JD.com Powers Through Q4, China Stocks Rebound

5 Min. Read Time

JD.com Earnings

E-commerce giant JD.com (JD US, 9618 HK) released Q4 earnings this morning before the US market open. Let’s not bury the lead: they crushed it! JD had a few positives during the fourth quarter of 2020 including Singles Day and the IPO of JD Health on December 8, 2020. Yesterday, we released a piece of commentary on the correction. A key point was growth stocks can be divided between concept stocks (companies hoping to capitalize on a trend) versus quality growth (real companies with real revenues, net income, and free cash flow). JD.com’s free cash flow was RMB 4.575B ($701mm)! $701mm in Q4 while free cash flow in 2020 was $5.352B! JD Logistics will pursue an IPO in Hong Kong while JD Digits, their fintech arm, likely will refrain from doing so due to the new regulations. One downside to Hong Kong listings is that forward revenue guidance is not allowed.

- Revenue +31.4% to RMB 224.3B ($34.4B) versus analyst expectations of RMB 219B

- Core business line JD Retail RMB 208.594B ($31.9B) from RMB163B YoY

- Annual active customers +30.3% to 471.9mm from 362mm year over year

- Adjusted EBITDA increased to RMB 2.7B ($0.4B) from RMB 2B YoY

- Adjusted EPS RMB 1.49 ($0.23) versus estimate RMB 1.23

Key news

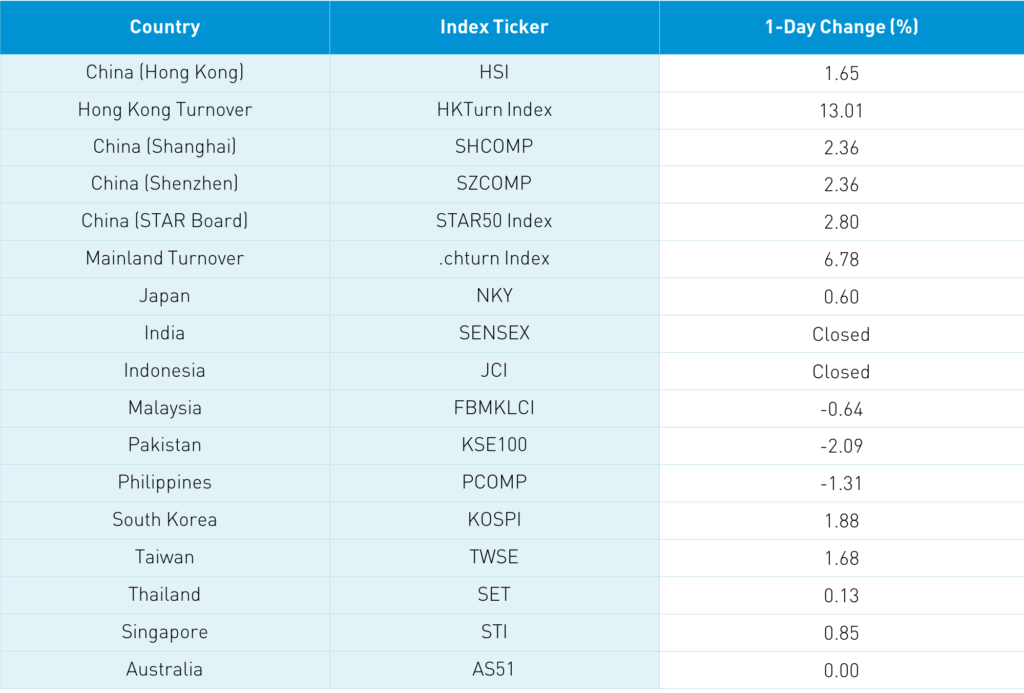

Asian equities were higher today as Mainland China and South Korea rebounded after recent weakness. Hong Kong and Mainland China saw several catalysts today including yesterday’s strong economic data release. Yesterday, I emphasized that the release occurred after the market close and so the market did not have an opportunity to react.

The China Semiconductor Industry Association announced that it has been communicating with its US equivalent the Semiconductor Industry Association to address chip shortages. On the diplomatic front, top US and Chinese diplomats will meet in Alaska in April and again at the G-20 climate change summit in October, which will be jointly chaired by both superpowers. On the domestic political front, Premier Li gave a speech at the conclusion of the National People’s Congress (NPC), though it did not make waves.

