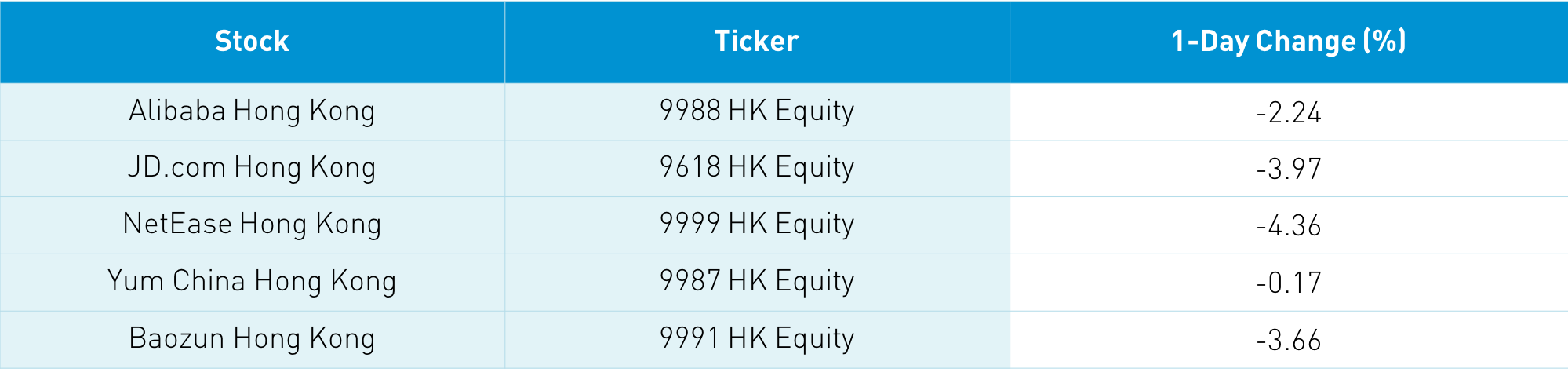

Asian equities were a sea of red following the US’ downward performance on rising US Treasury yields. Fed Chair Powell speaks today at noon, so we’ll see if he can soothe investors’ fears. Previous winners from a stock and sector perspective were hit the hardest. The Hang Seng Index was off -2.15% while the broader Hang Seng Composite was off -3.26%. The Chinese companies listed in Hong Kong within the MSCI China All Shares Index were off -4.4%. Hong Kong volume leaders by value were Tencent, which fell -4.56%, Meituan, which was off -8.75%, Semiconductor Manufacturing, which dropped -1.98%, China Mobile, which fell -2.22%, Hong Kong Exchanges, which was off -3.01%, Alibaba Hong Kong, which fell -2.24%, Xiaomi, which fell -3.97%, Ping An Insurance, which was off -0.71%, Kuaishou Technology, which fell -5.55%, and BYD, which dropped -8.12%. The only bright spots were energy stocks, which outperformed on low US oil inventories and reduced coal mining raising prices.

Southbound Stock Connect, Mainland investors' access to Hong Kong stocks, was a rare outflow day of $558mm. Shanghai, Shenzhen, and STAR Board were off -2.05%, -2.90%, and -2.59% respectively in a similar pattern as we saw in Hong Kong and regionally as previous winners were kicked to the curb. Steel names were a rare outperformer as output curbs should raise prices. Northbound Connect, the venue for foreign investors to buy Mainland stocks, saw -$1.139B of outflow following yesterday’s +$1.393B inflow. Bonds were off a touch, CNY eased a touch versus the US dollar, and copper fell by -1%. Shanghai and Shenzhen are back at the bottom of their breakout ranges. We’ll see if the previous resistance level becomes the support level. Real estate was off as tighter property sale rules were announced in several cities.

This month is a very important month for earnings for Chinese companies listed in the US, Hong Kong, and Mainland China. The stocks that were embraced by investors are being kicked to the curb. What happens when these companies start reporting Q4 results? Alibaba reported very strong Q4 results as revenue grew 36.9%. What happens if Tencent, Meituan, and others put up similar results?

