Mainland Mutual Funds Balance Value and Growth, Week in Review

4 Min. Read Time

Upcoming Webinar

Join us on Wednesday, April 28thth at 11:00 am EDT for our event:

A Quarter with Two Halves: Q1 China Internet Sector Update

Click here to register.

Week in Review

- Asian equities had a mixed start to the week. China outperformed Monday with automakers and electric vehicle companies leading the way as their products were on display at the Shanghai Auto Show.

- Meituan announced a private placement worth approximately $10 billion, including a $400 million investment from Tencent. The company’s shares were +1.52% higher in Tuesday trading.

- The head of the CSRC, China's SEC, recommended dialogue with US regulators on the issue of bringing US-listed Chinese companies into compliance with the Holding Foreign Companies Accountable Act in a statement Wednesday.

- TAL Education reported Thursday that revenues grew +58.9% year-over-year to $1.37 billion versus $857 million in Q4 2020 thanks to a strong increase in student enrollment.

Friday's Key News

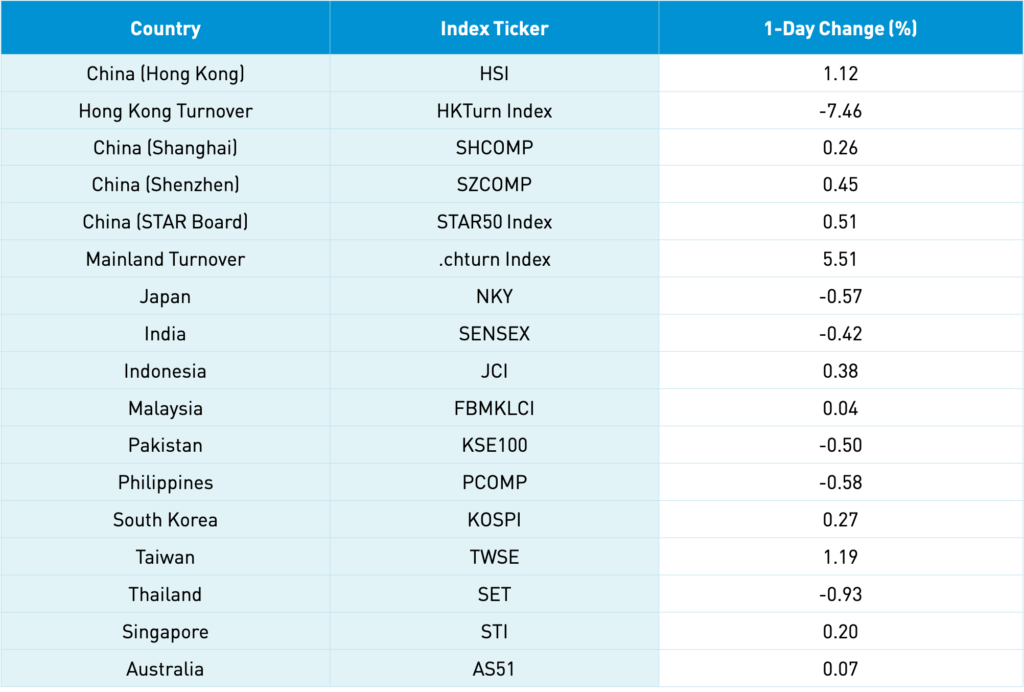

Asian equities were largely higher though Japan and India were off on rising coronavirus cases. Meanwhile, Hong Kong and Taiwan had strong days. President Biden’s global leader climate summit appeared to go well, providing a tailwind for clean technology plays such as wind, solar, and electric vehicles.

Mainland mutual fund managers’ positioning was a big topic overnight as they release their Q1 holdings. Industrial & Commercial Bank of China (ICBC) was the largest net purchase, followed by energy giant CNOOC and Agricultural Bank of China (ABC). The stock with the largest decrease was BOE Tech, followed by CGN Power, a nuclear energy company, Zijin Mining, and tech company Luxshare Precision. Q1 saw mainland managers balance their portfolios by adding value and subtracting growth. Their largest holdings are still Kweichow Moutai, Wiliangye Yibin, China Merchants Bank, Ping An Insurance, China Tourism Group, Midea Group, CATL, ICBC, Hikvision, and Gree. This is a global phenomenon that is not unique to the US.

The amount invested in stock funds increased 2.86% from Q4 2020 while that in bond funds increased 8.57% and money market funds +10.73%. Remember asset classes compete with one another so yields on bonds and money market funds compete with one another. The yield on Chinese government bond funds has increased from 2.6% to a peak of 3.36% in November 2020 to 3.17% today. Ant Group’s Yue Bao Money Market Fund’s yield has declined from 1.4% a year ago to 1.1% today. There was talk mainland PMs might be itching to get back into growth stocks now that their portfolios are more balanced between value and growth.

