Growth Sentiment Mixed Following Internet Earnings, Week in Review

4 Min. Read Time

Week in Review

- Growth stocks rebounded on Monday against the backdrop of an economic release that saw both retail sales and industrial production miss sky-high estimates. Investors saw this as reason enough that stimulus will not be removed hastily.

- Earnings season for US and Hong Kong-listed internet companies continued this week. Baidu, Baozun, NetEase, iQiyi, Tencent, Tencent Music, JD.com, KE Holdings, Trip.com, and Vipshop all reported Q1 financial results this week. Most releases beat or met analyst expectations except for Trip.com, which suffered from a lingering lack of travel in Q1.

- Shares outstanding in one Mainland-listed China internet ETF have doubled since the mid-February correction. It makes one wonder what their investors know.

- The second half of Q1 2021 saw everything but the kitchen sink thrown at Chinese internet companies. Fortunately, as their earnings prove, many of these companies are still offering growth rates that are hard to find.

Key News

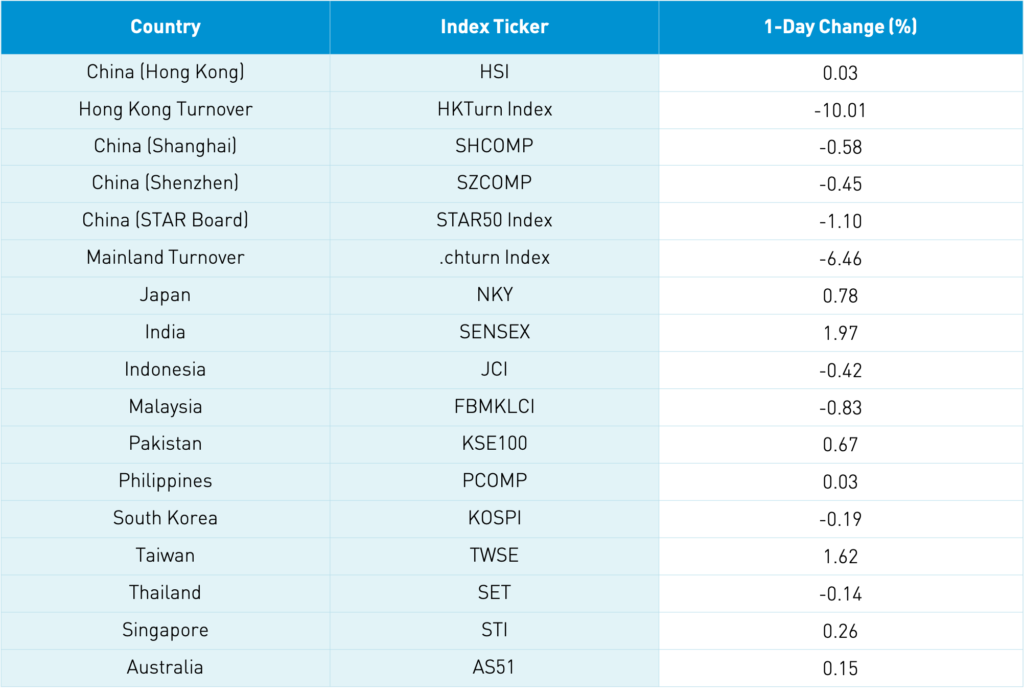

Asian equities ended a positive week on a mixed note with little significant news overnight. India ripped nearly +2% while Southeast Asia and China were off as the latter was hit on profit-taking as value outperformed growth. Shanghai dipped below the 3,500 level while Shenzen is sitting above the 2,300 level.

Tencent was off overnight despite good Q1 results yesterday. The media keeps hammering their investment plans along with other internet firms, claiming that their plans are too ambitious. Overlooked is the fact that Tencent’s Fintech unit saw revenue increase +47% year-over-year as the company adheres to new lending rules, which, evidently, are not the end of the world for the company’s fintech and payments business. I do not see Tencent’s dip today as being more than temporary. Furthermore, there is an element of seasonality in Tencent’s quarterly results. Q1 is always the company’s weakest quarter and results tend to strengthen throughout the year. Another factor in Tencent’s performance was the announcement from Hang Seng Indexes that the Hang Seng Index will increase from 55 to 58 holdings. Xinyi Solar, BYD, and Country Garden Services will be added. While we did not know the number of additions prior to the announcement, we did know those top holdings would see their max weight reduced from 10% to 8% going forward. As the top holding, Tencent will see net outflow, which likely weighed on the stock. The change will be implemented at the close on Friday, June 4th.

