Asian Equities Rejoice Over Powell’s Comments, Tencent’s Fine is a Rounding Error

3 Min. Read Time

Upcoming Webinar

On Friday, April 30th, Nobel-Laureate Economist Robert Engle will be co-hosting:

A Financial Risk Framework For Climate Change: Portfolio Construction, Stress Testing, and Risk Transfer

Click here to register.

Key News

Asian investors embraced Jerome Powell’s dovish comments sending equities higher, though South Korea was an outlier to the downside. Copper rose +0.92% on the comments in Mainland futures trading while energy and materials had strong days.

Reuters reported after the close that Tencent will be hit with an anti-competitive fine of RMB 10 billion versus Alibaba’s RMB 18 billion fine. The company had $23 billion of cash on the books at year-end as part of $49 billion of current assets. Tencent is well connected politically so this should amount to a yawn, though I’m sure the nattering nabobs of negativity will be out in force.

Today was a big Hong Kong Q1 earnings day as BYD revenue grew +108% year-over-year (YoY) while net income doubled, though the stock was off. China Construction Bank grew net income by +2.8% YoY, showing why investors have avoided the companies. Hong Kong Exchanges revenues grew +49% and net income grew +70% YoY as the company benefits from the relisting of US Chinese companies. I half-joking call the US regulation of US-listed Chinese companies the Hong Kong investment banker employment act.

Separately, I received a research piece stating that the size of the Chinese asset management assets under management nearly doubled comparing Q1 2021 to Q1 2020 to RMB 7.7 trillion. A Mainland broker noted that several stocks jumped today as prestigious private equity firm Hillhouse disclosed ownership stakes.

According to the Financial Times, US accounting firms find themselves in a tough situation as the US increases regulatory efforts towards US-listed Chinese companies. The article solely focused on the risks and few bad apples while failing to speak at all to the rewards or gains investors have reaped in the companies. Coincidentally, I had a conversation yesterday with an executive of a financial firm heavily involved in Chinese investment banking and trading. His opinion was that Big Firm accounting firms will find a solution as there is simply much money at stake for them.

Our friend Garry asked a question on our webinar yesterday about China’s digital currency as a threat to mobile payment platforms. We believe digital currency is not a threat to mobile payment platforms, which offer a host of other services. Furthermore, the central bank is also likely to lean on these platforms to encourage user adoption. Overnight a Mainland financial outlet announced, “The People’s Bank of China (PBOC) Digital Currency Research Institute has executed a strategic cooperative agreement with Ant Group”. The article noted this is despite Ant’s pulled IPO and restructuring to comply with recent fintech rules.

