Forced Deleveraging and Meituan Results Weigh on Growth Stocks

4 Min. Read Time

Key News

Friday’s report spoke to the deleveraging sell-off in several US-listed Chinese ADRs as an Asian family office was liquidated after China’s correction post-Chinese New Year. This led to margin calls, which could not be met. When one cannot meet a margin call, brokers unwind your position regardless of price in order to limit their exposure. We sent a Tweet at 10:16 am Friday via @ahern_brendan stating that Tencent Music Entertainment, Baidu, and Vipshop were affected. Over the course of Friday’s trading, iQiyi and GSX Techedu also had massive blocks sold at deep discounts followed by similar discounted block trades in ViacomCBS, Discovery Inc’s Class A and K share classes, Shopify, and Farfetch. The family office did not own the stocks directly, which would have led to regulatory filings, but through swaps with brokers using leverage. This morning, we were met with reports that two institutional brokers suffered losses due to their exposure to the family office.

How much more selling is there to come? It’s hard to say, but there was talk that this unwinding may have started the week before last and that Friday was just the final flush. The media is hyping contagion from the event, which is feasible. However, the severity of the post-Chinese New Year correction has likely forced out other levered players. One positive sign was that Tencent Music Entertainment announced a $1 billion buyback. We are likely to see sell-side analysts reiterate their ratings based on the stock prices. If the stocks were pushed down severely from this deleveraging, the seller has been removed.

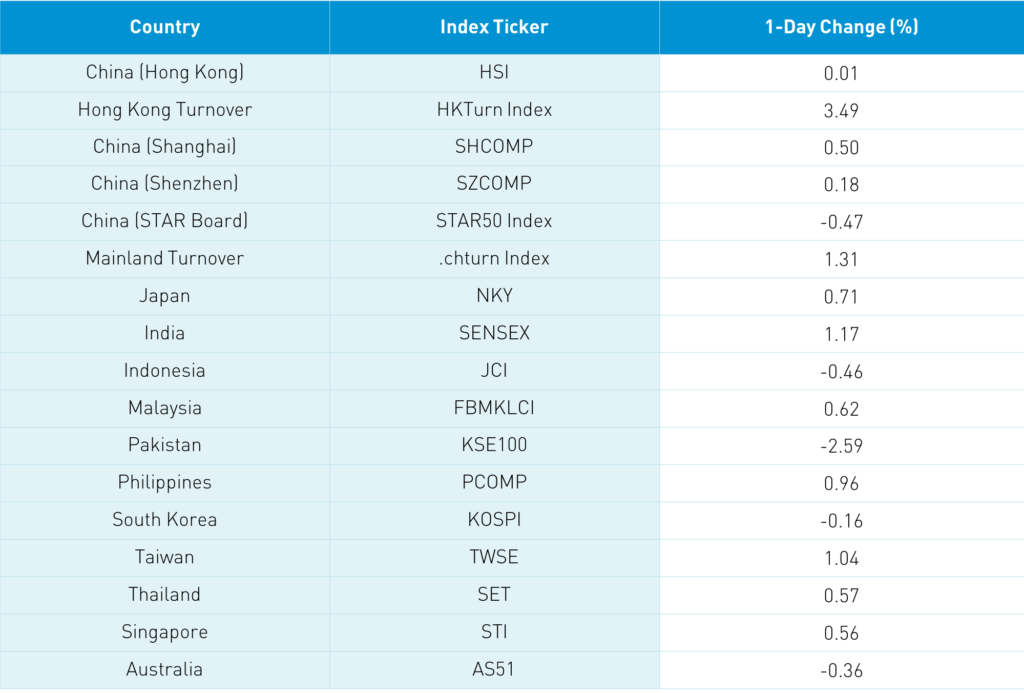

Asia had a decent day overnight as most markets were up, though Korea was off and Pakistan was off heavily. Friday’s fallout in US-listed Chinese stocks weighed on growth stocks, which was exacerbated by Meituan’s Q4 results reported after the Hong Kong close Friday. We also had state media warning consumers about exaggerated electric vehicle claims, which sent the space lower.

The weekend’s edition of the Wall Street Journal included an interview with US Trade Representative Katherine Tsai that is a worthwhile read. While acknowledging the negative impact of tariffs, they will stay on as “Every good negotiator retains his or her leverage to use it”. US consumers and manufacturers will continue to pay for the tariffs through higher prices. The article failed to acknowledge that if one were to include goods manufactured and sold in China by US companies to the definition of trade, there is no trade deficit!

