China’s Exports Rise Amid Global Recovery, Week in Review

3 Min. Read Time

Upcoming Event

Join us on Tuesday, May 25th at 8:20 am for our virtual mid-year conference:

Innovation: The Next Phase of China’s Secular Growth

Featuring the CFO of NIO Steven Feng and Former US Ambassador to China Max Baucus.

Click here to register.

Week in Review

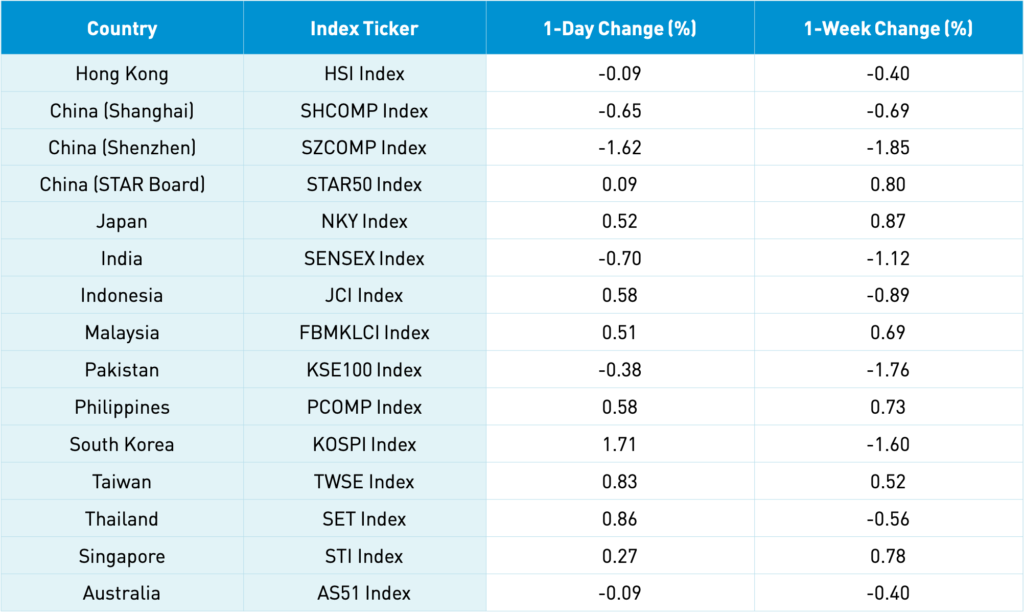

- Mainland China markets were closed Monday through Wednesday this week for the Labor Day holiday. Hong Kong remained open as the Hang Send gained +0.96% from Monday to Thursday amid a volatile week for global equities. As Mainland China was on holiday, markets digested Treasury Secretary Yellen’s mention of the possibility of raising rates and an unfortunate virus situation in India.

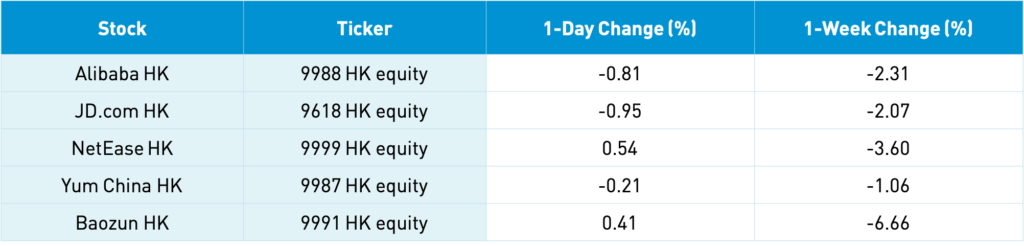

- Alibaba-backed cloud computing firm Qiniu, the latest Chinese company to decide to list in the US despite the Holding Foreign Companies Accountable Act (HFCA), filed for a Nasdaq IPO on Monday.

- Domestic travel in China was strong during this year’s Labor Day holiday. Chinese tourists took 230 million trips this year, up 103% from 2019 (pre-pandemic) levels. CICC forecasts domestic tourism revenue for this year’s holiday will be RMB 113 billion ($17.4 billion)

- Chinese vaccine makers came under pressure in Thursday trading following the US’ expressed support for patent waivers for covid-19 vaccines worldwide, meaning that Chinese vaccines may become less competitive abroad.

