Punters Punt While Smart Money Buys

3 Min. Read Time

Upcoming Event

Join us on Thursday, March 25th from 9:00 am to 1:00 pm EDT for our event:

KraneShares’ Future of Green ETFs Summit.

Click here to register.

Key News

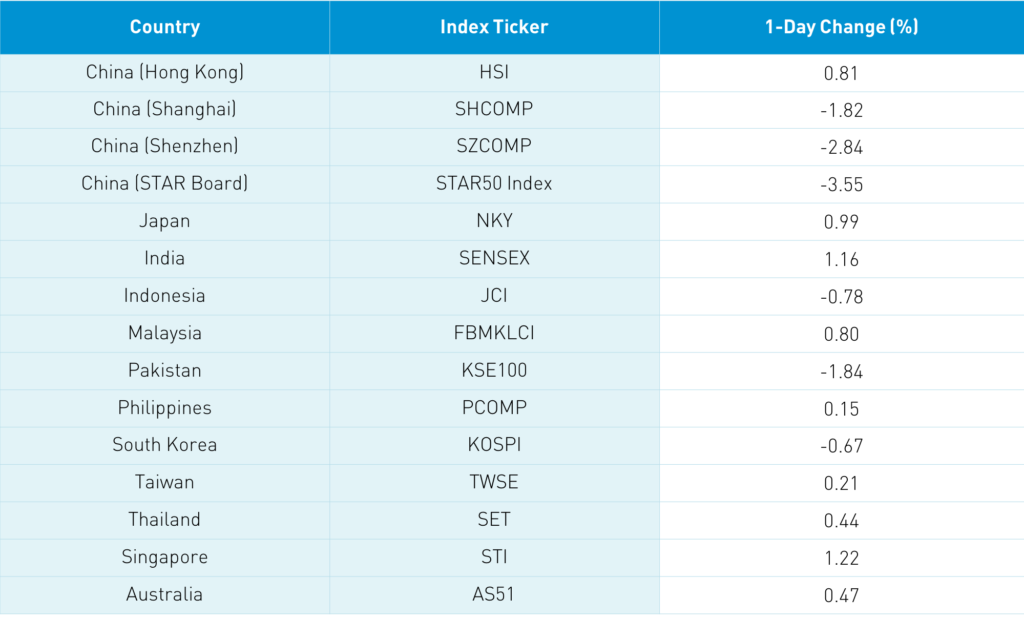

Asian equities opened lower though rallied mid-morning on reports that Chinese pension plans and insurance companies, affectionately known as the National Team, were buying Mainland stocks. The news lifted the region though ironically the Mainland rallied off lows but faded in afternoon trading. I suspect Mainland China’s retail investors are coming out of stocks and the exit door is only so big. The historic track record of the National Team, long-term investors who have bought previous market plunges, is quite strong. Buy low sell high – amazing concept. An element of stability did occur in Hong Kong as one local broker noted institutional investors putting cash to work in quality growth stocks while cyclical stocks, which have been underweighted, garner some TLC.

We also had positive auto sales numbers released. Great Wall Motor's February vehicles sales grew +788% to 89,050 and Guangzhou Auto reported that February sales grew +443% to 105,128. February EV sales increased 700% year over year though fell -38% month-over-month to 97,000. Tesla sold 18,318 EVs, which is up 18% from January. There is chatter that US-listed Chinese automakers Nio, Li, and Xpeng will relist in Hong Kong. I am surprised Tesla hasn’t done the same. We are also starting to see sell-side analysts opine on the dramatic move as an opportunity to buy good companies at cheaper prices than a month ago.

The Hang Seng Index bounced around the room, closing up +0.81% at 28,773 on high volumes nearly twice the 1-year average. Hong Kong volume leaders by value traded were Tencent, which rose +0.23%, Meituan, which fell -2.2%, Xiaomi, which fell -1.79%, Alibaba Hong Kong, which rose +1.54%, Hong Kong Exchanges, which fell -3.21%, China Mobile, which was off -2.49%, China Construction Bank, which fell -0.91%, Ping An Insurance, which rose +0.61%, GCL-Poly Energy, which gained +1.87%, BYD, which rose +0.8%, and JD.com, which fell -2.74%. Mainland investors sold another $1.141B of Hong Kong stocks today.

Mainland China couldn’t hold the mid-morning rally as selling continued in the afternoon. Shanghai, Shenzhen, and STAR Board were off -1.82, -2.84%, and -3.55% respectively.

Mainland volume leaders by value traded were Kweichow Moutai, which fell -1.17%, Longi Green Energy, which was off -6.15%, liquor name Wuliangye Yibin, which fell -0.82%, BYD, which fell -3.42%, broker East Money, which was off -4.44%, Ping An Insurance, which fell -1.06%, CATL, which was off -1.64%, Sany Heavy Industry, which dropped -7.1%, BOE Tech, which fell -5.1%, and China tourism, which gained +1.18%. Volumes were just over the 1-year average while breadth was awful with nearly 5 to 1 losers to winners. Northbound Stock Connect volumes were high with a net buying of $373 million worth of Mainland stocks. There was chatter that the National Team might have used Connect to buy Mainland stocks. Bonds were off a touch, CNY rallied versus the USD, and copper was up a touch.

Yesterday’s move in US-listed Chinese stocks left me and our institutional brokers scratching our heads. There was no significant catalyst for yesterday’s market action. Yes, there was some individual stock news, but nothing to warrant the move. This morning an institutional broker noted that retail trading now accounts for 23% of US trading volume, which is up 2X from 2019. Work from home has become trade from home, though I believe this is a global phenomenon.

H-Share Update

The Hang Seng had a choppy session, gaining +0.81% to close at 28,773. Volume was flat overnight, which is still 181% of the 1-year average while breadth had 36 advancers and 16 decliners. The 200 Chinese companies listed in Hong Kong within the MSCI China All Shares Index were off -0.03%, with materials up +1.04%, staples +0.88%, industrials +0.64%, healthcare +0.56%, communication +0.34%, and utilities +0.04%, while discretionary fell -0.185, real estate -0.34%, tech -0.55%, financials -0.59%, and energy -2.14%. Southbound Stock Connect volumes were moderate as Mainland investors sold $1.141B of Hong Kong stocks today as Southbound trading accounted for 14% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen had a choppy session closing -1.82% and -2.84% at 3,359 and 2,160 respectively. Volume was flat for the day, which is still 114% of the 1-year average while breadth had just 630 advancers and 3,271 decliners. The 519 Mainland stocks within the MSCI China All Shares Index fell -2.07%, with utilities down -0.73%, real estate -0.93%, communication -0.95%, discretionary -0.96%, energy -1.07%, financials -1.82%, industrials -1.93%, materials -1.94%, staples -2.1%, healthcare -2.935, and tech -3.32%. Northbound Stock Connect volumes were high as foreign investors bought $373mm of Mainland stocks as Northbound Connect trading accounted for 7.9% of Mainland turnover.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.51 versus 6.53 yesterday

- CNY/EUR 7.75 versus 7.75 yesterday

- Yield on 1-Day Government Bond 1.55% versus 1.50% yesterday

- Yield on 10-Year Government Bond 3.25% versus 3.24% yesterday

- Yield on 10-Year China Development Bank Bond 3.69% versus 3.68% yesterday

- China's Copper price +0.27% overnight