Meituan Rises in Hong Kong Trading as Lufax Earnings Beat Expectations

3 Min. Read Time

Upcoming Webinar

Join us tomorrow at 11:00 am EDT for our event:

A Quarter with Two Halves: Q1 China Internet Sector Update

Click here to register.

Key News

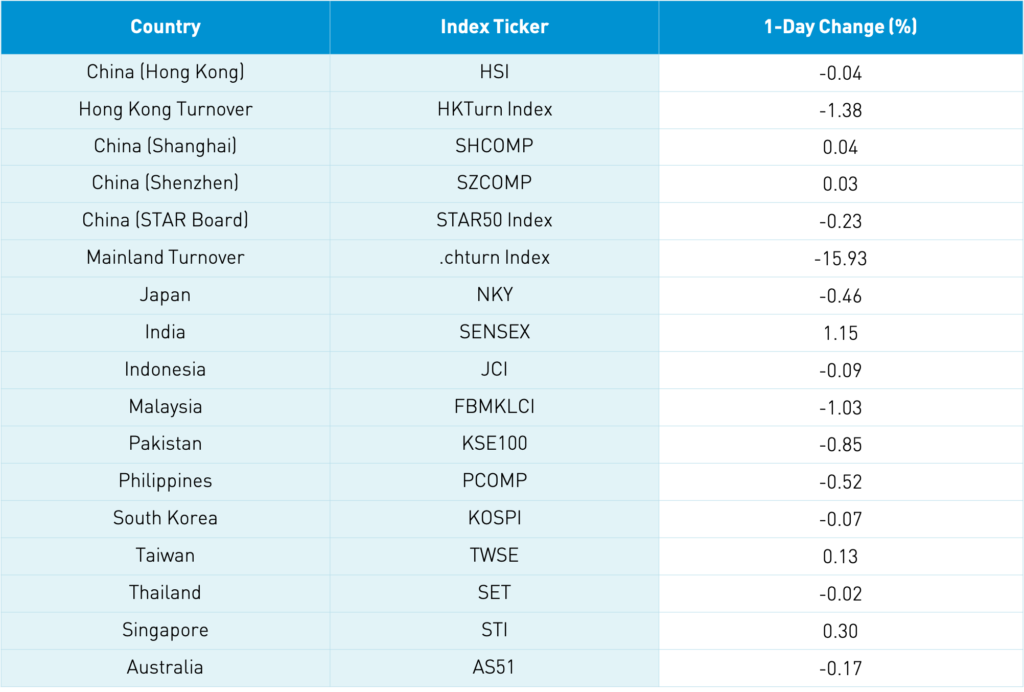

Asian equities were largely lower though India outperformed despite media coverage of rising coronavirus cases. Hong Kong had a volatile day and posted a small loss while China staged a late-day comeback to close somewhat higher.

Meituan’s anti-competitive investigation was announced after Hong Kong’s close yesterday, sending its US listing down -5.82%. How did the Hong Kong listing do today based on the same information? Up +2.62%. Similar to Alibaba, the investigation would put the issue to bed resulting in a fine. It’s amazing to see the disparity.

Wuxi Biologics announced after the Hong Kong close yesterday that its parent sold 108 million shares at a 6.8% discount to Monday’s closing price, sending the Hong Kong listing down -6.01%. It will be interesting to discover the buyer of the shares. Both Meituan and Wuxi were bought by Mainland investors via the Southbound Connect.

March Industrial Profits increased 92.3% year-over-year to RMB 711.2B. The release was not cited as a market-moving event, since investors will focus on companies’ earnings season.

Fintech company Lufax Holdings reported Q1 financial results after the US market close yesterday. Management did a great job keeping costs relatively under control, allowing the company to increase profitability. This is despite its core retail credit facilitation service fees and wealth management transaction and service fees declining -7.1% and -9.4% respectively. “Other income” increased by +241%, offsetting the above weakness and driven by an “increase in account management fees, collections, and other value-added service fees”. The company addressed increased regulation on their conference call. I like how management addressed it right up front in the call stating “our business was not materially affected, thanks to our pre-emptive regulatory intentions and proactive adjustments. These efforts have also enabled us to achieve solid operating results in the first quarter.” Well said!

- Revenue increased +16.9% to $2.328B (RMB 15.251B) from RMB 13.046B versus analyst expectations of RMB 14.573B

- Expenses increased 17.1% to $1.302B (RMB 8.53B)

- Net Margin 32.6%, which is an increase of 1.6%

- Net Profit increased 18.7% to $758mm (RMB 4.969B)

