Economic Data Released After China’s Close While US-China Dialogue Ramps Up

4 Min. Read Time

Upcoming Event

Join us on Thursday, March 25th at 9:00 am EDT for our event:

KraneShares’ Future of Green ETFs Summit.

Click here to register.

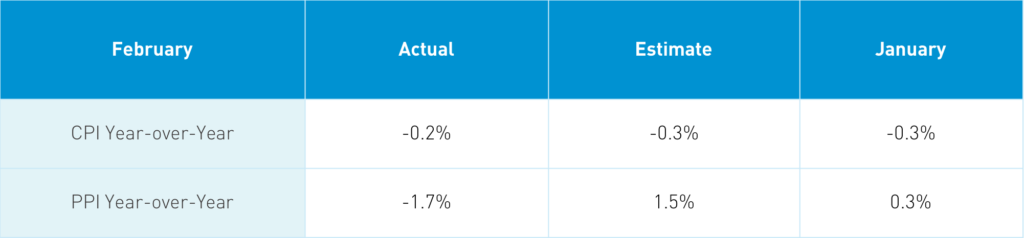

Takeaway: Remember that Chinese New Year took place in February this year but occurred in January last year, which makes for some funky year-over-year comparisons. The US’ CPI gets a lot of criticism due to its composition and for not being a good measure of actual inflation as it lacks food and energy price changes. China’s CPI is heavily influenced by pork prices, which have been falling after the swine flu led to the wiping out of Chinese pigs. Pig herds are coming back, creating more supply as pork prices fell -14% in February. Remove pork prices and CPI would have registered a small uptick. Sub-category medical care saw prices rise +0.3% though off their more than 1% streak for the last 10 months. PPI was higher as the global economy comes on line requiring more commodities, which are driving up prices.

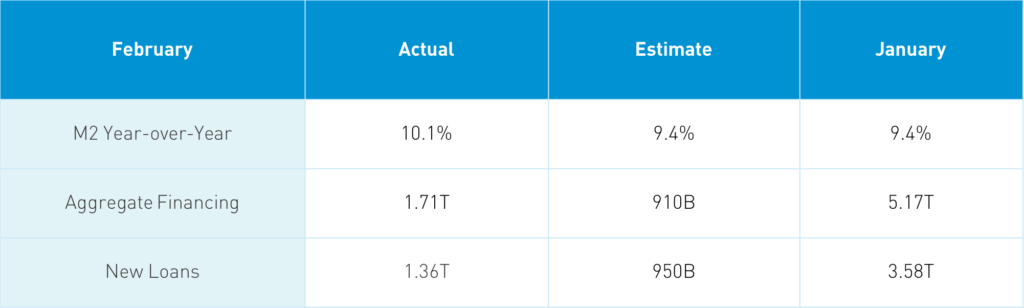

Takeaway: This data was released after the market close. Remember the market has been concerned about tighter monetary conditions though the data shows otherwise. China’s economy continues to rebound along with the global economy for that matter, requiring more capital as the data indicates. This release is a bit of a sleeper due to the post-market release – nonetheless, a very encouraging release!

Key News

The Wall Street Journal reported yesterday that the US and China will co-chair a G-20 climate summit. We’ve previously stated that John Kerry is apt to have an outsized role within the Biden Administration due to his long friendship with the President, which was forged by their decades in politics. A small win on climate change, which China is taking very seriously, could lead to other wins.

Overnight, Mainland brokers noted that a carbon credit allowance trading system could be launched in Shanghai as soon as June. Carbon credits give industrial users the right to pollute but discourage polluting by setting a price.

We also had news that the US and China’s senior diplomats might be meeting in Alaska, which could pave the way for a Biden-Xi summit. Media reports are saying Secretary of State Antony Blinken would meet with foreign minister Wang Yi. As we've been saying, communication and dialogue is the first step in finding ways to avoid further escalation.

