US Treasury Yields Give Asia Altitude Sickness, Week in Review

3 Min. Read Time

Upcoming Event

Join us on Thursday, March 25th at 9:00 am EDT for our event:

KraneShares’ Future of Green ETFs Summit.

Click here to register.

Week in Review

- China released overwhelmingly positive trade data as exports continue to grow in 2021. However, the upbeat release was overshadowed in the markets by pressure on growth stocks.

- Growth stocks recovered as the week progressed. Asian investors cheered Fed Chairman Powell’s remarks on sticking to a policy of lower for longer despite yield curve movement.

- E-Commerce platform Pinduoduo announced Wednesday that its revenues grew by +146% year-over-year in the fourth quarter of 2020. As quarantines mostly ended in China in mid-2020, the Q4 year-over-year earnings growth rates for China’s internet firms are pandemic-agnostic and therefore demonstrate that online consumption will continue to grow even without a pandemic.

- Weibo, commonly referred to as the "Twitter of China," announced Thursday that the company grew revenues by +10% to $513 million in Q4 2020, versus analyst expectations of $497 million.

Key News

Asian equities ended the week with a thud, negating gains from earlier in the week, though India gained today despite having a loss for the week. The US Treasury 10-Year yield rising to 1.75% weighed on US equities, which followed through to Asian equities overnight. However, the Treasury yield has fallen back below 1.7%, which is apt to give stocks some support. Our prediction that the US-China Alaska meeting would delve into an “airing of grievances” came to fruition on day one. The theatrics were performed with the media present. It is interesting that each side played to the media for their domestic audience. We’ll find out if day two is more constructive.

Equity markets were spooked by the rising yields and universally negative media coverage of the US-China meeting, but guess who didn’t care? CNH! CNH is the version of China’s currency that trades during US market hours. It is a very reliable indicator to determine whether political bark has any bite to it. No movement tells us not to believe the hype.

