Fintech Platforms Meet With Regulators, Week in Review

4 Min. Read Time

Week in Review

- Asian equities had a mixed start to the week Monday as the market digested news that Meituan would become the next target for regulatory action arising from China’s new, internet platform-focused anti-monopoly law. However, the company has $2.6 million in cash on its balance sheet to cover any fines.

- Fintech company Lufax Holding reported Q1 financial results after the US market close Monday. The company increased revenue by +16.9% to RMB 15.251 billion versus analyst expectations of RMB 14.573 billion. We noted in our Q4 report that Lufax is a standout among fintech platforms for having successfully navigated the current regulatory environment in China.

- Q1 earnings releases continued this week for companies listed in both China and the US. Among the notable releases were search engine and cloud computing giant Baidu, battery maker CATL, and liquor giant Kweichow Moutai. The companies grew revenue by 108%, 10%, and 11%, respectively, year-over-year in Q1.

- Asian investors cheered Fed Chair Powell’s dovish commentary from the day before in Thursday trading. Meanwhile, Tencent was hit with a $1.5 billion fine from regulators, which was significantly less than Alibaba’s $2.7 billion fine and a rounding error considering the size of the company’s balance sheet.

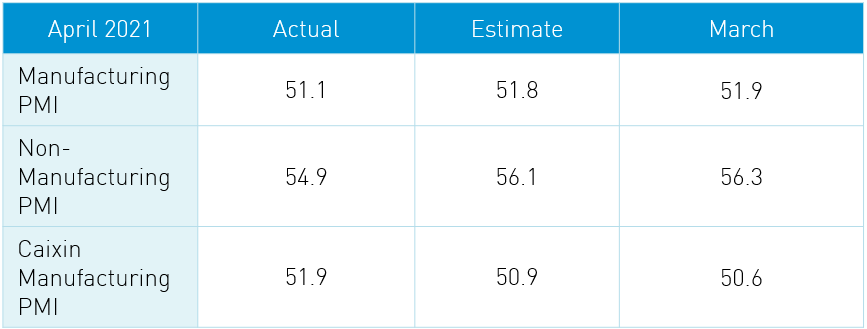

April PMI Release

Takeaway: The “official” PMI, released by the National Bureau of Statistics, came in a touch light, indicating the pace of growth is slowing. The “private” PMI survey conducted by IHS Markit and released by media company Caixin, exceeded expectations. Why the disparity? The “official” PMI is a large survey of big companies while the “private” PMI is a smaller survey and focuses on small and medium-sized companies making it more volatile. Remember that PMIs are diffusion indexes, meaning that readings above 50 indicate growth while readings below 50 indicate contraction. PMIs are a month-to-month comparison, not year-over-year. Therefore, the pace of growth is slowing, which is not all that surprising. Inventories of raw materials continue to contract, which could be a good sign for commodity prices. Input and output prices continue to increase, albeit at a slower pace. The Fed might be indifferent to inflation, but it’s out there. Both the official and Caixin surveys saw strong business activity expectations despite new export orders falling to 50.4 from March’s 51.2. The release was good, but not great, which likely contributed to an off day in the equity market. At the same time, it might give policymakers some pause on scaling back supportive economic policies.

Friday’s Key News

Asian equities ended April with a thud as India, the Philippines and Hong Kong underperformed regionally. Taiwan was closed today while Hong Kong and Mainland China will be closed Monday. China will be closed until Thursday. One element of today’s market action was simply investors taking chips off the table pre-holiday.

Internet names were the talk of the town as the PBOC met with thirteen companies about implementing controls on their fintech business lines, like what we saw with Ant Group. These requirements include not lending to college students, the companies holding at least 30% of loans on their books, and the most they can lend is RMB 200,000. Furthermore, the financial arms of the companies need to financial holding companies so that they can be regulated like a bank. This would satisfy the PBOC’s desire for more transparency in their operations from a monitoring perspective. This makes sense to me as stability is job #1 for the central bank if job #2 is preventing a crisis from occurring (stopping the first domino).

US-listed Chinese equities were weak yesterday and this news was likely a factor. On their earnings conference call earlier this week, the CEO of Lufax mentioned he would be visiting Beijing to meet with regulators. During the call, he reiterated that the company was complying with regulations. One of our favorite Mainland research firms was fairly dismissive of the news, believing compliance is easily attainable. Three Chinese policy banks reported a delay in their 2020 financial results, which is likely nothing, but could have weighed on sentiment toward financials. The policy banks are not publicly listed, but their bonds are heavily owned. Bonds rallied today, including bonds issued by these policy banks in an indication that there is no need for alarm.