Hong Kong-listed internet stocks shrugged off news from the Cyberspace Administration that several apps need to change their data gathering within 15 days.

China’s regulators are concerned about rising commodities prices. Reuters, Bloomberg, and our friend Brian noted that the PBOC’s Shanghai head of research wrote that a strengthening yuan would negate rising commodity prices. While this is true, it would make exports more expensive. Tightening commodity margin requirements is another option to lower prices, though it is hard to overcome the forces of supply and demand.

Chang An Auto, Huawei, and CATL are entering a partnership to build “an intelligent connected electric vehicle platform” which investors liked overnight.

Chinese financial media were buzzing about CICC’s equity strategy report recommending investors return to growth sectors following the recent rebalancing. The report came at the perfect time because we have CICC’s Beijing-based equity strategist Kevin Liu speaking next Tuesday morning at our Mid Year conference. My colleague Fernando noted a similar recommendation from hedge fund manager Gavin Baker of Atreides Management, who runs an excellent blog. Fairlead Strategies’ Katie Stockton, a great technical analyst who will also be speaking Tuesday at our conference, is also quite constructive after this recent correction in China internet stocks as the long-term trend is still in place in her opinion.

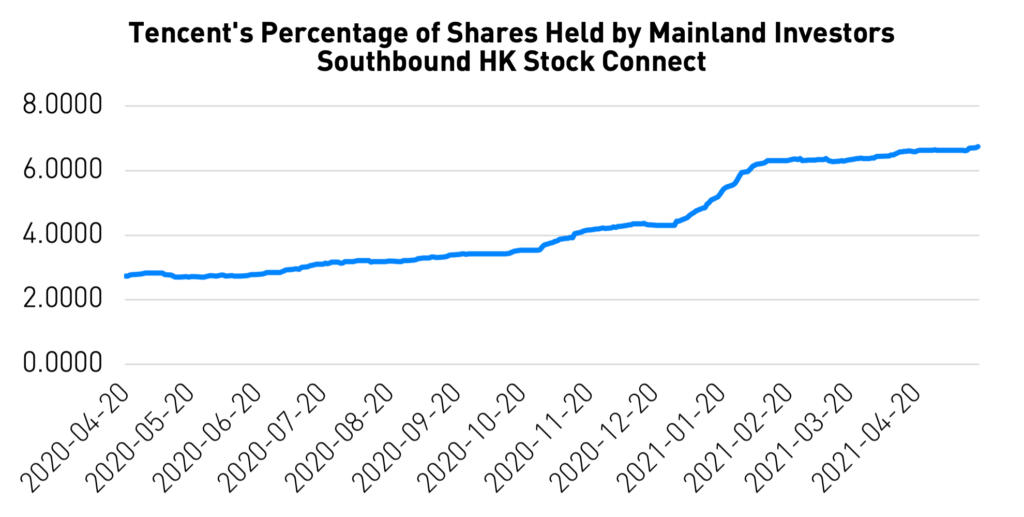

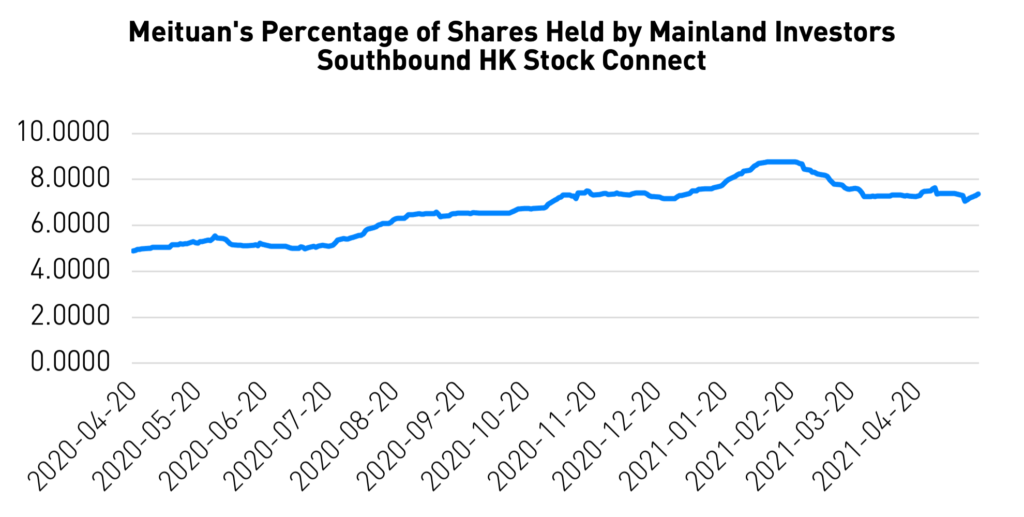

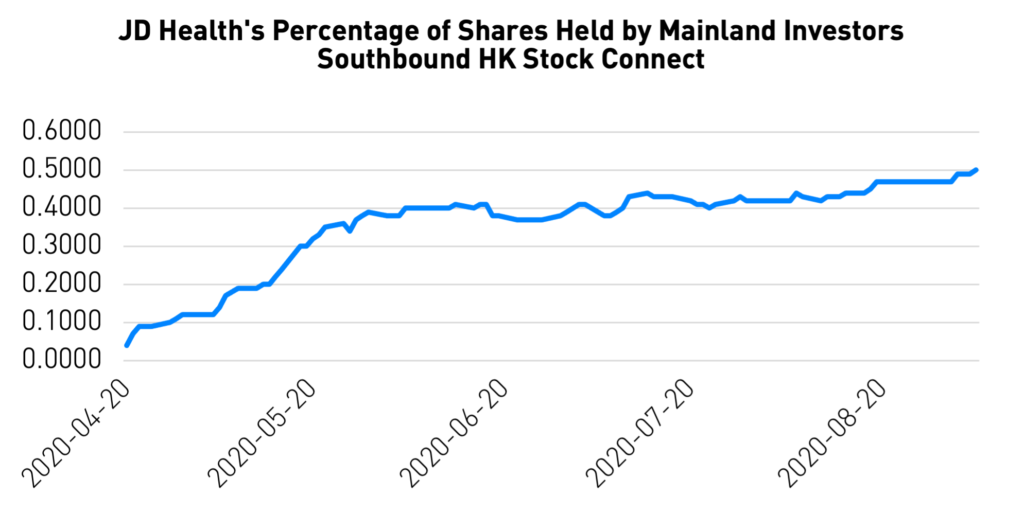

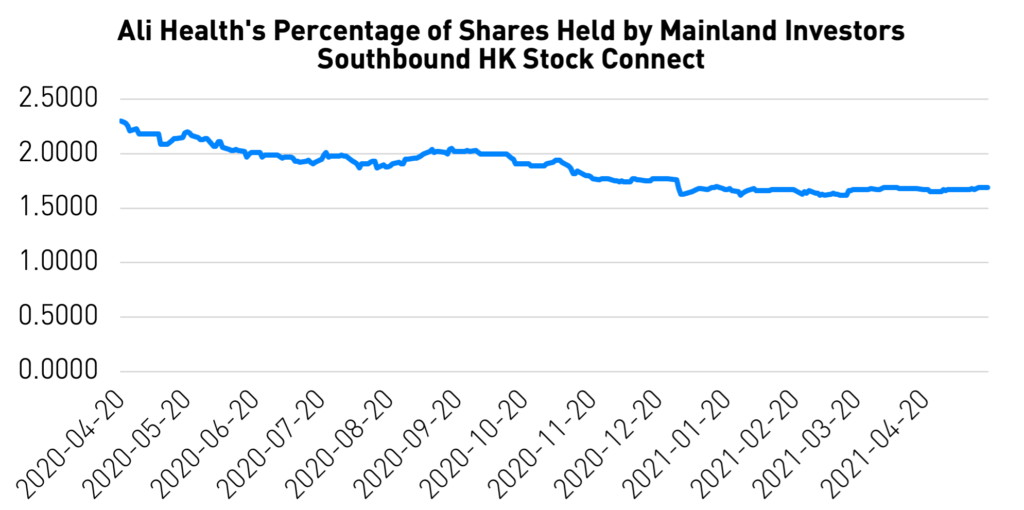

Below are 1-year charts showing the percentage of shares outstanding of the four Hong Kong-listed Chinese internet stocks held by Mainland investors via the Southbound Stock Connect as of yesterday. Against the backdrop of internet regulation, one would have thought these charts would be declining, but they have been rising.