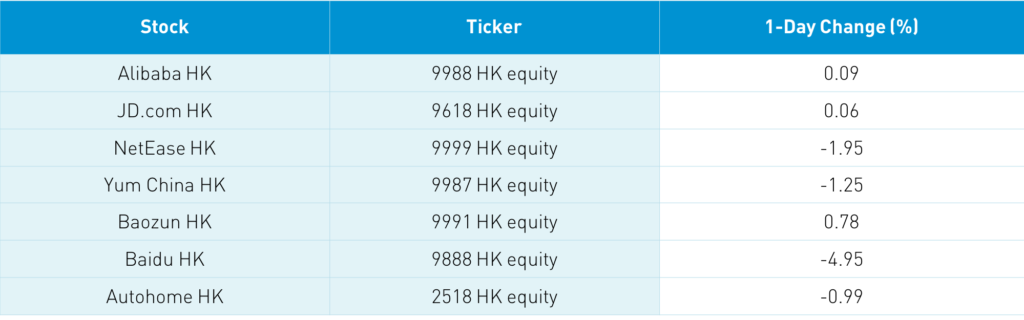

Bilibili relisted in Hong Kong today under ticker 9626 HK. Shares were off -0.99% in Hong Kong though appear up pre-market.

Takeaway: The year-over-year comparison was a low bar considering China was in quarantine a year ago. Compared to 2019, the results still look strong at +72.1%. This was not a market-moving release.

Meituan Q4 Earnings Overview

Lost in the madness of Friday and receiving my vaccine shot that morning was Meituan’s Q4 financial results, which were reported after the close in Hong Kong Friday. While top-line growth was very impressive the company’s investments to fund future growth took a toll on net income and earnings per share (EPS). The company stated that investors should prepare themselves for more investment as they are growing multiple business units. With the market rotating to quality/net income from growth/revenue growth, the timing is not ideal despite the medium to long-term opportunity for the company.

- Revenue increased +34.7% to RMB 37.917B from RMB28.158B versus analyst expectations of RMB 26.81B

- Revenue by category: food delivery +37% to RMB 21.537B, in-store/hotel/travel +12.2% to RMB 7.135B and new initiatives +51.9% to RMB 9.244B

- Transacting User for year +13.3% to 510.6mm while active merchants +10.1% to 6.8mm (2020 versus 2019)

- Cost of revenues +54.3% to RM 28.461B (75% of revenue), Selling/marketing expenses +43.5% to RMB 7.675B (20.2% of revenue), Research/development expenses +45.1% to RMB 3.249B (8.6% of revenue)

- Adjusted net loss increased 163% to -$1.436B from a profit of RMB 1.46B versus analyst expectations of an RMB loss of -968mm

