Investors Cheer China’s Q1 Economic Release, Week in Review

4 Min. Read Time

Upcoming Webinar

Join us on Tuesday April 20th at 11:00 am EDT for our event:

Diving Into Dividends: 3D/L Capital Management co-CIOs Make the Case for Yield

Click here to register.

Week in Review

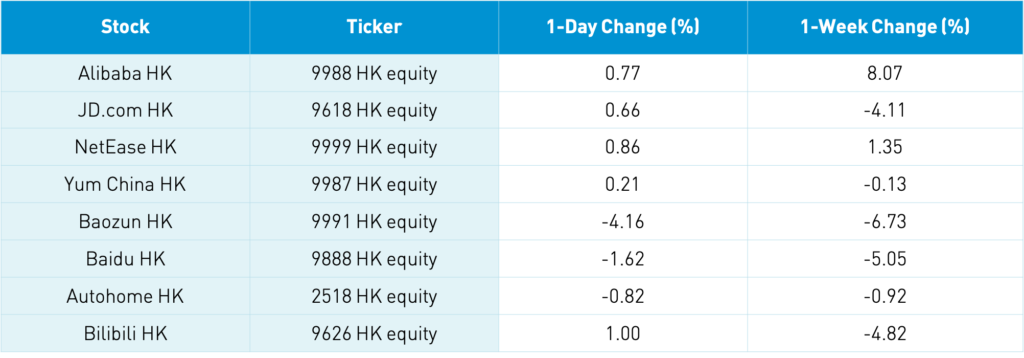

- Alibaba’s Hong Kong share class gained +6.52% Monday after the State Administration of Market Regulation (SAMR) fined Alibaba $2.8 billion for its anti-competitive practices. Fortunately, the company has $47.8 billion in cash to cover the fine, which could have been much higher. The SAMR also published guidelines for avoiding fines in the future and most major affected firms have assured investors of compliance with the new rules.

- China’s imports beat expectations while exports were a touch light in March, according to a Tuesday release. Exports to the US grew +53.3% YoY to $38.66B while EU exports grew +45.9% to $36.56B.

- Asian equities had a strong session on Wednesday as growth names outperformed following more certainty around the regulation of internet firms and financial technology platforms.

- The PBOC’s Thursday open market operations came in slightly below the amount of maturing loans to banks, indicating a slight tightening of monetary policy. However, the central bank continues to pursue a policy of “no sharp turns” in 2021.

Economic Data Release Overview

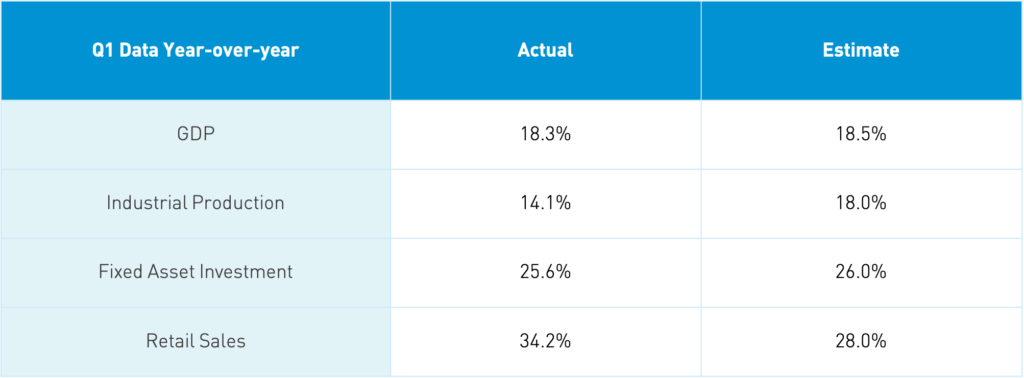

Takeaway: We knew the 10 am local time release was going to be strong since the economic data is a year-over-year (YoY) comparison from 2020’s quarantine reduced levels. Yes, GDP came in a touch light and industrial production was off. However, investors largely cheered the release as GDP saw the highest year-over-year growth since 1992. Within GDP, the primary industry is agriculture because when China first started calculating GDP agriculture was the largest segment of the economy. By contrast, today it is a distant third at RMB 1.13 trillion. The agricultural sector grew +8.1% YoY. The secondary industry, which is construction/manufacturing at RMB 9.26 trillion, grew +24.4%. Meanwhile, the third industry, the services sector, which is worth RMB 14.54 trillion, grew +15.6%.

