VIPS & GSX Announce Buybacks, JD Health’s 2020 Results Rip

3 Min. Read Time

Yesterday’s latest rumor on Archegos liquidation involved Wells Fargo selling off their exposure via several block trades in US and Chinese ADRs. Stocks rumored to be involved yesterday were iQiyi, Baidu, Farfetch, and Vipshop. If Goldman Sachs, Morgan Stanley, and Wells Fargo have flushed their exposure, that would leave three remaining prime brokers: Nomura, Credit Suisse, and Deutsche Bank. MS and GS are the two largest prime brokers in the US so one would suspect that the positions of the remaining players would be smaller. There is some evidence of stabilization as non-involved stocks have started to percolate after being swept into the downdraft. This morning Vipshop announced a $500mm buyback while GSX Techedu’s CEO announced that he was buying back $50mm following Tencent Music Entertainment’s $1B buyback announcement. There had been rumors that UBS wanted to buy Credit Suisse, which would be significantly easier today.

Key News

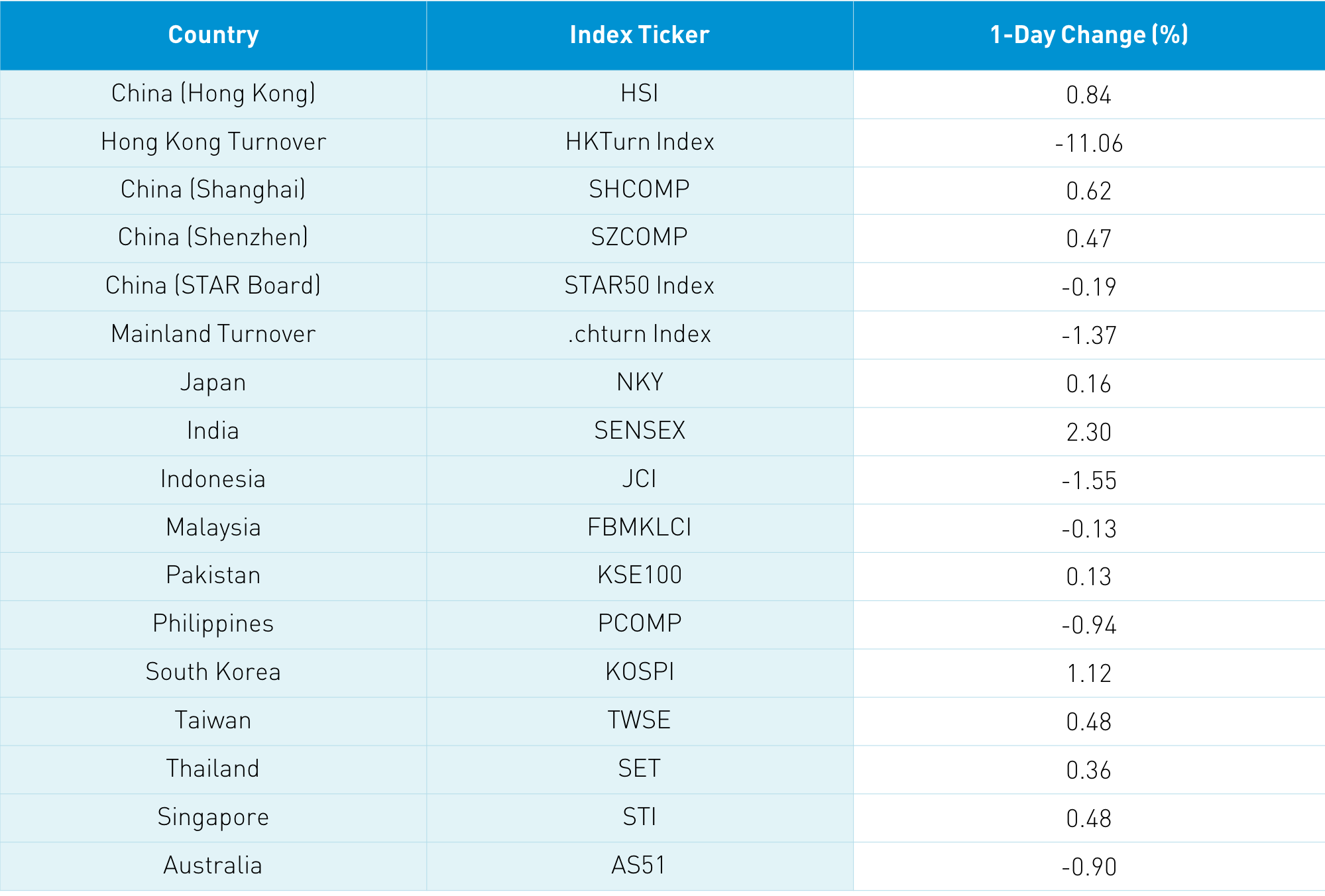

Asian markets were largely higher though Japan was off as companies paid dividends, Meanwhile, India returned from holiday in good spirits. It was fairly quiet on the news front with China’s earning season kicking into full gear. Clean energy was front and center as China’s carbon allowance trading program is expected to launch at the end of June.

There are rumors that the recent fundraisings from Didi, the Uber of China, and Bytedance, known for its TikTok video app, are moves preceding IPOs. Media reports are stating that Bytedance has a $250B valuation. There is talk that Didi will list in the United States, but aren’t US-listed Chinese stocks going to be listed? We continue to see Chinese companies list in the US (Lufax and KE Holdings were big IPOs last year). What do they know that the US media is missing?

FTSE Russell announced it would add Chinese government bonds to its World Government Bond Index (WGBI, the cool traders all pronounce it Wig Bee), beginning in October and taking place over thirty-six months leading to a 5.25% weight. The move follows Bloomberg Barclays’ addition of Chinese government bonds last year to its Global Aggregate last year. According to Bloomberg, the WGBI inclusion is expecting more than $100B of foreign capital to China’s bond market, which has more than $300B of foreign ownership today, accounting for 11% of total ownership.

Online pharmacy and health care products provider JD Health (6618 Hong Kong) reported very strong 2020 financial results after the Hong Kong close yesterday. The company had a large loss due to the value change in its convertible shares, though analysts will remove this accounting loss from results as it isn’t a cash flow loss. The RMB 17.5B loss led to a dramatic disparity between IFRS (GAAP) and adjusted results. It is interesting to note that JD Health is considered a consumer discretionary company rather than a healthcare company.

- Revenue increased +78.8% to RMB 19.382B beating analyst expectations of RMB 18.561B

- Active annual users were 89.8mm

- Gross profit increased +74.9% to RMB 4.917B

- Loss for the year increased +1,673% to RMB 17.234

- Adjusted profit for the year increased +117% to RMB 748mm beating analyst expectations of RMB 410mm