FTSE indexes moved to Alibaba’s Hong Kong listing from the US listing because the US listing is considered a foreign listing while the Hong Kong listing is considered a local listing. This has nothing to do with the PCAOB audit issue, but rather the value of volume traded of the Hong Kong share class versus the EM benchmark, not the US share class. One of their largest index client’s EM and non-US equity funds and ETFs no longer hold the US shares, but the Hong Kong shares as they converted. Conversion is easy. All a fund has to do is tell its custodian to convert and tomorrow it owns the Hong Kong shares. On May 11th, we will receive the Pro-forma for MSCI’s Semi-Annual Index Review. I believe it is highly likely that MSCI will announce the same transition. The 1-year average volume for Alibaba HK (9988 HK) is 29 million shares versus Alibaba US (BABA US), which is 19 million shares. The value traded of Alibaba HK is $912 million versus BABA US, which is $4.687 billion. JD.com HK listed in June 2020 so it likely will not see its transition until Q3, though its value of volume traded on Hong Kong is only $234 million versus the US share class’ $935 million over the last year.

A Mainland financial media source noted that 20 Chinese companies listed in the US in Q1 2021, raising $4.4 billion with the largest being e-cigarette company RLX Technology, which raised $1.6 billion. This is despite the passage and implementation of the Holding Foreign Companies Accountable Act, which requires US-listed Chinese companies to have their audit reviews verified by the PCAOB. Why are they listing in the US? The article states that the “likelihood of Chinese stocks already listed in the US facing delisting is extremely small.”

Cadillac announced the launch of the all-electric LYRIQ at the Shanghai auto show. If you haven’t seen the photos, it is a very cool-looking car!