- Adjusted EPS was RMB -0.24 versus analyst expectations of RMB -0.14

H-Share Update

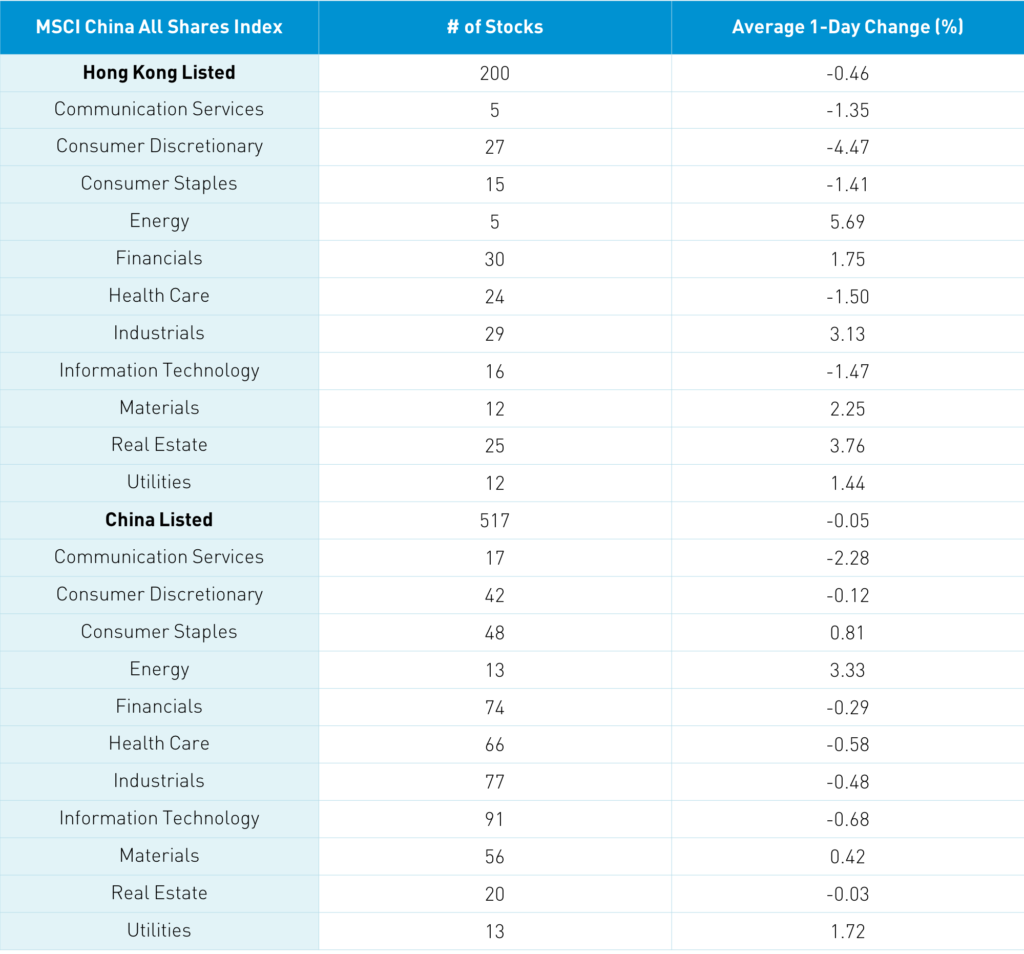

The Hang Seng Index gained +0.01% on volume which was +3.4% higher than Friday and 123% of the 1-year average. There was a touch of the value/cyclical rotation at growth’s expense as we near quarter-end. The 200 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index were off -0.46% as growth sectors were off including discretionary, which fell -4.47%, healthcare, which fell -1.5%, communication, which fell -1.35% and staples, which fell -1.41%. Meanwhile. value sectors gained led by energy, which gained +5.69%, real estate, which gained +3.76%, industrials, which gained +3.13%, materials, which gained +2.25%, and financials, which gained +1.75%. Hong Kong’s most heavily traded stocks were Tencent, which fell -1.29%, Meituan, which fell -7.15%, Baidu, which fell -4.95%, Alibaba HK, which gained +0.09%, Xiaomi, which fell -1.38%, China Construction Bank, which gained +3.25%, HK Exchanges, which gained +0.78%, Bilibili HK, which fell -0.99%, China Xinhua energy, which gained +10.34% on rising coal futures, and China Mobile, which gained +0.49%. Southbound Connect volumes were moderate/light as Mainland investors bought $120 million worth of Hong Kong stocks today as Tencent was bought somewhat, Sunac was sold, and Meituan was sold somewhat as Southbound trading accounted for 13.3% of Hong Kong turnover.

A-Share Update

Shanghai, Shenzhen, and the STAR Board were mixed at +0.5%, +0.18% and -0.47%, respectively, while the 517 Mainland stocks within the MSCI China All Shares Index eased -0.05%. Energy had strong day as coal futures rose and energy companies are expected to pay out sizeable dividends. Turnover was up by a mere +1.3%, which is just 87% of the 1-year average. The two most heavily traded Mainland stocks by value were liquor stocks Kweichow Moutai and Wiliangye Yibin, which gained +1.05% and +2.31%, respectively. Northbound Stock Connect volumes were moderate as foreign investors sold -$889 million worth of Mainland stocks as Northbound trading accounted for 7% of Mainland turnover. Bonds were flat, CNY depreciated versus the US dollar, and copper rallied 1.34%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.57 versus 6.54 Friday

- CNY/EUR 7.74 versus 7.71 Friday

- Yield on 1-Day Government Bond 1.31% versus 1.25% Friday

- Yield on 10-Year Government Bond 3.20% versus 3.20% Friday

- Yield on 10-Year China Development Bank Bond 3.58% versus 3.59% Friday

- China’s Copper Price +1.34% overnight