- Adjusted EPS RMB 0.33 versus analyst expectations of RMB -0.40

- Cash at year-end was RMB 32.27B from RMB 4.965

H-Share Update

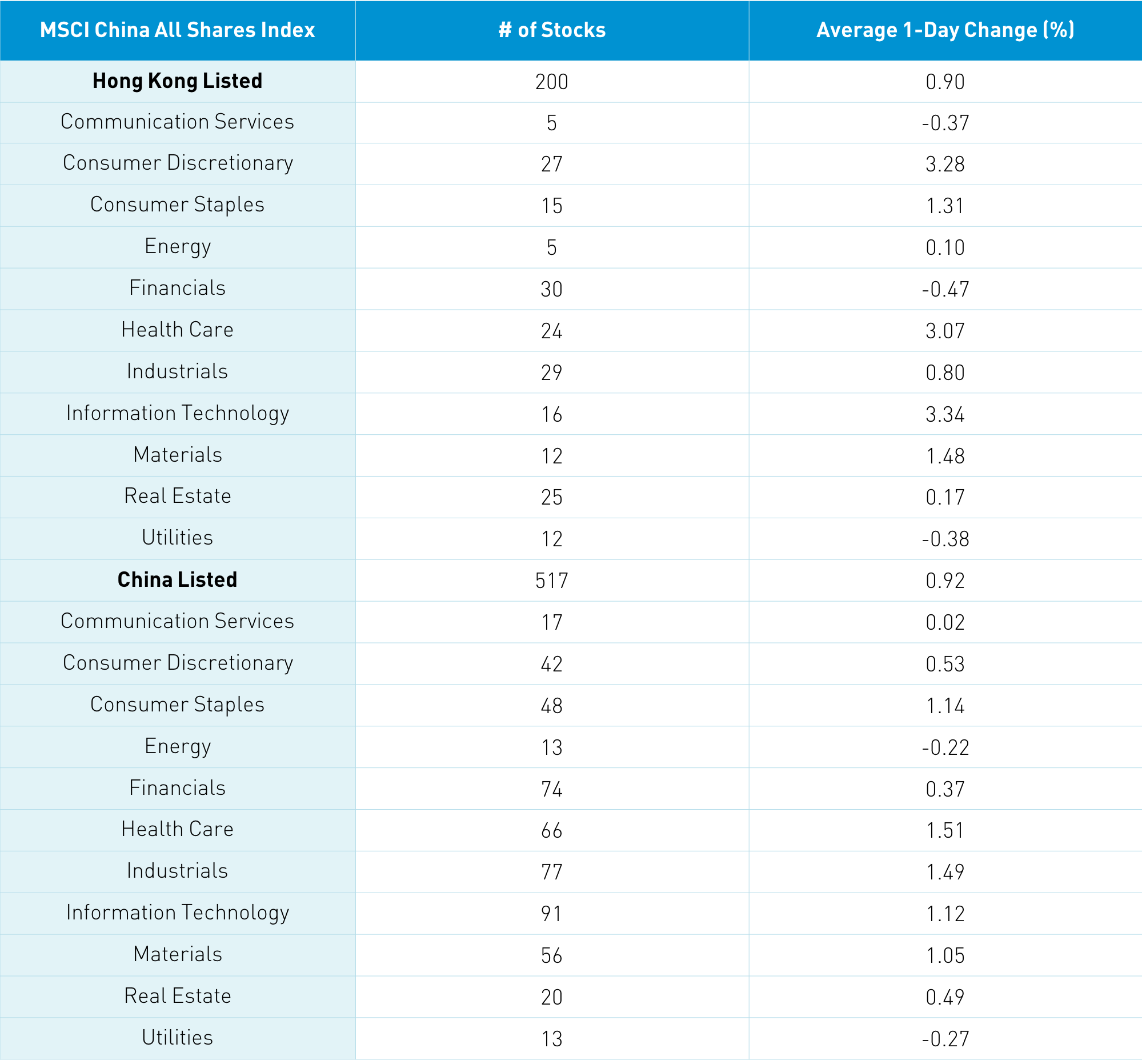

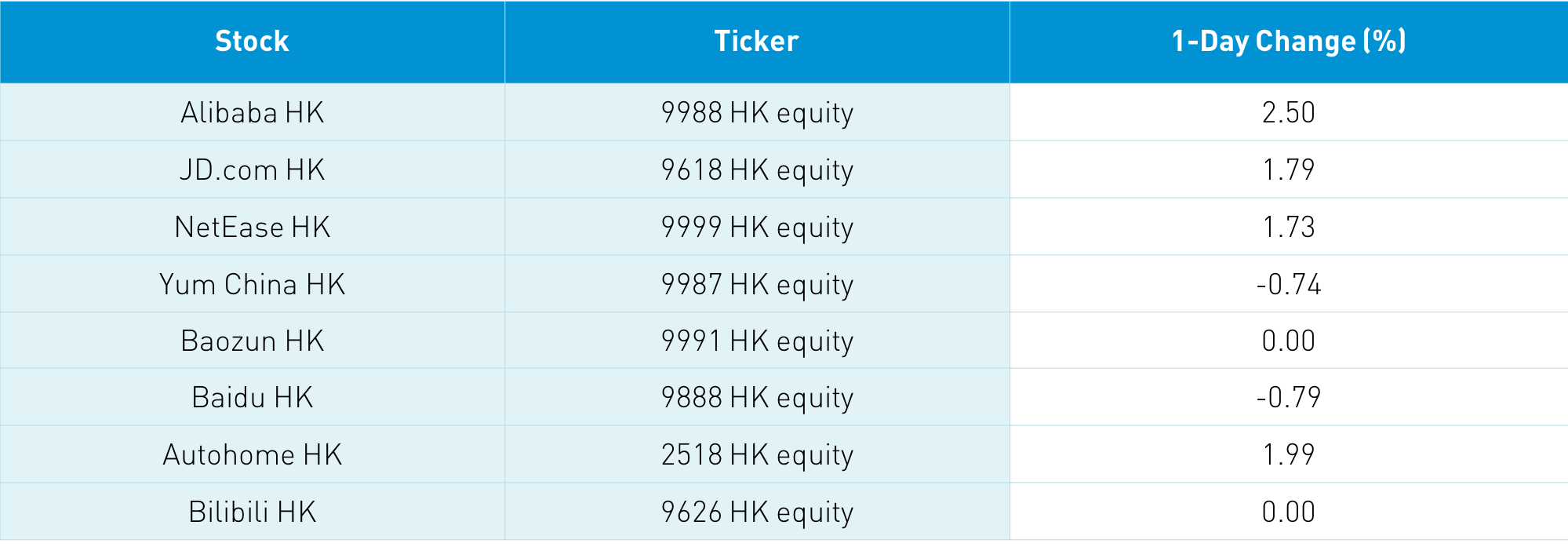

The Hang Seng gained +0.84% led by growth stocks/sectors, though once again it is on light volumes, which declined -11% from yesterday to just above the 1-year average. The 200 Chinese companies listed in Hong Kong within the MSCI China All Shares Index gained +0.9%, led by tech +3.34%, discretionary +3.28%, and healthcare +3.08%, while financials, utilities, and communication were all off less than -0.5%. Hong Kong volume leaders by value traded were Tencent, which fell -0.41%, Alibaba Hong Kong, which rose +2.5%, Meituan, which was up +4.71%, Baidu Hong Kong, which fell -0.79%, Xiaomi, which gained +2.2% after announcing it will get into EVs, BYD, which fell -0.41% after 2020 results were good/not great though Q1 estimates were very strong, Wuxi Biologics, which gained +2.08%, China Construction Bank, which was off -1.2%, Lenovo, which rose +12.35%, and Ping An, which fell -0.16%. Mainland investors bought $418mm of Hong Kong stocks today on light volumes as Southbound trading accounted for 10.8% of Hong Kong turnover. Tencent had very large buying as an FYI.

A-Share Update