H-Share Update

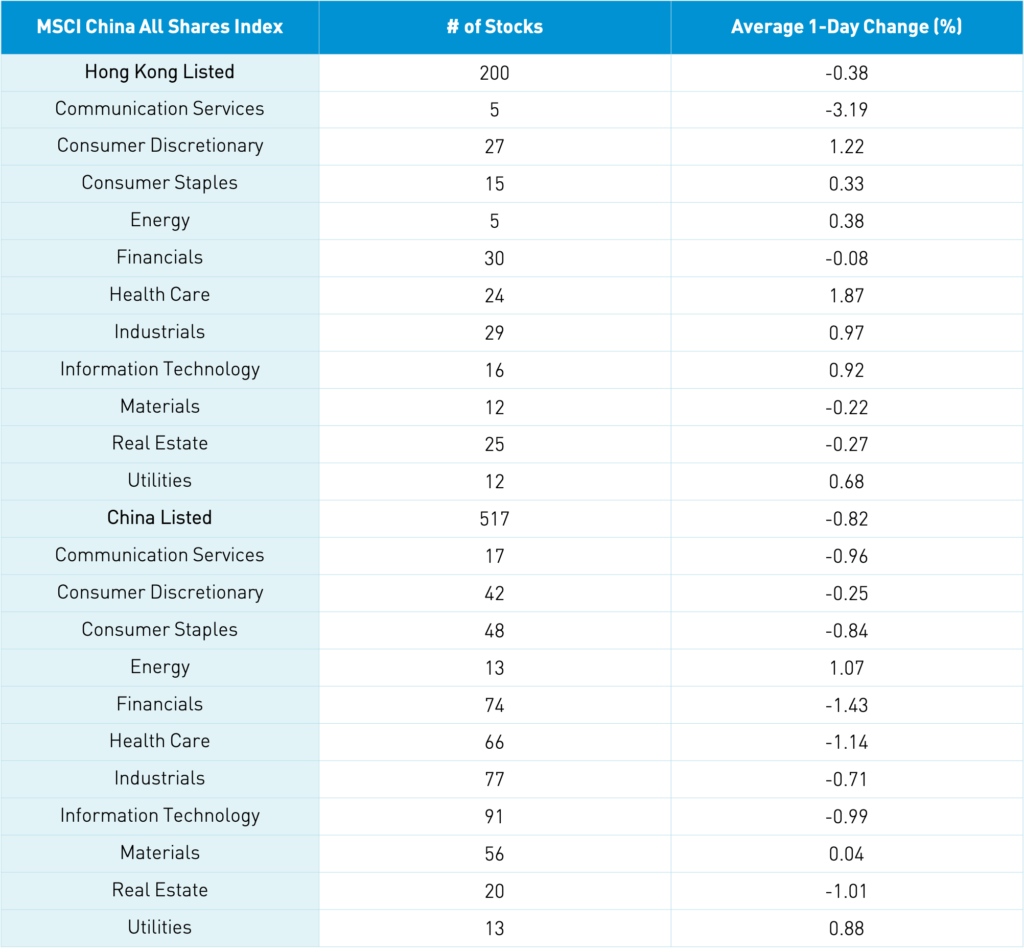

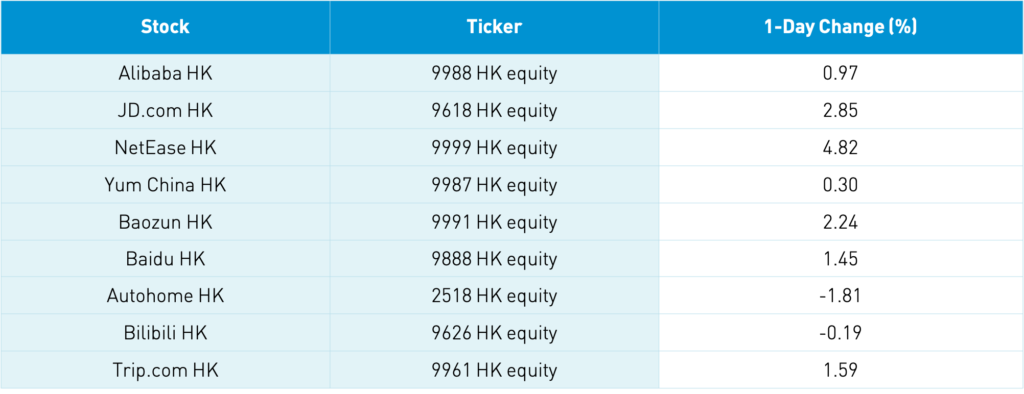

The Hang Seng retreated in the morning but managed to mitigate its losses to close up +0.03% at 28,458 as volume declined to just below the 1-year average. The 200 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index declined -0.37% as healthcare +1.87%, discretionary +1.22%, industrials +0.98%, and tech +0.93%. Meanwhile, communication fell -3.19% due to Tencent, and real estate fell -0.27%. Hong Kong’s most heavily traded stocks by value were Tencent, which fell -3.37%, Alibaba HK, which gained +0.97%, Meituan, which gained +0.735, Xiaomi, which gained +0.37%, JD.com HK, which gained +2.85%, Kuaishou Tech, which gained +5.73%, Ping An Insurance, which gained +0.43%, AIA, which gained +0.1%, Wuxi Biologics, which gained +2.31%, and BYD, which gained +1.86%. Southbound Stock Connect volumes were light as Mainland investors bought $263 million worth of Hong Kong stocks as Southbound trading accounted for 13.2% of Hong Kong turnover.

A-Share Update

Shanghai, Shenzhen, and the STAR Board were off -0.58%, -0.45%, and -1.1%, respectively, as volume was off -6.46%, which is 90% of the 1-year average. Breadth saw 2,024 advancers and 1,836 decliners. The 517 