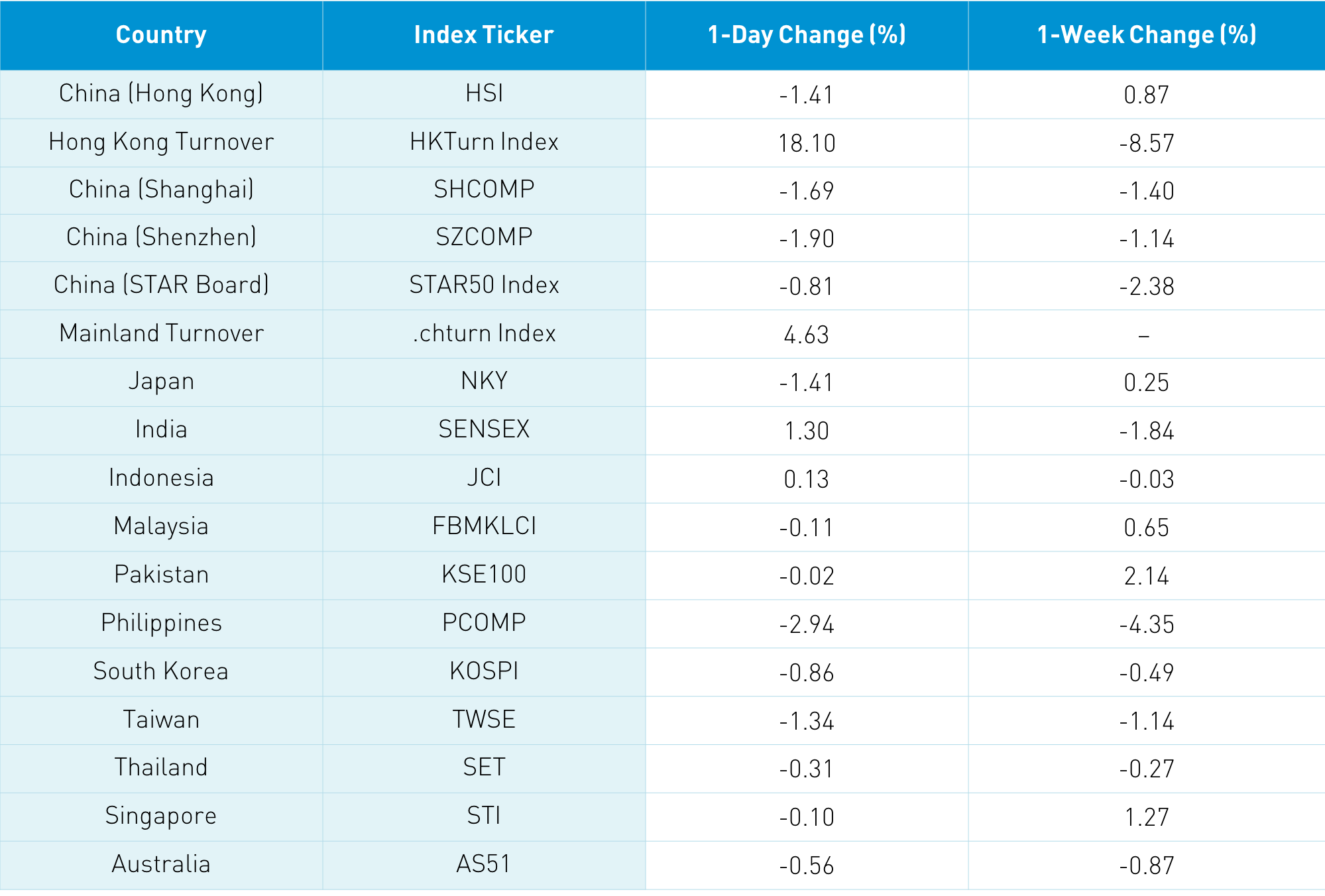

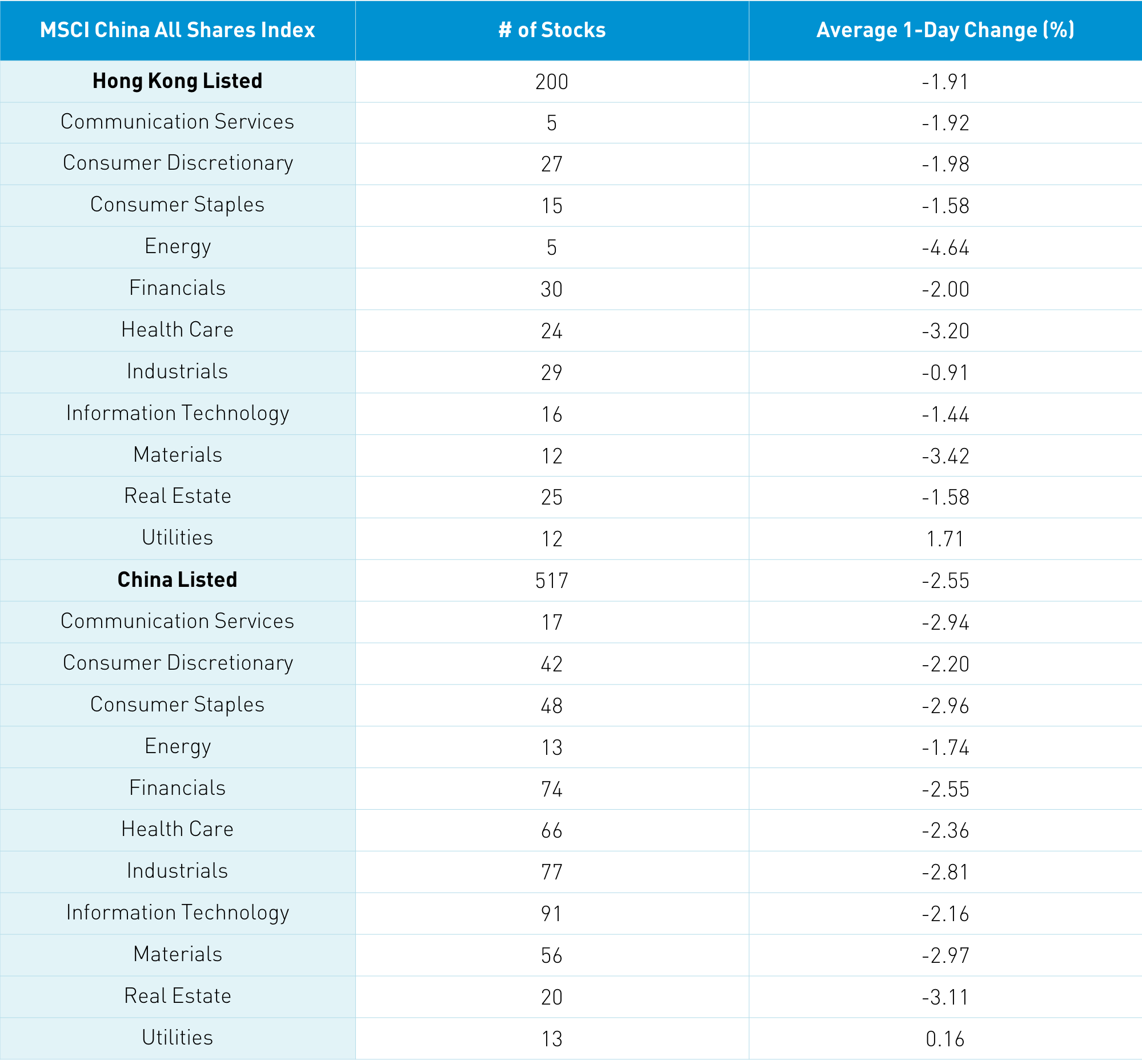

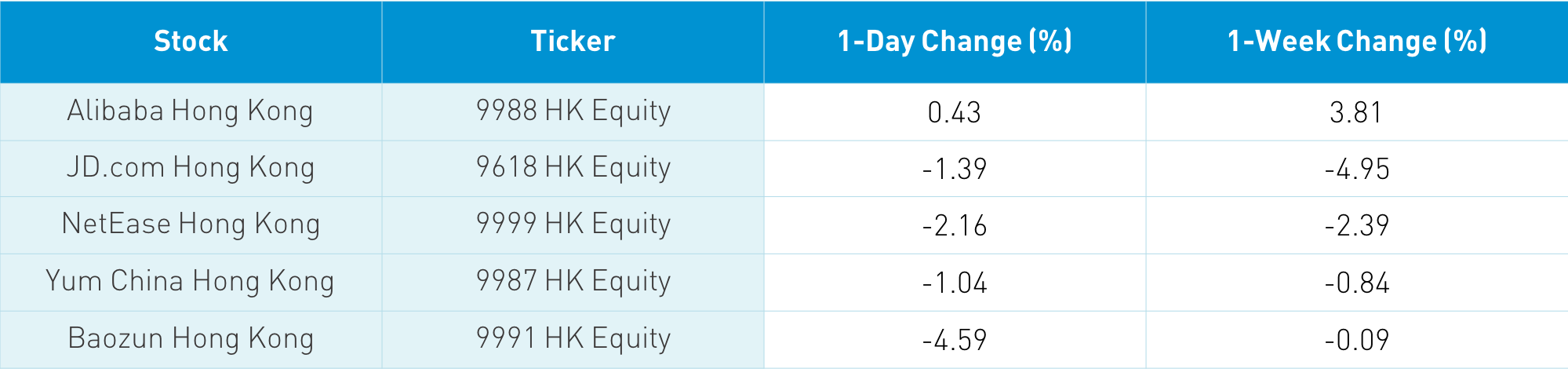

The Hang Seng Index slumped -1.41% while the 200 Chinese stocks listed in Hong Kong and within the MSCI China All Shares Index fell -1.91% as utilities were the only positive sector today. Breadth was awful as 4 stocks fell for every 1 advancer while volume rose +18% from yesterday, which is 134% of the 1-year average. Hong Kong volume leaders were Tencent, which fell -1.95% despite buying from Mainland investors via Stock Connect, Alibaba Hong Kong, which rose +0.43% as FTSE’s indexes transition from the US share class to the Hong Kong share class, Meituan, which fell -1.3%, Xiaomi, which gained +0.19%, CNOOC, which fell -4.68% on heavy selling from Mainland investors via Stock Connect, Ping an Insurance, which fell -1.15%, Kuaishou Tech, which was off -0.63%, Hong Kong Exchanges, which dropped -0.64%, GCL-Poly Energy, which fell -10.97%, and AIA, which fell -0.56%.

Southbound Connect volumes were light as Mainland investors sold $419 million worth of Hong Kong stocks today as Southbound trading accounted for 10.6% of Hong Kong turnover. Shanghai, Shenzhen, and the STAR Board were off -1.69%, -1.9%, and -0.81%, respectively, which swung the weekly return to negative. The 517 Mainland stocks within the MSCI China All Shares Index lost -2.55% today as Mainland breadth was off with 1,445 advancers and 2,438 decliners. Volume increased by +4.63% though was still -11% below the 1-year average. Mainland volume leaders were Ping An, which fell -2.19%, Kweichow Moutai, which was off -2.88%, TCL Tech, which fell -6.26%, CATL, which dropped-5.75%, Longi Green Energy, which was off -4.7%, Sungrow Power, which fell -8.88%, East Money, which fell -3.86%, SF holding, which was off -6.52%, Wuliangye Yibin, which