Industrial output missed estimates, but one culprit was a sharp contraction in coal output, which fell -0.2% YoY as China begins to take carbon neutrality seriously. Motor vehicle output increased +69.8% to 2.5 million vehicles, led by electric vehicle output, which grew +237.7% YoY to 233,000 units. Categories within retail sales all saw strong growth in the first quarter, with restaurants surging +91.6% and jewelry sales growing +83.2%. The value of urban retail sales was 8X greater than rural, showing the huge effect continued urbanization could have in the decades to come. Urban residents had twice the personal income of rural residents in Q1.

Key News

Asian equities ended the week on a positive note, cheering yesterday’s US economic data release and China’s economic release today on a quiet night from a news perspective though volumes were light. Chinese investors noted that a large European China mutual fund is increasing its exposure to liquor stock Kweichow Moutai. Like investors in the US, Chinese investors study star mutual fund managers.

Leaders from China, France, and Germany held a video climate change summit Friday. PBOC Governor Yi Gang spoke yesterday at the China Development Forum on what China needs from the financial community to reach peak carbon emissions by 2030 and carbon neutrality by 2060. He noted that China is already the largest green finance market globally, though a significant amount of work remains to be done.

Trip.com (TCOM US) will list on Monday in Hong Kong under ticker 9961 HK as retail investors are oversubscribed 17X while the institutional offering was 5X oversubscribed. Bloomberg is reporting that shares are up +3% in over-the-counter trading. We also heard that Tencent’s We Doctor is making progress on its Hong Kong IPO.

Distressed debt manager Huarong, which appears to be in distress itself, made a payment covering a maturing bond today. Over the years, I have witnessed several other companies run into problems that the media implied would the first domino in a Chinese financial crisis. This is the latest. And, as always, coverage fails to put one firm’s troubles in perspective.