H-Share Update

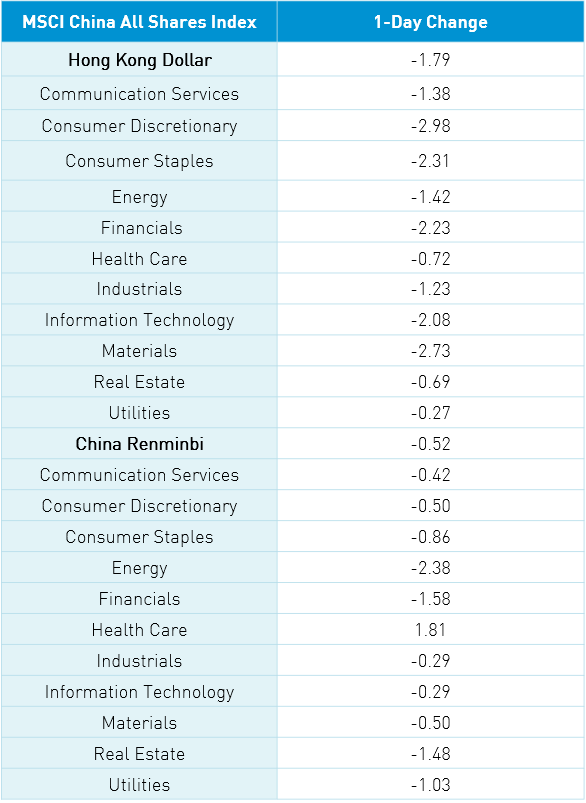

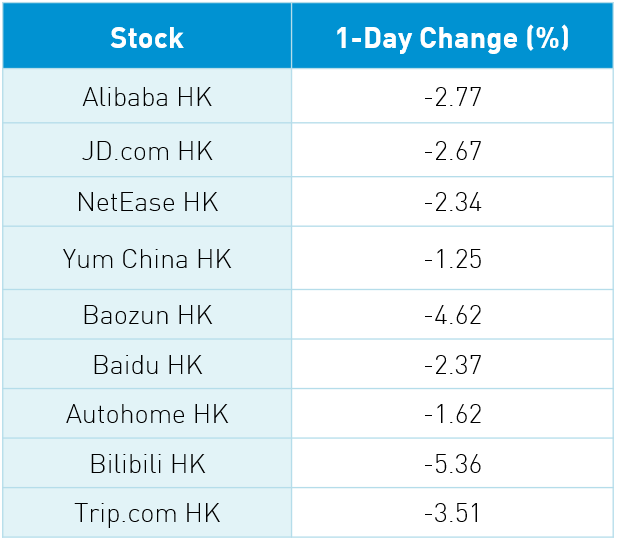

The Hang Seng grinded lower to close -1.97% on volume that was up +5% from yesterday, which is only 79% of the 1-year average. The Chinese companies listed in Hong Kong and within the MSCI China All Shares Index were off -1.8% with discretionary -2.99%, materials -2.73%, staples -2.32%, financials -2.24%, and -2.09%. In addition to internet names’ weakness, electric vehicle and auto names were off along with metals and mining. Hong Kong’s most heavily traded stocks by value were Tencent, which fell -1.35%, Meituan, which fell -3.62%, Alibaba HK, which fell -2.77%, Ping An, which fell -1.51%, ICBC Bank, which fell -3.62%, China Construction Bank, which fell -3.45%, AIA, which fell -4.44%, HSBC, which gained +1.14%, Hong Kong Exchanges, which fell -2.08%, and BYD, which fell -5.04%. Southbound Stock Connect trading was closed today.

A-Share Update

Shanghai, Shenzhen, and the STAR Board were off -0.81%, -0.29%, and -0.14%, respectively, as volume increased +5.61% from yesterday, which is just below the 1-year average. There were 1,227 advancing stocks and 2,645 declining stocks. The Mainland stocks within the MSCI China All Shares Index were off -0.51% with healthcare the only positive sector, gaining +1.82%. Meanwhile, energy -2.37%, financials -1.57%, real estate -1.47% and utilities -1.02%. The Mainland’s most heavily traded stocks by value were battery maker CATL, which gained +2.15%, Longi Green Energy, which gained +5.63%, Kwiechow Moutai, which fell -0.97%, BOE Tech, which gained +0.96%, Fosun Pharma, which gained +10.01%, Ganfeng Lithium, which gained +6.22%, Huadong Medicine, which gained +10.01%, Tianqi Lithium, which gained +2.18%, Walvax Biotech, which gained +6.35%, and BYD, which fell -2.69%. Northbound Stock Connect volumes were moderate/high as foreign investors sold -$239 million worth of Mainland stocks as Northbound Stock Connect trading accounted for 7.4% of Mainland turnover. CNY was steady at 6.47 while bonds rallied and copper eased -0.44%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.47 versus 6.47 yesterday

- CNY/EUR 7.79 versus 7.84 yesterday

- Yield on 1-Day Government Bond 1.63% versus 1.55% yesterday

- Yield on 10-Year Government Bond 3.16% versus 3.19% yesterday

- Yield on 10-Year China Development Bank Bond 3.54% versus 3.57% yesterday

- China’s Copper Price -0.44%