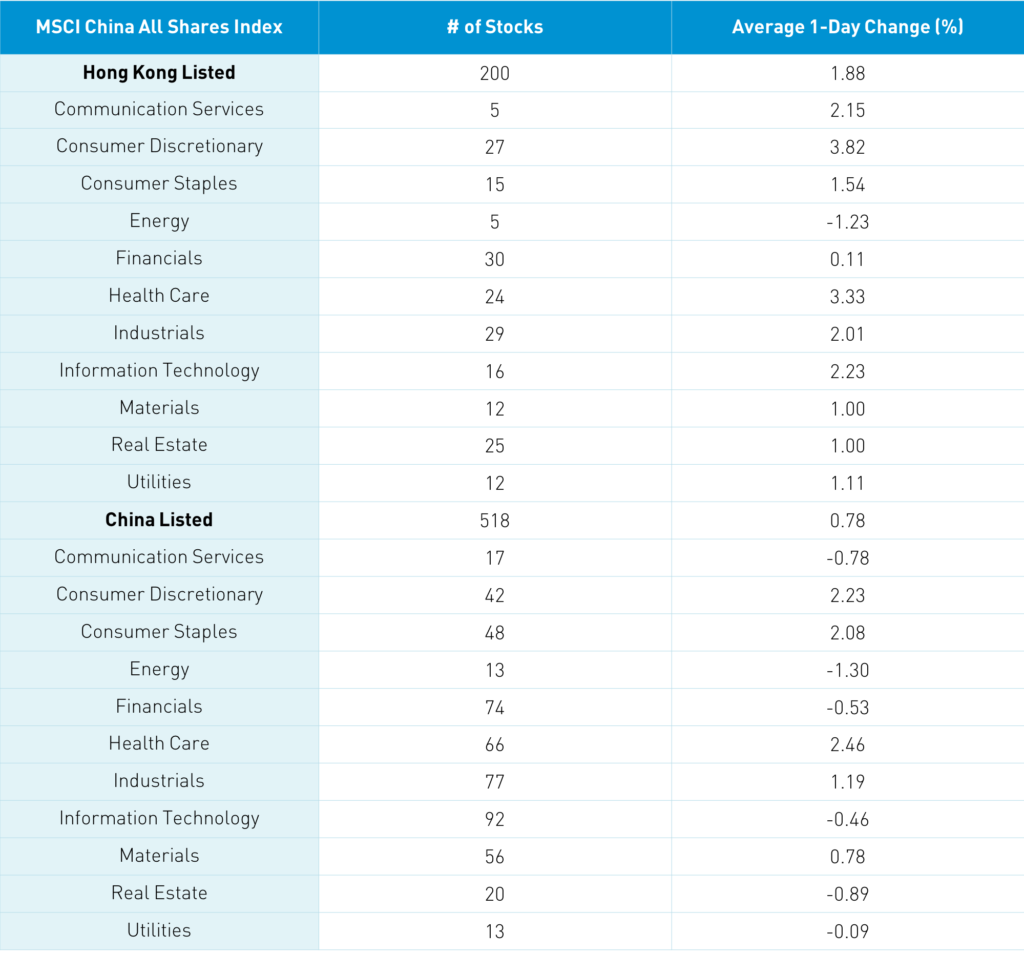

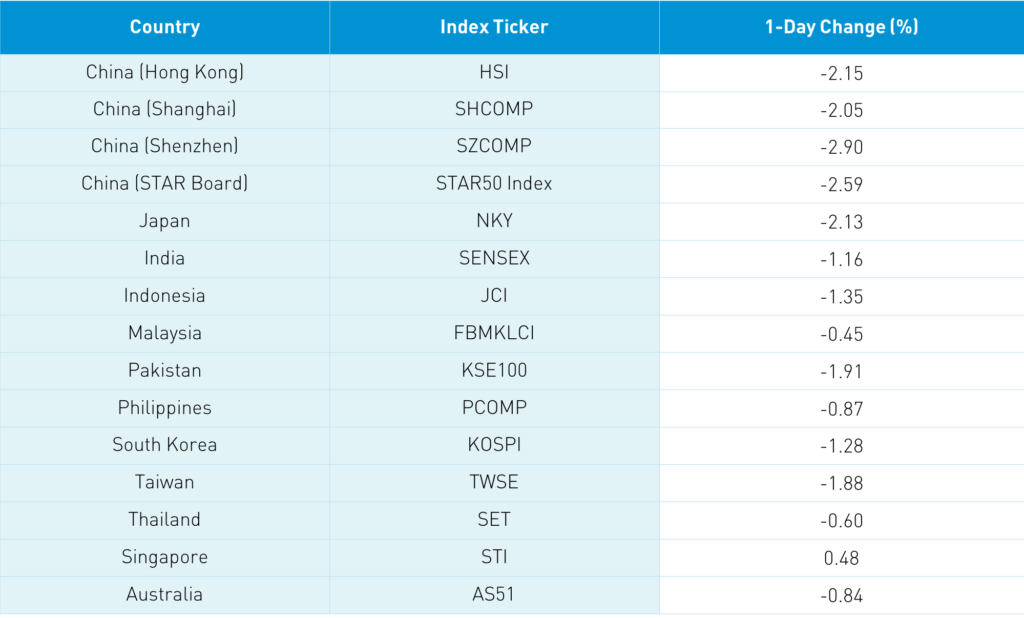

Asian equities had a largely positive day though South Korea and Singapore were outliers to the downside. On a rebound day, we would want to see strong volumes. However, Hong Kong turnover was off -30.98% from yesterday, despite being 125% of the 1-year average. The Hang Seng Index gained +0.47% and the Chinese companies listed in Hong Kong and within the MSCI China All Shares Index gained +1.88%. Two Hong Kong brokers noted institutional investors bought the dip in quality growth names. Hong Kong volume leaders by value were Tencent, which rose +2.25%, Meituan, which gained +4.97%, Alibaba Hong Kong, which rose +1.96%, Xiaomi, which fell -0.68%, China Mobile, which was off -2.1%, Hong Kong Exchanges, which gained +0.91%, BYD, which rose +5.21%, Ping An Insurance, which rose +0.1%, Wuxi Biologics, which was up +5.71%, and AIA, which fell -0.3%.

There was a touch of growth stocks and sectors gaining with discretionary, health care, tech, staples, and industrials outperforming. Southbound Connect volumes were moderate/light as Mainland investors sold $558 million worth of Hong Kong stocks today via Southbound Connect with Tencent and Meituan were net outflows. Southbound Connect trading accounted for 13.8% of Hong Kong turnover.

Shanghai, Shenzhen, and STAR Board returned -0.05%, +0.21%, and +0.21%, respectively, as names from favored growth sectors that were kicked to the curb yesterday rebounded as mega and large caps outperformed.

The 518 Mainland stocks within the MSCI China All Shares Index gained +0.78%, led by healthcare, discretionary, staples, and industrials while energy was the worst sector. Mainland volume leaders by value traded were Kweichow Moutai +1.7%, Longi Green Energy +1.19%, liquor stock Wuliangye