TAL Education Reports Strong Q4 Financial Results

3 Min. Read Time

Key News

Asian equities rebounded today on a very light news day. Today is President Biden’s global leader climate summit, during which the president will likely announce carbon-cutting goals. The US-China Joint Statement addressing the Climate Crisis following John Kerry’s visit to China last week shows an area of alignment. Reuters covered the National Energy Administration announcement that coal’s percentage in energy consumption would fall below 56% in 2021 from 56.8% in 2020 and 68% in 2010. Yesterday, it was announced that solar and wind’s percentage of power consumption would rise to 11% in 2021 from 9.7% in 2020. The goal is to get solar and wind up to 16.5% of power consumption by 2025 and non-fossil fuel power generation to 25% by 2030.

There is talk that the PBOC will take on assets from Huarong Asset Management. Regulators are pondering the best way to revive the embattled lender after the decision was made to bail it out.

US politicians are pushing a number of bills aimed at China, though I don’t see them having any real economic bite. The real beneficiary appears to be US tech companies, which will receive government subsidies for research & development. The cynic in me would point out the tech industry’s lobbying group applauding the move. According to one of the bills, US government officials will not attend the 2022 Beijing Olympics, though athletes will be allowed to compete.

Online education company TAL Education released Q4 earnings this morning. Revenues grew by 58% year-over-year driven by a strong increase in student enrollment. However, the costs to grow the business also increased, leading to a loss in net income in EPS. Investors are apt to give the company a pass as it is executing on the large opportunity of tutoring driven by China’s rigorous school exams. How you do on the kindergarten exam determines which primary school you attend. Afterward, your primary school exam determines which middle school, followed by high school exam culminating in the almighty “Gao Kao” college entrance examination. TAL is currently operating in 84 Chinese cities with 155 learning centers in Beijing alone, 100 in Shanghai, 81 in Guangzhou, 79 in Nanjing, 79 in Shenzhen, etc. China is big! I was very impressed by the company's very strong free cash flow as cash rose to $5.938 billion.

Percent change is year-over-year versus Q4 2020.

- Revenues +58.9% to $1.367B versus $857mm in Q4 2020 and analyst expectations of $1.201B

- Student enrollment increased 44% to 6,690,950 from 4,646,040 in Q4 2020

- Operating costs increased +84.8% to $1.662B from Q4 2020’s $899mm

- Selling and marketing expenses increased +171% to $660mm while general and administration expenses +57.6% to $348mm

- Loss from operations increased to $297mm from $41.3mm which was larger than anticipated

- Adjusted net loss was -$88mm versus Q4 2020’s loss of -$57.2mm and analyst expectations of a -$97mm loss

