Asia Gains, 2021 China GDP Forecast Raised, Week in Review

4 Min. Read Time

Week in Review

- Some elements of the reopening trade were present in the markets this week as some growth stocks came under pressure. Click here for our analysis of this week’s headline-driven “flash crash” in US-listed China internet stocks.

- The PBOC and CSRC, China’s central bank and securities regulator, respectively, reiterated that monetary policy will involve “no sharp turns” in 2021 in speeches on Monday, which soothed Mainland markets.

- Baidu listed in Hong Kong on Tuesday with the goal of raising $3.1 billion through the home market offering.

- Tencent released strong fourth-quarter 2020 results on Wednesday as the company grew revenues by +26% year-over-year, which was slightly above analyst expectations. The company also assured investors that it is in full compliance with new regulations for financial technology platforms and would comply with any and all new internet platform regulations.

Friday’s Key News

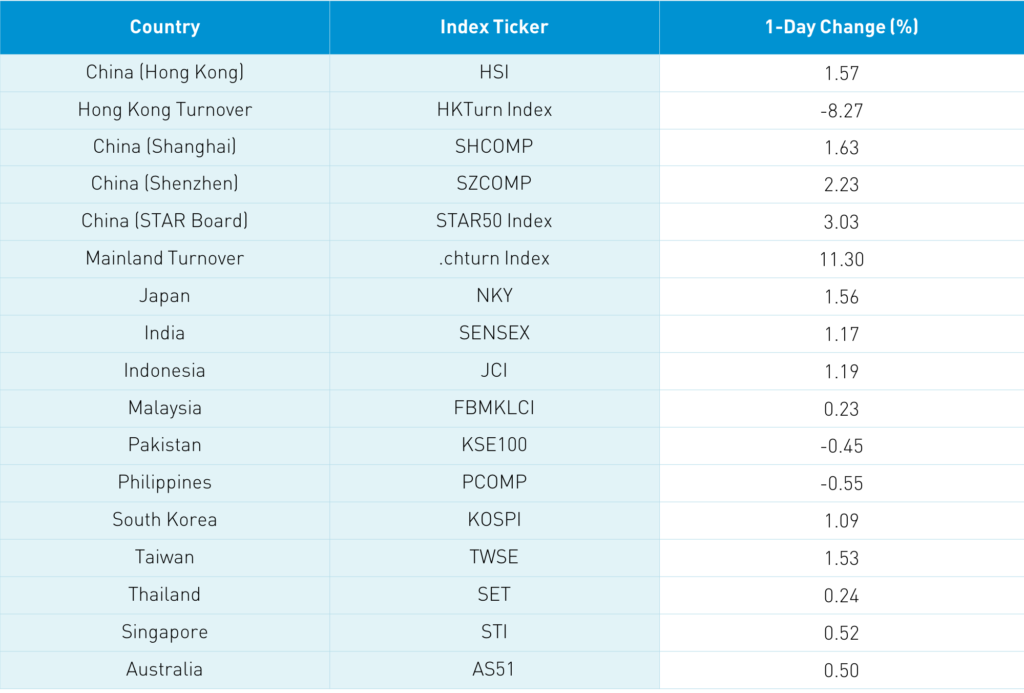

Asian markets finished in the green. I was shocked to see Shanghai and Shenzhen were up +0.4% and +0.91% this week while Hang Seng lost -2.26%. However, candidly it felt worse due to the below reasons.

By far the biggest news is chatter this morning that there is a forced seller in several US-listed Chinese stocks. If you use leverage/borrowed money to buy stocks when they decline you have to add cash to the account. If you can’t add the cash, the broker sells your shares, regardless of price. This would explain the flash crash we saw on Wednesday. Why did this affect the whole space? Because once one domino goes, it forces others to act. My parents taught me debt is the root of all evil. Someone learned a very hard lesson this week. Unfortunately, we were all affected. Would hope/speculate the market will bounce back once the forced seller is out of the equation.