Yibin +416%, BYD +3.81%, battery giant CATL +4.83%, broker East Money +1.02%, Ping An -0.92%, BOE Tech flat, GEM Co -2.22% and China Tourism Group +6.14%. Volume was off -24% from yesterday and -13% from the 1-year average. Foreign investors bought $802mm of mainland stocks today via Northbound Stock as Northbound Connect trading accounted for 6% of Mainland turnover.

MSCI announced the dates for the dissemination of its May Semi-Annual Index Review’s pro forma on May 11th and the actual rebalance occurring May 27th. An institutional broker noted that Singapore ADRs will be eligible for inclusion at the May SAIR. While it is still a few months away, this could be a catalyst for Sea Ltd (ticker: SE), the Singapore-based gaming and e-commerce company.

This Friday is the rebalance for the Hang Seng Index with Alibaba Health, hotpot chain Haidilao, and real estate development company Longfor Group being added.

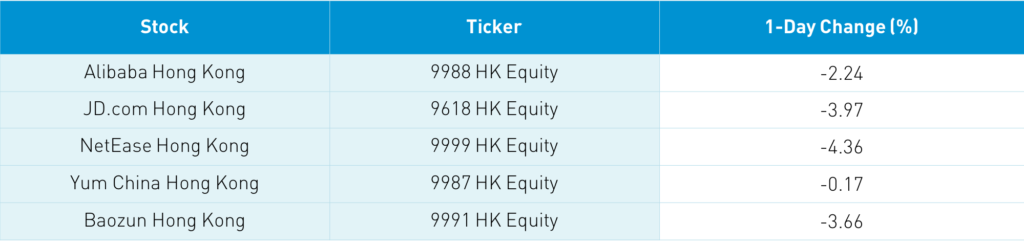

JD.com and Pinduoduo will report tomorrow.

I added MSCI China All Shares’ sector performance for Hong Kong and Mainland China. MSCI China has become a touch funky as out of the 604 holdings, Tencent and Alibaba make up 29% of the index while the remaining 602 holdings make up the remaining 71%. I’m a big fan of MSCI China All Shares as a total China solution as it includes the full weight of Chinese A-Shares versus MSCI China holding all of the stocks but only 20% of the potential weight of China A-Shares.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.51 versus 6.53 yesterday

- CNY/EUR 7.75 versus 7.75 yesterday

- Yield on 1-Day Government Bond 1.55% versus 1.50% yesterday

- Yield on 10-Year Government Bond 3.25% versus 3.24% yesterday

- Yield on 10-Year China Development Bank Bond 3.69% versus 3.68% yesterday

- China's Copper price +0.27% overnight