Tencent Investor Sale Teaches Diversification The Hard Way

3 Min. Read Time

Upcoming Event

Join us tomorrow at 11:00 am EDT for our event:

The Return of Volatility: Navigating Market Risk With Managed Futures.

Click here to register.

Key News

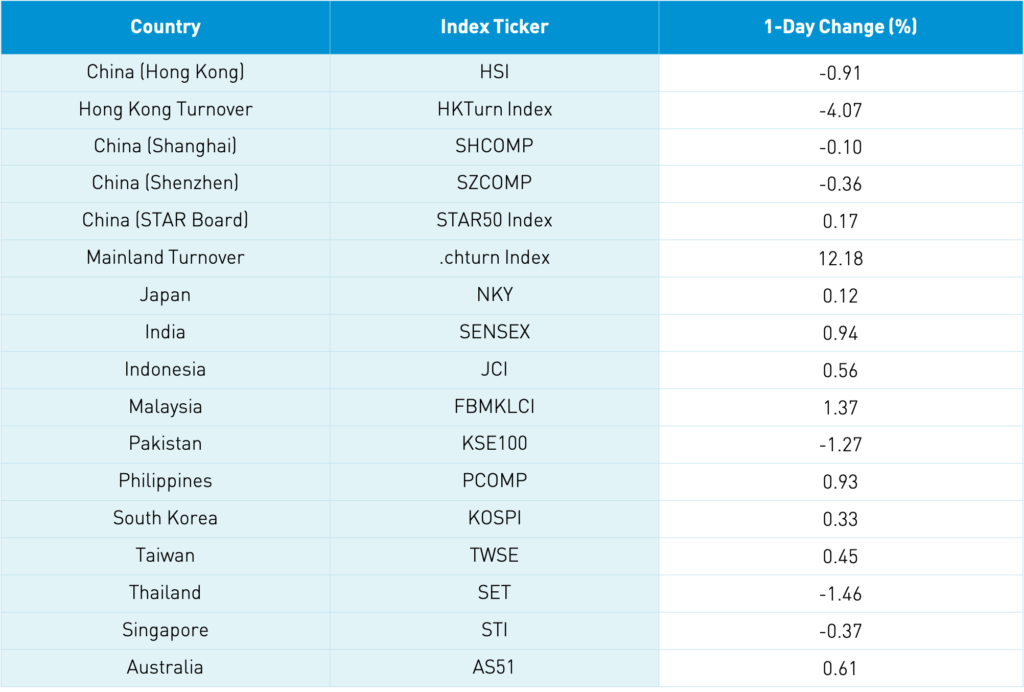

Asian equity markets were all open today as most gained, albeit on lighter volume than normal. South Korea gained on strong volume following Samsung’s positive Q1 guidance. Meanwhile, Thailand was off on strong volume while China and Hong Kong were off on weak volume. Despite the strong PMI releases and the IMF raising China’s GDP target to 8.4%, rumors that the US may boycott the 2022 Beijing Olympics weighed on sentiment while the value/cyclical/reopening trade outperformed at the expense of the growth/work from home trade. Electric vehicle plays were hit with profit-taking despite the reporting of strong March sales while Chinese steel stocks outperformed.

After the close, Tencent investor Prosus announced that it is selling 2% or 191 million of its shares in the company, which would raise $14.6B. Prosus is an Amsterdam-listed company comprised of non-South African holdings of Naspers, whose $32 million investment in Tencent back in 2001 is now worth $239 billion. The sale brings Prosus’ stake in Tencent to 29%, though the company pledges not to sell again for three years. We have warned about holding Tencent, Prosus, and Naspers shares at the same time because doing so would be tripling down on Tencent as they move with one another.

Coincidentally, two Tencent investments are rumored to be evaluating spinoffs through public listings: South Korean gaming company Krafton, which is famous for the PUBG video game, and online grocer company Missfresh following We Doctor’s Hong Kong IPO filing a week ago.

A Mainland media source noted that China is examining real estate taxes. This will be something to keep an eye on.