Chinese companies within the MSCI China All Shares Index were off -0.81% led by energy +1.07%, utilities +0.89%, and materials +0.05%. Meanwhile, financials -1.43%, healthcare -1.13%, real estate -1.13%, tech -0.99% communication -0.95% and staples -0.84%. The Mainland’s most heavily traded stocks were Chang An Auto, which gained +8.46%, Changchun High & New Tech, which fell -7.2%, East Money, which fell -3.44%, COSCO Shipping, which gained +10%, BYD, which gained +0.15%, Walvax Biotech, which fell -6.25%, BOE Tech, which gained +1.84%, Longi Green Energy, which fell -0.11%, CATL, which fell -0.57%, and Wuliangye Yibin, which fell -2.28%. Northbound Stock Connect volumes were moderate/high as foreign investors sold -$89 million worth of Mainland stocks as Northbound trading accounted for 5.6% of Mainland trading. Bonds rallied as the Chinese 10-Year Gov’t bond yield reached 3.09%, CNY was flat, and copper was off.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.43 versus 6.43 yesterday

- CNY/EUR 7.84 versus 7.86 yesterday

- Yield on 1-Day Government Bond 1.49% versus 1.50% yesterday

- Yield on 10-Year Government Bond 3.09% versus 3.10% yesterday

- Yield on 10-Year China Development Bank Bond 3.54% versus 3.52% yesterday

- Copper Price -0.60% overnight