fell -3.55%, and Luxshare, which fell -7.1%. Northbound Stock Connect volumes were moderate as foreign investors sold $619 million worth of Mainland stocks today as Northbound Connect trading accounted for 8.4% of Mainland trading. CNY was off a touch while bonds rallied and copper fell.

Today is quad witching day, the third Friday of the month of every quarter, when index and stock futures expire along with index and stock options. We also have the FTSE Russell index rebalance, which should make today a very heavy volume day.

Nike reported Q3 fiscal results highlighting the reality that China is three-quarters out of its quarantine. Year-over-year revenue growth by geography were North America, which fell -10%, Europe/Middle East/Africa, which dropped -4%, Greater China, which rose +51%, and the Asia Pacific/Latin America, which fell -7%.

We are in this cyclical/value rotation coming at the expense of growth stocks globally. Yes, reopening plays such as airlines, hotels, amusement parks, and restaurants are going to do great in the coming quarters. Economic activity is going to pick up helping steel companies and such. A steeper yield curve will help banks. Though how sustainable is that growth? I don’t believe it is sustainable in the long-term. Remember China being three-quarters out of quarantine tells us that things are apt to play out here. Exhibit A: China Merchants Bank (3968 Hong Kong) grew net profit in 2020 by 4.8%. The defense concludes its argument.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.51 versus 6.52 yesterday

- CNY/EUR 7.74 versus 7.76 yesterday

- Yield on 1-Day Government Bond 1.58% versus 1.50% yesterday

- Yield on 10-Year Government Bond 3.24% versus 3.26% yesterday

- Yield on 10-Year China Development Bank Bond 3.65% versus 3.67% yesterday

- China's Copper Price -0.70% overnight