H-Share Update

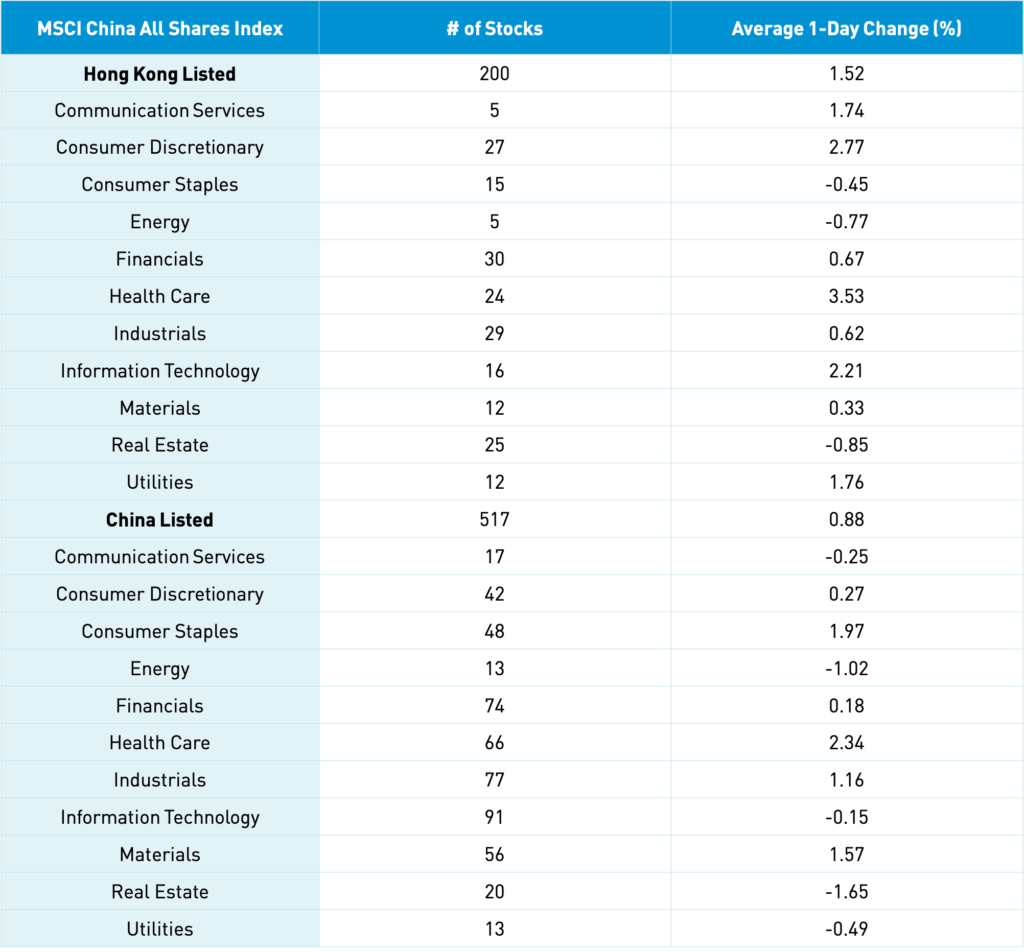

The Hang Seng jumped at the open and closed +1.12% at 29,078 as turnover increased 4%, which is 70% of the 1-year average. The 200 Chinese companies listed in Hong Kong gained +1.53% led by healthcare +3.54%, discretionary +2.78%, tech +2.22%, Utilities +1.77%, and communication +1.75%. Real estate, energy, and staples were off -0.83%, -0.76%, and -0.44%, respectively. Cleantech plays did well along with healthcare sub-sectors such tele-doctor, pharmaceuticals, and medical devices. Hong Kong’s most heavily traded stocks by value were Tencent, which gained +1.77%, Meituan, which gained +4.93%, Ping An Insurance, which gained +1.04%, Alibaba HK, which gained +1.36%, Xiaomi, which gained +2.27%, China Mobile, which fell -1.59%, Kuaishou tech, which gained +4.56%, Wuxi Biologics, which gained +4.36%, Sunny Optical, which gained +0.41%, and Anta Sports, which gained +4.36%. Southbound Connect volumes were light as Mainland investors bought $404 billion worth of Hong Kong stocks as Southbound trading accounted for 11.4% of Hong Kong turnover.

A-Share Update

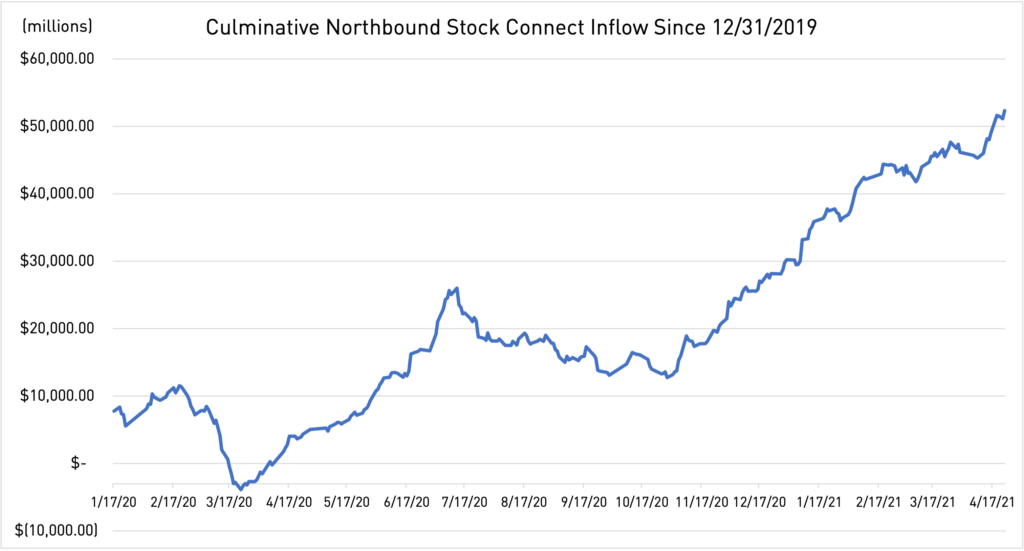

Shanghai, Shenzhen, and the STAR Board gained +0.26%, +0.45%, and +0.51%, respectively, as volumes were up +5.51%, which is 88% of the 1-year average. Breadth was off with 987 advancers and 2,914 decliners. The 517 Mainland stocks within the MSCI China All Shares Index gained +0.91% led by healthcare +2.38%, staples +2%, materials +1..61%, and industrials +1.16%. Meanwhile, real estate -1.625, energy -0.99%, and utilities -0.46%. Healthcare sub-sectors and cleantech plays did well. The Mainland’s most heavily traded stocks by value were broker East Money, which gained +3.54% on a broker upgrade, Kweichow Moutai, which gained +2.6%, GEM Co, which gained +10%, BOE Tech, which gained +2.25%, Ping An Insurance, which fell -0.15%, Wuliangye Yibin, which gained +3.25%, Aier Eye Hospital, which ripped +10.9%, Sany Heavy Industry, which gained +3.98%, GoerTek, which fell -2.18%, and Sungrow Power, which gained +6.53%. Northbound Stock Connect volumes were moderate as foreign investors bought $1.211 billion worth of Mainland stocks as Northbound Connect trading accounted for 6.4% of Mainland turnover. CNY appreciated versus the US dollar back to 6.49 while bonds were off and copper was up a touch.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.50 versus 6.49 yesterday

- CNY/EUR 7.83 versus 7.80 yesterday

- Yield on 1-Day Government Bond 1.65% versus 1.75% yesterday

- Yield on 10-Year Government Bond 3.17% versus 3.16% yesterday

- Yield on 10-Year China Development Bank Bond 3.55% versus 3.53% yesterday

- China's Copper Price +0.19% overnight