H-Share Update

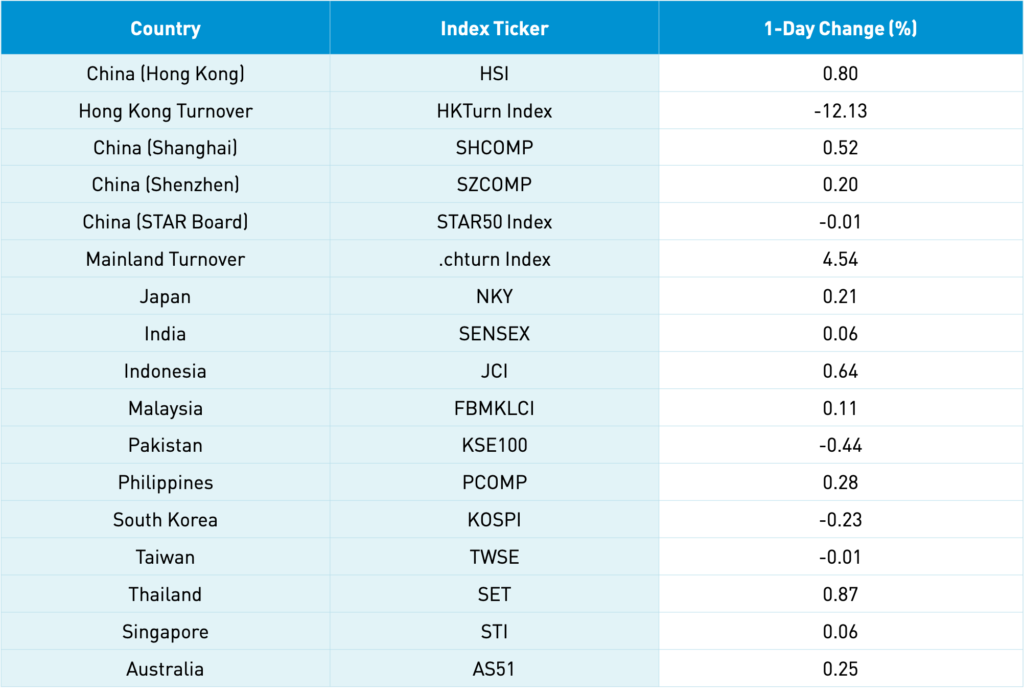

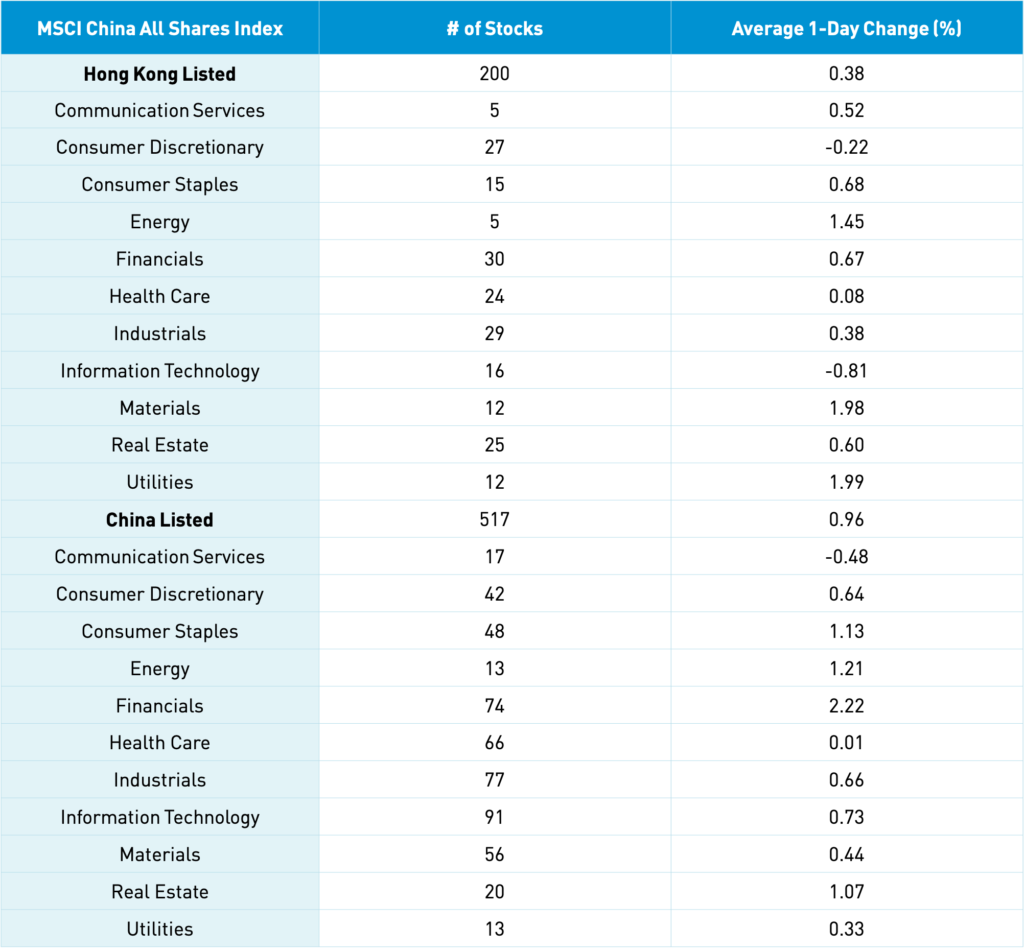

The Hang Seng gained +0.8% as volume declined -12% from yesterday to 75% of the 1-year average. The 200 Chinese companies listed in Hong Kong within the MSCI China All Shares Index gained +0.38%, led by utilities +1.99%, materials +1.98%, and energy +1.44%, while tech fell -0.81% and discretionary -0.23%. Metals, mining, and rare earth stocks had a strong day. Hong Kong’s most heavily traded by value were Tencent, which gained +0.56%, Meituan, which fell -0.06%, AIA, which gained +3.71%, Alibaba Hong Kong, which fell -0.09%, Ping An, which rose +1%, BYD, which dropped -3.21%, Hong Kong Exchanges, which fell -1.8%, HSBC, which rose +1.79%, Xiaomi, which fell -0.59%, and BYD Electronic, which fell -12.04% on an earnings miss. Southbound Connect was closed today as China will close Monday through Wednesday for Labor Day. Volumes are going to be low next week.

A-Share Update

Shanghai, Shenzhen, and STAR Board diverged at +0.52%, +0.2%, and -0.01% respectively on volumes which gained +4.54% from yesterday, which is only 93% of the 1-year average. The 517 Mainland stocks within the MSCI China All Shares Index gained +0.94%, led by financials +2.2%, energy +1.2%, staples +1.12%, and real estate +1.06%, while communication fell -0.5% and healthcare was flat. The Mainland’s most heavily traded by value were Kweichow Moutai, which fell -0.77%, broker East Money, which gained +0.76%, EV battery maker CATL, which rose +3.53%, Tianqi Lithium, which rose +8.6%, Inner Mongolia Yili, which gained +7.21% on net income doubling, liquor stock Wuliangye Yibin, which was up +1.37%, COSCO Shipping, which gained +6.49% on very strong earnings, Ganfeng Lithium, which was up +3.98%, Fosun Pharma, which rose +2.26%, and Gree Electric Appliances, which gained +2.5%. Northbound Stock Connect volumes were moderate as foreign investors bought $786mm of Mainland stocks as Northbound Connect trading accounted for 6.6% of Mainland turnover. Bonds rallied, CNY appreciated to 6.47 versus the US $, and copper rose +0.92%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.47 versus 6.48 yesterday

- CNY/EUR 7.85 versus 7.83 yesterday

- Yield on 10-Year Government Bond 3.19% versus 3.20% yesterday

- Yield on 10-Year China Development Bank Bond 3.57% versus 3.57% yesterday

- China’s Copper Price +0.92% overnight