H-Share Update

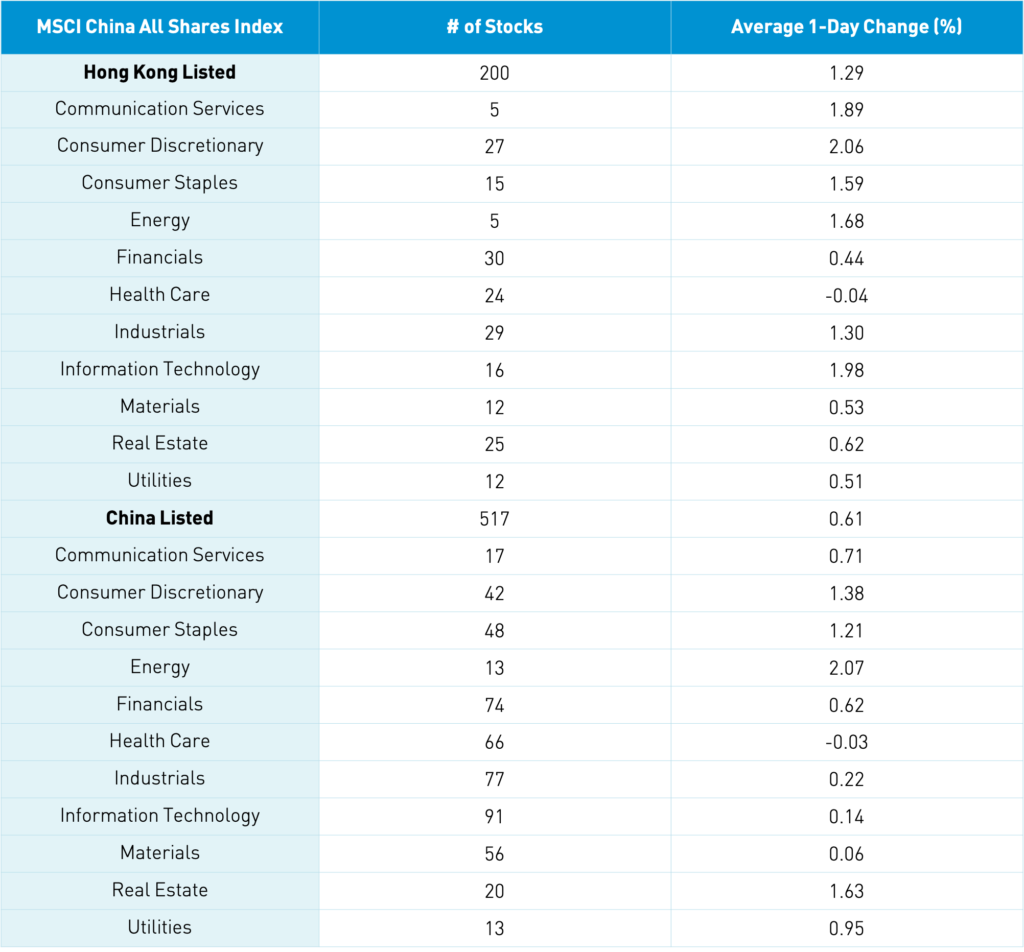

The Hang Seng was down in the morning as investors digested the economic release, leading to an afternoon rally to close +0.61% led by growth stocks. The index closed the week up by +0.94%. Volume increased +14.91% from yesterday, which is only 91% of the 1-year average. The Chinese companies listed in Hong Kong and within the MSCI China All Shares Index gained +1.29% led by discretionary +2.01%, tech +1.93%, communication +1.8%, energy +1.64%, and staples +1.54%. Health care was a laggard, falling -0.08%. Hong Kong’s most heavily traded stocks by value were Tencent, which gained +1.94%, Alibaba HK, which gained +0.77%, Meituan, which gained +1.9%, Geely Auto, which gained +7.13% after announcing its electric vehicle efforts, Xiaomi, which gained +1.96%, Ping An Insurance, which fell -0.61%, Xinyi Solar, which gained +3.61%, China Mobile, which gained +3.02%, HK Exchanges, which gained +0.78%, and energy giant CNOOC, which gained +3.06%. Southbound Stock Connect volumes were light as Mainland investors bought $648 million worth of Hong Kong stocks as Tencent was bought heavily and Southbound trading accounted for 10.6% of Hong Kong turnover.

A-Share Update

Shanghai, Shenzhen, and the STAR Board gained +0.81%, +0.62%, and +0.83%, respectively, leading to weekly returns of -0.7%, -0.73%, +0.26%. The Mainland stocks within the MSCI China All Shares Index gained +0.63% led by energy +2.09%, real estate +1.65%, discretionary +1.4%, staples +1.23%, and utilities +0.97%. Meanwhile, health care was off -0.01%. Semiconductors were off a touch on news that two US politicians want to limit semiconductor equipment sales to China though I am surprised Dutch semiconductor equipment manufacturer ASML is not up more than +0.4% as Chinese companies would simply drop US companies for them. Turnover today was up +4.7% from yesterday, which is only 78% of the 1-year average. Breadth was very strong with 3,315 advancers and only 697 decliners. The Mainland’s most heavily traded stocks by value were Kweichow Moutai, which gained +1.95%, BOE Tech, which fell -0.85%, alcohol stock Wuliangye Yibin, which gained +2.35%, Longi Green Energy, which fell -1.65%, and Huadong Medicine, which gained +4.38% on an analyst upgrade. Foreign investors bought $1.097 billion worth of Mainland stocks today as Northbound Stock Connect volumes were moderate/light as Northbound trading accounted for 6.5% of Mainland turnover. For the week, foreign investors bought $3.78 billion worth of Mainland stocks. Bonds gained a touch and copper had a strong day.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.52 versus 6.52 yesterday

- CNY/EUR 7.82 versus 7.80 yesterday

- Yield on 1-Day Government Bond 1.72% versus 1.58% yesterday

- Yield on 10-Year Government Bond 3.16% versus 3.17% yesterday

- Yield on 10-Year China Development Bank Bond 3.57% versus 3.57% yesterday

- China’s Copper Price +2.11% overnight