Baidu will be added to the Hang Seng Composite Index tomorrow. Meanwhile, Trip.com (TRIP US, formerly C-trip.com) appears to be getting closer to listing in Hong Kong

I read an interesting article on Legos winning a trademark infringement case in China against a company that had violated copyright law by copying the company’s famous bricks. The violating company owes a fine of $4.7 million and the company’s CEO was sentenced to jail for six years.

Takeaway: Reserves declined -1.1% month-over-month though have risen by +3.6% year-over-year. The decline was driven by the US dollar’s rise and declining bond prices.

H-Share Update

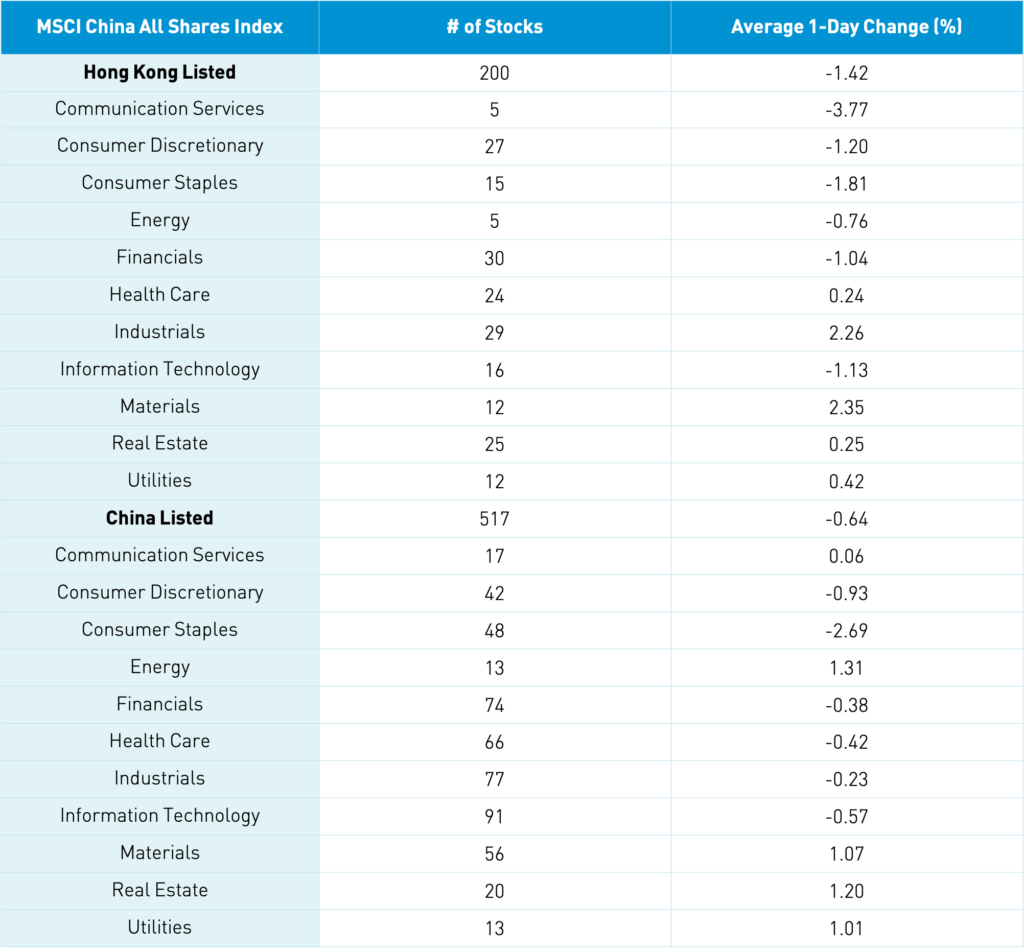

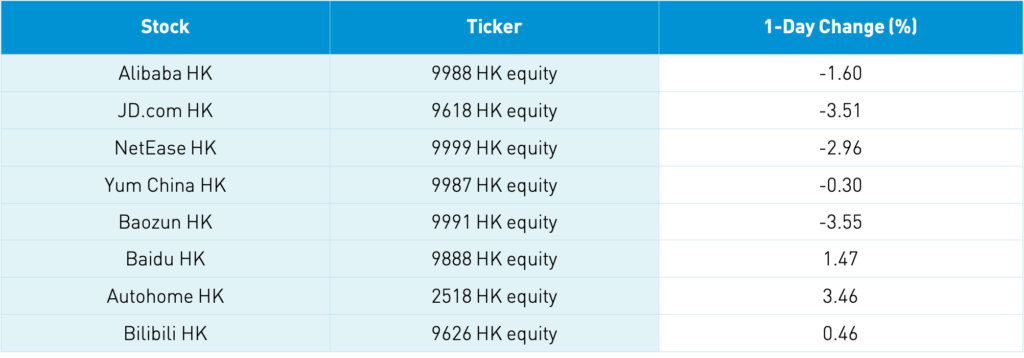

The Hang Seng was off -0.91% while the Chinese companies listed in Hong Kong and within the MSCI China All Shares Index were off -1.42%. Materials and industrials were up +2.33% and +2.24%, respectively, while communication was down -3.79% due to Tencent, staples lost -1.83%, discretionary lost -1.22%, and tech lost -1.15%. Hong Kong volume leaders by value were Tencent, which fell -3.75%, Meituan, which fell -2.39%, Alibaba HK, which fell -1.6% despite Charlie Munger’s Daily Journal filing an investment in the company, Xiaomi, which fell -0.57%, SMIC, which fell +5.02%, HK Exchanges, which fell -2.39% on talk that the group may launch a Mainland FX futures exchange, COSCO shipping, which gained +29.11% after raising financial forecasts driven by strong demand as the global economy comes online, Ping An Insurance, which fell -0.43%, Wuxi Biologics, which gained +1.43%, and AIA, which fell -1.63%. JD.com was off -3.51% after its fintech unit pulled its Star Board IPO as the company likely has to refile its financials after the new fintech rules. Volumes were down -4.19% from last Thursday, which is 109% of the 1-year average. Southbound Stock Connect volumes were light as Mainland investors bought $109 million worth of Hong Kong stocks as Southbound Connect trading accounted for 12.3% of Hong Kong turnover as Tencent was a rare net sell.