Shanghai, Shenzhen, and STAR Board returned +0.62%, +0.47%, and -0.19% respectively as volume declined -1.37% to just 86% of the 1-year average. Breadth had 1,146 advancers and 2,745 decliners. The 517 Mainland stocks within the MSCI China All Shares Index gained +0.82%, led by healthcare +1.41%, industrials +1.4%, staples +1.04%, and tech +1.02%, while energy and utilities were off -0.32% and -0.36% respectively. Clean energy and liquor had a strong day as Mainland volume leaders by value traded were Longi Green Energy, which rose +9.25%, Sungrow Power, which was up +10.66%, Kweichow Moutai, which gained +1.08%, BYD, which was up +0.54%, Shenzhen Energy, which rose +0.08%, Tongwei, which gained +5.59%, and Wuliangye Yibin, which was up +0.5%. Northbound Connect volume was moderate/light as foreign investors bought $579mm of Mainland stocks today as Northbound trading accounted for 6.5% of Mainland turnover. Bonds rallied though CNY eased versus the US $ while copper rallied.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.57 versus 6.57 Yesterday

- CNY/EUR 7.70 versus 7.74 Yesterday

- Yield on 1-Day Government Bond 1.31% versus 1.31% Yesterday

- Yield on 10-Year Government Bond 3.21% versus 3.20% Yesterday

- Yield on 10-Year China Development Bank Bond 3.58% versus 3.58% Yesterday

- China’s Copper Price -0.20% overnight