Yes, we have worries about China's internet regulation and, yes, we had the SEC say they would start to identify companies due to the Holding Foreign Companies Act (HFCA). The China regulation is multi-faceted: personal data protection, fintech companies becoming regulated like banks, anti-competitive practices going away, and anti-monopoly rules.

As Tencent’s President stated on their earnings call, Tencent has complied with the fintech regulations. These companies are critical to China’s economy. I don’t see that changing.

On the HFCA front, there is a path for the companies to comply by disclosing whether China’s government owns them and whether management includes members of the party. What is the big deal with filing that information in a report no one reads? Ultimately, these companies are growing at a tremendous rate that I believe will continue as China continues to urbanize, growing the urban middle class, who will continue to grow China’s already sizable domestic consumption.

Bloomberg Economics revised up its China GDP growth projection for 2021 to 9.3% from 8.2%. However, the PBOC estimates GDP growth to average 6% over the next five years. 2021 GDP will be coming off a low base and will also benefit from momentum stemming from China’s strong rebound in the second half of 2020.

The PBOC stated that its central bank digital currency will complement, rather than replace, existing digital payments networks run by Ant Group and Tencent. As we have mentioned before, the PBOC will likely need to work with these firms to spur user adoption of the currency. The PBOC also said that the central bank digital currency will serve as a backup for private payments networks, ensuring stability and reliability in the financial system. The central bank is keen to roll out the currency as, from their perspective, it will allow for more efficient monetary policy given better data and control.

It was a relatively quiet news day though some political rhetoric concerns continue. President Biden’s comments on China in yesterday’s press conference did not help assuage concerns over the future of the relationship, but he did stress that his administration is not looking for confrontation. Climate change is a potential area of cooperation between the two superpowers, and I believe common ground will be found leading up to the G20 climate summit, which the US and China are co-chairing, though the summit is not until October.

China's largest banks are reporting earnings for the fourth quarter of 2021. The dividends these banks are offering are at a premium to those offered by global banks. This is also a function of higher treasury yields in China.

H-Share Update

The Hang Seng gained +1.57% though the 200 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index gained +2.47%. While we had 3 to 1 advancers to decliners, turnover was light in Hong Kong. I’d like to see more conviction in the buying. Hong Kong volume leaders by value were Tencent, which gained+2.31%, Xiaomi, which gained +6.28% after announcing they are getting into EVs, Baidu, which fell -5.56%, Meituan, which fell -5.08%, Alibaba HK, which fell -2.26%, HK Exchanges, which gained +3.02%, China Mobile, which fell -0.49%, Wuxi Biologics, which gained +6.64%, Anta Sports, which gained +5.61% at Nike’s expense, and Great Wall Motors, which gained +10.38% as they were rumored to be Xiaomi’s partner, though they denied this after the market’s close. Southbound Connect volumes were light though Mainland investors bought $776 million worth of Hong Kong stocks as Southbound Connect trading accounted for 11.9% of Hong Kong turnover. Tencent saw MASSIVE buying while Meituan also had buyers and Xiaomi.

A-Share Update

Shanghai, Shenzhen, and the STAR Board gained +1.63%, +2.23%, and +3.03%, respectively, as bargain hunters lifted the market. Volume was up 11% from yesterday though still below the 1-year average. Shanghai and Shenzhen are sitting on support levels. Discretionary, staples, healthcare, industrials, tech, and materials all had strong days. Northbound Stock Connect had a strong day with $983 million in inflows as Northbound connect accounted for 8.3% of Mainland turnover. CNY was off on dollar strength and copper gained a touch.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.54 versus 6.55 yesterday

- CNY/EUR 7.71 versus 7.72 yesterday

- Yield on 1-Day Government Bond 1.25% versus 1.25% yesterday

- Yield on 10-Year Government Bond 3.20% versus 3.19% yesterday

- Yield on 10-Year China Development Bank Bond 3.59% versus 3.57% yesterday