A-Share Update

Shanghai, Shenzhen, and the STAR Board diverged -0.1%, -0.36%, and +0.17%, respectively, as volume rose +12.18% from yesterday though was just 84% of the 1-year volume. Value sectors outperformed with energy +1.31%, real estate +1.2%, materials +1.07%, and utilities +1%. Meanwhile, staples -2.7% and discretionary -0.93%. Due to the strong credit growth earlier this year, there are concerns credit expansion will be curtailed. The Mainland’s most heavily traded stocks by value were BOE Tech, which gained +2.82%, Kweichow Moutai and Wuliangye Yibin, which fell -3.06% and -4.88%, respectively, after a famous Mainland mutual fund manager cut his position in another liquor play, Longi Green Energy, which fell -4.37% after being hit with profit-taking, BYD, which fell -2.9%, broker East Money, which fell -2.55%, Luzhou Laojia, which fell -6.11%, CATL, which fell -1.79% on profit-taking in electric vehicles, TCL Tech, which gained +1.23%, and GeM Co., which gained +3.58%. Foreign investors sold -$430 million worth of Mainland stocks as Northbound Connect trading accounted for 8.9% of Mainland turnover as Kweichow Moutai was bought in size. Bonds were weaker while CNY gained versus the US dollar and copper eased a touch.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.54 versus 6.54 yesterday

- CNY/EUR 7.78 versus 7.75 yesterday

- Yield on 1-Day Government Bond 1.54% versus 1.59% yesterday

- Yield on 10-Year Government Bond 3.22% versus 3.21% yesterday

- Yield on 10-Year China Development Bank Bond 3.61% versus 3.59% yesterday

- China's Copper Price -0.19% overnight