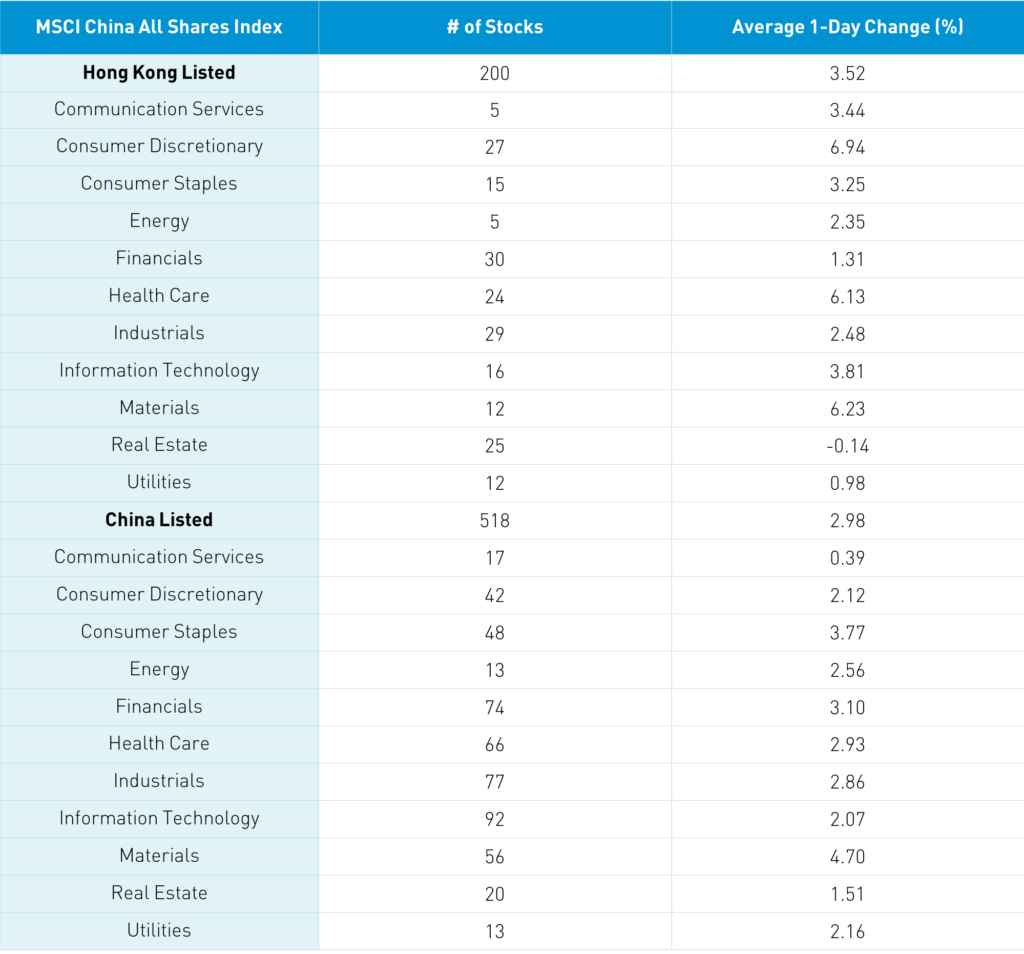

The Hang Seng Index gained +1.65% as the Chinese companies listed in Hong Kong and within the MSCI China All Shares Index gained +3.52% led by discretionary, healthcare, materials, all of which gained about +6%. Volume was up 13% from yesterday, placing it at 141% of the 1-year average. Hong Kong equity leaders by value traded were Xiaomi, which gained +0.23%, Tencent, which gained +3.34% accompanied by strong Connect inflow, Meituan, which gained +8.71% despite selling via Connect, Alibaba HK, which fell -0.35%, SMIC, which gained +10.1%, HK Exchanges, which gained +3.69%, Kuaishou Technology, which gained +10.64% in advance of its index inclusion tomorrow, China Mobile, which fell -0.64%, China Construction Bank, which gained +1.87%, and Wuxi Biologics, which gained +7.34%. Southbound Connect volumes were moderate to light as Mainland investors bought $583 million worth of Hong Kong stocks and Southbound Connect trading accounted for 12.4% of Hong Kong turnover.