We also have the Two Sessions, China’s most significant policy meeting occurring for the next week, where we will receive guidance on economic goals. What happens when we hear about electric vehicle targets, solar/wind energy transmission production goals, raising domestic consumption, 5G, and semiconductor support? Investors can be fickle, which is why we have always wanted to focus on long-term trends as market timing is difficult. Will there be more or less Chinese urban middle-class consumers in the next decade?

Baidu’s Hong Kong listing has been approved and its roadshow will kick off next week.

The automotive industry's semiconductor chip shortage has gone beyond Ford to include GM, which is now idling three plants. Toyota and Nio have also had to curtail production. It will be interesting to see if auto plant idling cools ascent in the prices of industrial metals.

Online travel company Trip.com Group (TCOM US, formerly known as C-trip) reported Q4 financial results after the US market close yesterday. Year-over-Year (YoY) comparisons aren’t pretty though the results were better than anticipated. Management should be given credit as they showed prudence in cutting costs. The company managed to stay profitable in the quarter. TCOM’s China business has rebounded. However, their UK and foreign business are still being affected. TCOM is likely to see investor attention as a “reopening” play.

- Revenue -40% to RMB 5B ($761mm) versus analyst expectations of RMB 4.943B

- Sales & marketing expense -50% to RMB 1.2B ($189mm)

- General & administrative expense declined -20% to RMB 676mm ($104mm)

- Gross margin improved to 82% versus 79% in Q4 2019

- Adjusted Net Income RMB 1.063 versus analyst expectations of RMB 187mm

- Adjusted EPS RMB 1.75 ($0.27) versus analyst expectations of RMB 0.28

Baozun (BZUN US and 9991 HK) is an “e-commerce service partner that helps brands execute their e-commerce strategies in China”. The company helps foreign brands market and sell across China’s e-commerce platforms while helping with social media. While revenue missed analyst expectations by a small amount, net income and especially earnings per share (EPS) beat them. I do not hold many individual stocks though I do hold 100 shares of Baozun, which I bought during the downdraft in late December 2019.

- Revenue increased +20% to RMB 3.346B ($512mm) versus analyst expectations of RMB 3.383B

- Gross merchandise value sold +28.7% to RMB 22.872B

- Brand partners increased to 266 from 231 from 12/31/19

- GMV brand partners increased to 258 from 222 from 12/31/2019

- Adjusted Net Income +68.4% YoY to RMB 271mm ($41mm) versus analyst expectations of RMB 258mm

- Adjusted EPS RMB 3.58 ($0.55) versus analyst expectations of RMB 3.35

H-Share Update

The Hang Seng traded lower in the morning falling -2.15%, closing at 29,236. Volume increased +21%, which is 149% of the 1-year average while breadth had 16 advancers and 35 decliners. The 200 Chinese companies listed in Hong Kong were off -4.4%, with energy up +0.02%, while discretionary fell -7.34%, healthcare -6.76%, tech -6.46%, materials -5.41%, communication -4.56%, industrials -4.14%, utilities -3.97%, staples -3.64%, real estate -2.09%, and financials -0.96%. Southbound Stock Connect volumes were light compared to recent history as Mainland investors sold $558mm of Hong Kong stocks today as Southbound trading accounted for 14.7% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen opened lower and traded lower down -2.05% and -2.9% closing at 3,503 and 2,294 respectively. Turnover increased by +12.9% from yesterday, which is 111% of the 1-year average while breadth had 1,155 advancers and 2,663 decliners. The 519 Mainland stocks within the MSCI China All Shares Index were off -3.39%, with utilities up +0.94%, while staples fell -4.88%, healthcare -4.26%, materials -4.2%, industrials -4.15%, tech -4%, discretionary -3.48%, communication -2.45%, real estate -2.09%, financials -1.19%, and energy -0.42%. Northbound Stock Connect volumes were moderate/high as foreign investors sold -$1.139B of Mainland stocks as Northbound Stock Connect accounted for 7.9% of Mainland turnover.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.47 versus 6.47 yesterday

- CNY/EUR 7.79 versus 7.80 yesterday

- Yield on 1-Day Government Bond 1.43% versus 1.40% yesterday

- Yield on 10-Year Government Bond 3.27% versus 3.26% yesterday

- Yield on 10-Year China Development Bank Bond 3.72% versus 3.71% yesterday

- China’s Copper Price -1.00% overnight