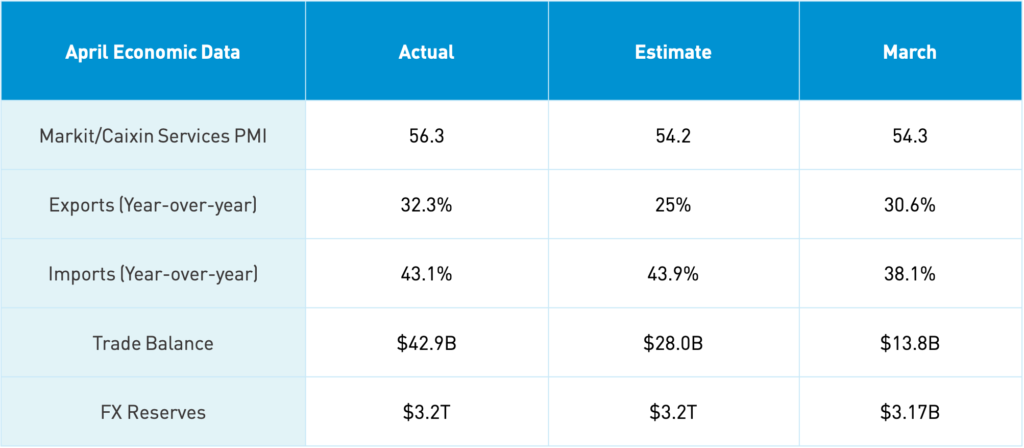

Economic/Trade Data Release Overview

Takeaway: While the services PMI was somewhat of a surprise to the downside, China’s services economy nonetheless expanded in April. PMIs are diffusion indexes, meaning that any reading above 50 indicates an expansion and any reading below 50 indicates a contraction. Meanwhile, exports blew estimates out of the water as China continues to fulfill the increasing demands of a recovering global economy. The surge in China’s exports is even more impressive considering its wide gulf with imports, indicated by the trade balance.

Friday’s Key News

Asian equities were mostly higher Friday, though an outlier to the downside was Mainland China, where markets have had limited time to absorb negative macro headlines due to this week's holiday. Commodities and banks were the positive stories of the week and continued into Friday. There was little else to be upbeat about in global markets this week as growth stocks came under pressure. Copper prices globally gained over +5% this week and crude oil, represented by the OIL ETF, gained +2%. Meanwhile, bank stocks in the US and China rose in anticipation of rising interest rates. However, the Nasdaq appears to be popping back up today.

CNY will likely not be on such a tear this year as it was in 2020 when the currency gained over 5% against the US dollar. The end of covid-19 supply constraints in other countries may hurt China’s terms of trade somewhat. Nonetheless, the currency has held steady in 2021 so far and net appreciation versus the USD in 2021 remains likely.

In 2019, Australia imported $2.2 billion worth of goods from China and exported $2.4 billion. The trade tussle is silly given the countries’ proximity to and reliance on one another.

China REITs are rising in popularity as more household savings are put into financial assets. REITs are an excellent way to mix real estate and equity investment. In the US, real estate assets account for over 30% of household savings, whereas in China they account for nearly 60%. CICC analysts believe that real estate as a percentage of household assets has peaked in China, which may mean a significant increase in equity market participation among Chinese savers. This could lead to massive inflows of new capital and a long-term tailwind for Mainland China equities.

China will take its turn chairing a UN Security Council Event today. Secretary of State Blinken will reinforce his administration’s commitment to reaffirming the US’ role on the world stage through multilateralism and international bodies such as the UN. Wang Yi, China’s foreign minister, will express his views on strengthening the global community as well. Though both statesmen will express their disagreements too, it is nice to see dialogue occurring.

H-Share Update

The Hang Seng opened higher and ended up mostly unchanged overnight, closing down slightly by -0.09% at 28,610. Volume was higher than yesterday and the average for the week as Southbound Stock Connect was closed Monday through Wednesday. The most heavily traded stocks in Hong Kong were Bank of China, which gained +0.03%, ICBC, which gained +0.05%, PetroChina, which gained +0.05%, China Construction Bank, which gained +0.09%, CNOOC, which gained +0.08%, China Petroleum & Chemical Co., which gained +0.04%, Xiaomi, which fell -0.25%, Geely Automotive, which fell -0.54%, and Sino Biopharma, which gained +0.05%.

A-Share Update

Shanghai, Shenzhen, and the STAR board diverged closing at -0.65%, -1.62%, and +0.09%, respectively. The most heavily traded stocks by foreign investors via Northbound Stock Connect were Kweichow Moutai, which fell -2.86%, Ping An Insurance, which fell -0.61%, China Merchants Bank, which gained +0.95%, COSCO Shipping, which gained +1.84%, Contemporary Amperex Technology, which fell -4.35%, BOE Tech, which fell -5.71%, and Midea, which fell -3.20%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.44 versus 6.46 yesterday

- CNY/EUR 7.81 versus 7.91 yesterday

- Yield on 1-Day Government Bond 1.39% versus 1.48% yesterday

- Yield on 10-Year Government Bond 3.16% versus 3.15% yesterday

- Yield on 10-Year China Development Bank Bond 3.54% versus 3.52% yesterday

- China’s Copper Price +0.12% overnight