Shanghai, Shenzhen, and the STAR Board gained +2.36%, +2.36%, and +2.8%. Meanwhile, the Mainland stocks within the MSCI China All Shares Index gained +2.98%. Volume increased by 6.7% from yesterday, though was only 93% of the 1-year average.

There was talk yesterday that an unnamed mutual fund portfolio manager was telling his friends on WeChat that he was buying yesterday. Overnight, there were discussions that mutual fund families want to raise money to put money to work at these levels. I failed to point out yesterday that mainland China ETFs saw inflows of $1.353 billion yesterday, which brings the weekly inflow to $4.073 billion. Today, we saw another $280 million of ETF net buying in China, which raises the 1-week total inflow to $4.56 billion. Cement names rallied on news they will be incorporated in China’s carbon curtailment programs. Mainland volume leaders by value traded were Kweichow Moutai, which gained +3.96%, liquor stock Wuliangye Yibin, which gained +4.92%, Ping An Insurance, which gained +3.7%, Longi Green Energy, which gained +4.69%, CATL, which gained +5.34%, BYD, which gained +3.26%, Zijin Mining, which gained +10.01%, broker East Money, which gained +2.84%, BOE Tech, which fell -1.18%, and Apple supplier Luxshare, which fell -2.95% on news that Apple will set up a plant in India. Northbound Stock Connect volumes were moderate as foreign investors bought $1.036 billion worth of Mainland stock as Northbound trading accounted for 7.7% of Mainland turnover. CNY appreciated versus the US dollar, bonds were mixed, and copper gained +1.13% in China.

There was little to no explanation for US-listed Chinese companies’ weakness yesterday, which frankly left me dumbfounded. There was chatter that tutoring programs in Beijing might be stopped as a coronavirus precaution, which led to US-listed TAL Education falling -11.64%. However, this drop is unreasonable as TAL has a much bigger online presence compared to offline.

Online anti-monopoly rules may have been another culprit as investors bet that Premier Li’s speech and the Two Sessions would lead to more rules, but that is not what happened. Just as there has been a focus on the risks presented by US-listed Chinese stocks with no examination of the rewards, the same is true for these anti-monopoly rules. Who can comply with the rules? The big companies! Big US financial firms love regulation because they can hire armies of lawyers. Who cannot do that? Small firms! Anti-monopoly rules will level the playing field, but China needs these companies. Look at the Five Year Plan. If you want to raise domestic consumption, doesn’t China need Alibaba, JD, Pinduoduo, and others? I think so! I tweeted (@ahern_brendan) yesterday afternoon that yesterday was a very rare day in which US-listed Chinese companies were down despite CNH, China’s currency that trades during US market hours, was up versus the US dollar. I cannot predict the future, but I gave a heavy hint that yesterday was a good day to buy on weakness. Remember to watch CNH as it provides a clue as to whether headlines have any bite to them.

I mentioned yesterday that China has launched a carbon credit allowance program similar to the EU and California markets. It made me wonder whether Chinese EV manufacturers will be able to sell their credits to polluters at a profit, similar to what Tesla has done in California. Polluters, which are mainly coal-fired electrical plants and industrial plants, pay for the right to pollute by buying credits from firms that do not use them. This provides a strong incentive for polluters to cut down on activity and install green equipment.

South Korean E-Commerce company Coupang (CPNG US) will go public today in the US. “Korea’s Amazon” was founded by Bom Kim after he dropped out of Harvard’s MBA program to launch a Groupon-inspired E-Commerce company in Korea. In a highly urbanized country like South Korea, fast delivery led to rapid growth. Then, the coronavirus pandemic accelerated revenue growth. Revenue in 2020 was 2X that in 2019, growing from $5.787 billion to $11.045 billion, though the company still lost $513 million in 2020. Investors are apt to give the company a pass.

Pinduoduo announced today that they will report on March 17th.

JD Power founder JD “Dave” Power, whose firm is known for their auto rankings, passed away recently. Born in Worcester, MA, Mr. Power went to my alma mater, to which he later became a very generous donor. I make a slight hat tip to Mr. Power in today’s headline.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.49 versus 6.51 yesterday

- CNY/EUR 7.75 versus 7.74 yesterday

- Yield on 1-Day Government Bond 1.50% versus 1.50% yesterday

- Yield on 10-Year Government Bond 3.25% versus 3.24% yesterday

- Yield on 10-Year China Development Bank Bond 3.66% versus 3.65% yesterday

- China’s Copper Price +1.13% overnight