- Adjusted EPS RMB 2.27 versus analyst expectations of RMB 1.72

H-Share Update

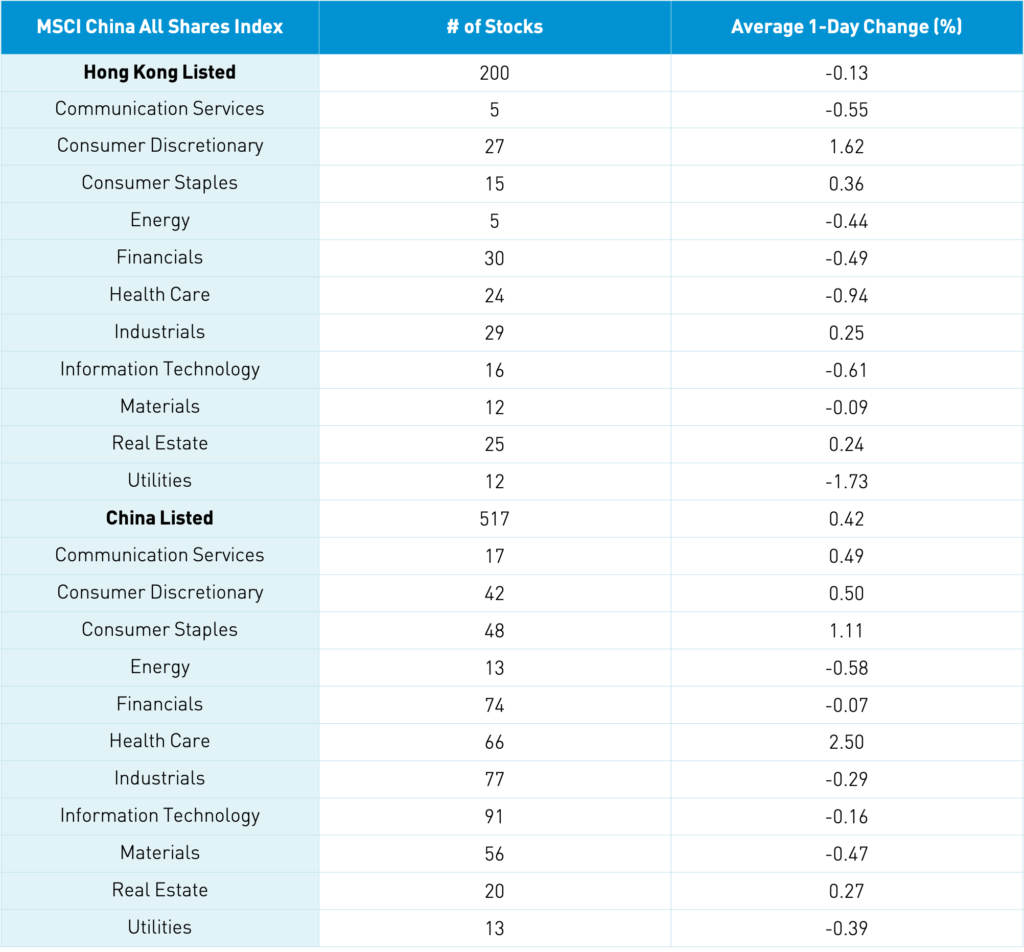

The Hang Seng bounced around the room closing -0.04% as volume fell -1.4%, which is back below the 1-year average. The 200 Chinese companies listed in Hong Kong within the MSCI China All Shares Index were off -0.14%, as discretionary rose +1.62% and staples +0.36% while utilities fell -1.73%, healthcare -0.94%, tech -0.61%, and communication -0.55%. Biotech and tele-doctor sub-sectors did well along with air pollution while nuclear power generation, energy generation, and cement were off. Hong Kong’s most heavily traded by value were Meituan, which rose +2.62%, Tencent, which fell -0.56%, Wuxi Biologics, which was off -6.01%, Ping An, which dropped -0.93%, Alibaba Hong Kong, which gained +0.8%, Xiaomi, which fell -0.38%, Hong Kong Exchanges, which dropped -0.28%, HSBC, which rose +2% post-earnings release, China Construction Bank, which fell -0.94%, and AIA, which gained +0.56%. Southbound Connect volumes were light as Mainland investors bought $107mm of Hong Kong stocks as Southbound trading accounted for 10.7% of Hong Kong turnover.

A-Share Update

Shanghai, Shenzhen, and STAR Board were mixed at +0.04%, +0.03%, and -0.23% respectively, overcoming morning losses. Volumes were off by -15.93%, which is only 86% of the 1-year average while breadth saw 1,296 advancers and 2,606 decliners. The Chinese companies listed in the Mainland within the MSCI China All Shares Index gained +0.42%, led by healthcare +2.49%, staples +1.1%, and discretionary +0.49%, while energy fell -0.59%, materials -0.48%, and utilities -0.4%. Healthcare sub-sectors outperformed along with paper companies, shipping, and alcohol sub-sectors while airlines, auto, and communication sub-sectors were off. The Mainland’s most heavily traded by value were broker East Money, which fell -2.61% on a broker downgrade after three executives quit, BOE Tech, which gained +1.66%, Zijin Mining, which rose +1.26%, Ping An, which was up +0.52%, GEM Co, which fell -2.77%, CATL, which was off -0.11%, COSCO Shipping, which gained +7.75%, Luxshare Precision, which rose +5.7%, Kweichow Moutai, which was up +0.8%, and Chongqing Sokon, which rose +3.5% on its involvement in with Huawei’s EV efforts. Northbound Connect volumes were moderate as foreign investors bought $541mm of Mainland stocks as Northbound trading accounted for 5.1% of Mainland turnover.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.48 versus 6.49 yesterday

- CNY/EUR 7.83 versus 7.84 yesterday

- Yield on 10-Year Government Bond 3.21% versus 3.20% yesterday

- Yield on 10-Year China Development Bank Bond 3.59% versus 3.58% yesterday

- China’s Copper Price +2.27% overnight