- Adjusted EPS loss was -$0.14 versus analyst expectations of -$0.16

- Cash doubled to $5.937B from $2.219B in Q4 2020

H-Share Update

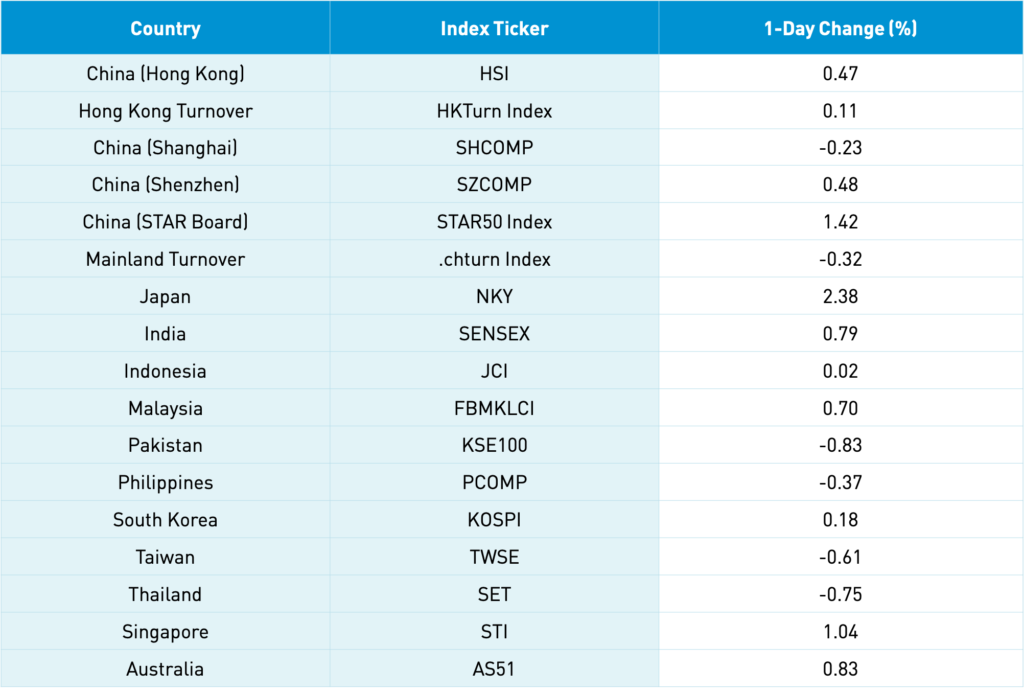

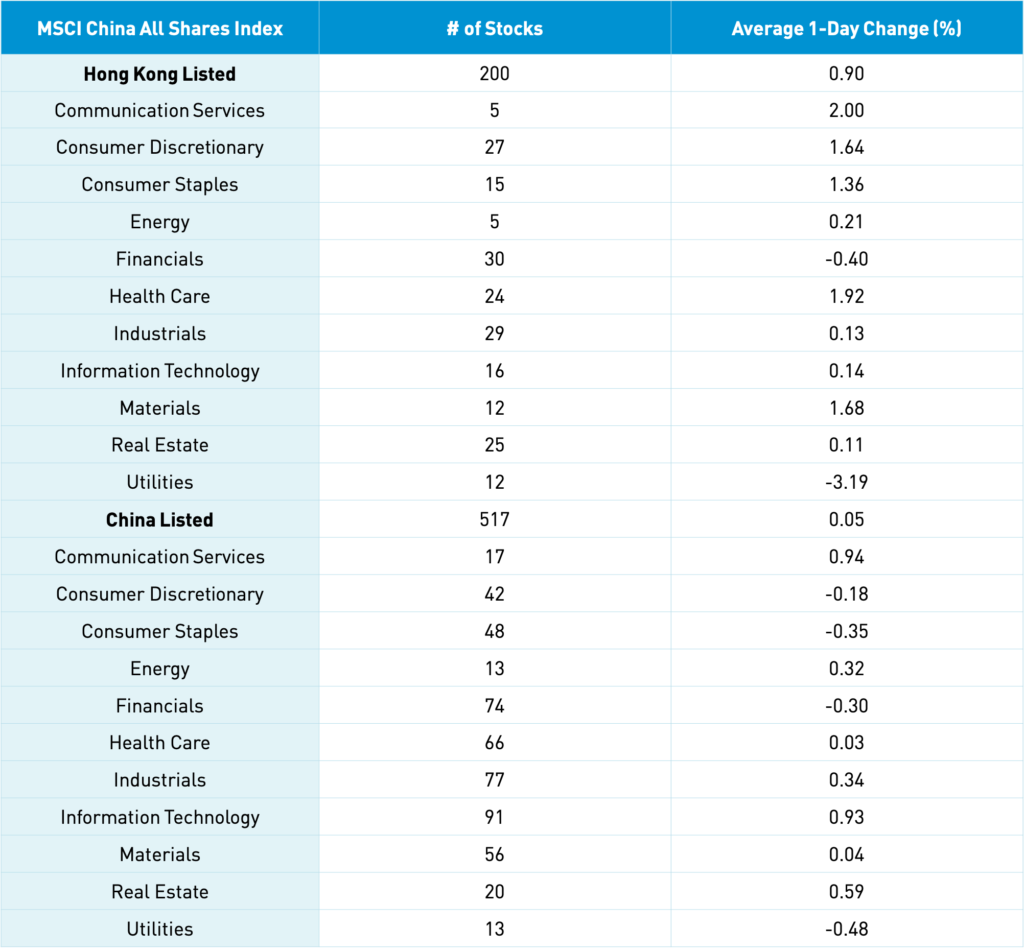

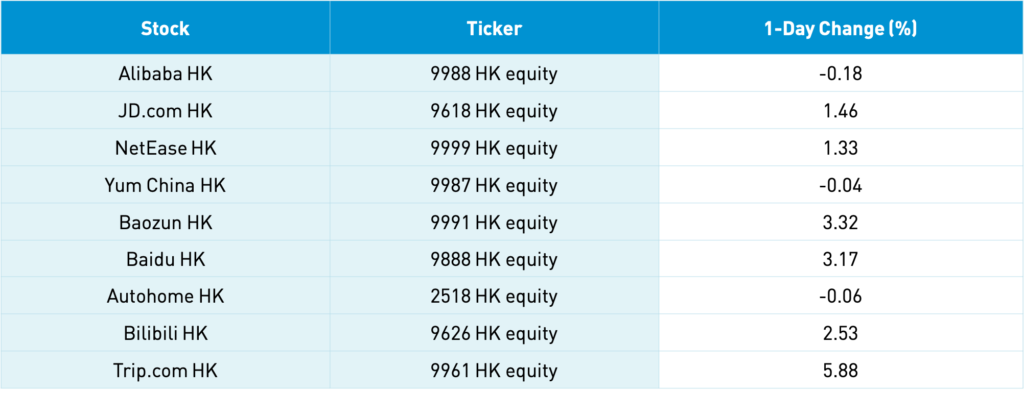

The Hang Seng gained +0.47% on volume flat day over day, which is just below the 1-year average. The Chinese companies listed in Hong Kong within the MSCI China All Shares Index gained +0.9%, led by communication +2%, healthcare +1.92%, materials +1.68%, discretionary +1.64%, and staples +1.36%, while utilities were off -3.19%. Hong Kong’s most heavily traded by value were Tencent, which rose +1.97%, Meituan, which gained +3.47%, Great Wall Motor, which fell -12.68% on an analyst downgrade, Ping An, which dropped -2.82% on earnings, Alibaba Hong Kong, which fell -0.18%, China Gas, which was off -11.32%, China Mobile, which gained +1.62%, Anta Sports, which rose +3.27%, Xiaomi, which was flat, and Geely Auto, which dropped -1.78%. Southbound Connect volumes were light (again) as Mainland investors bought a healthy $759mm of Hong Kong stocks as Southbound trading accounted for 10.0% of Hong Kong turnover. China Mobile and Anta saw outsized buying.

A-Share Update

Shanghai, Shenzhen, and STAR Board diverged -0.23%, +0.48%, and +1.42% respectively. Volumes were off a touch from yesterday, which is just 83% of the 1-year average while breadth saw 1,953 advancers and 1,813 decliners. The Mainland stocks within the MSCI China All Shares Index gained +0.05%, led by communication +0.92%, tech +0.1%, and real estate +0.57%, while utilities fell -0.5%, staples -0.37%, and financials -0.32%. Chemical, steel, and shipping companies had a strong day. The Mainland’s most heavily traded by value were GoerTek, which gained +10% post-earnings, Luxshare Precision, which rose +3.32%, Kweichow Moutai, which fell -1.18%, Longi Green Energy, which dropped -1.98% on earnings, BAIC BluePark New Energy, which was off -6.57%, broker East Money, which rose +1.94% on broker upgrade, GEM co, which was up +2.71%, Huadong Medicine, which gained +1.48% on earnings, BOE Tech, which rose +0.14%, and Ping An, which was up +0.2%. Northbound Stock Connect volumes were moderate as foreign investors sold -$246mm of Mainland stocks as Northbound trading accounted for 6.1% of Mainland turnover. CNY appreciated to 6.49 versus the US $ as bonds eased and copper gained.

Last Night's Exchange Rates, Prices, & Yields

- CNY/USD 6.49 versus 6.49 yesterday

- CNY/EUR 7.79 versus 7.81 yesterday

- Yield on 1-Day Government Bond 1.75% versus 1.70% yesterday

- Yield on 10-Year Government Bond 3.16% versus 3.15% yesterday

- Yield on 10-Year China Development Bank Bond 3.53% versus 3.52% yesterday

- China's Copper Price +0.38%