Pinduoduo Smashes Analyst Expectations as Revenue Goes Vertical

4 Min. Read Time

Q1 Financial Results

E-commerce company Pinduoduo (PDD US) announced Q1 2021 financial results before the US market open. Topline growth was amazing, growing more than 3X from a year ago. This is a stunning result! Yes, expenses increased but the company was able to cut its loss significantly. I believe investors will cheer these results simply due to the strong growth despite the market’s preference for quality/positive net income/positive free cash flow over hyper-growth/profitless companies. The company released three other press releases related to logistics, agriculture modernization, and plant-based meats. The company is working with Singapore’s Agency for Science, Technology, and Research to “conduct a study examining the health impact of substituting animal proteins with plant-based proteins.” The company also emphasized its Duo Duo Grocery, “its next-day pickup service”, as the company calls itself “China’s largest agriculture platform”.

- Revenues increased +239% to $3.383B (RMB 22.167B) from Q1 2020’s RMB 6.541B and analyst expectations of RMB 19.714B

- Online marketing services revenue increased to $2.153B (RMB 14.111B) from Q1 2020’s RMB 5.492B

- Transaction services increased to $447mm (RMB 2.931B) from Q1 2020’s RMB 1.048B

- Monthly active users increased 49% to 724.6mm from487.4mm

- Active buyers for the last twelve months increased 31% to 823.3mm from 628.1mm from the previous twelve months

- Total costs of revenues increased+487% to $1.640.2B (RMB 10.746B) from Q1 2020’s RMB 10.746B

- Total operating expenses increased to $2.376B (RMB 15.568B) led by sales/marketing +78%, General/administrative expenses +4% and R&D +51%

- Operating loss was $633mm (RMB 2.905.4B) versus Q1 2020’s loss of RMB 4.119.3B

- Adjusted net loss was $288.5mm (RMB 1.890.3B) versus Q1 2020’s loss of RMB 3.169B and analyst expectations of RMB -1.89B

- Adjusted EPS loss was -$0.23 (RMB 1.52) versus analyst expectations of RMB -2.24

- Cash on the books was $12.7B (RMB 83.4B) from Q1 2020’s RMB 87B and 12/21/2019’s RMB 41.057B

Key News

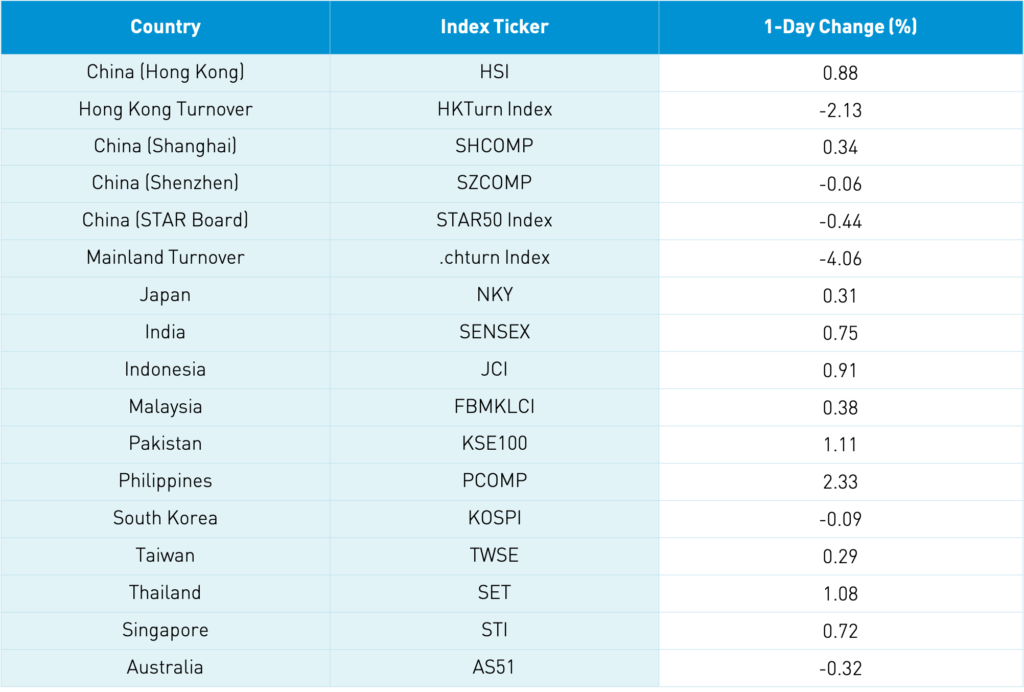

Asian equities were largely higher despite the US equity market move yesterday. China’s currency appreciated intra-day to 6.39 closing at 6.41 as the US dollar declines. Interesting to note China’s concern on commodity inflation versus the US Fed. The renminbi’s appreciation makes commodity prices cheaper to buy. China’s 10-Year Gov’t Bond is approaching the 3% level as bonds rallied overnight closing at 3.09%. KE Holdings (BEKE US) was off -2.81% yesterday despite denying rumors it was facing anti-trust fines. Watch BEKE tomorrow at 3:59 pm as it will see a very large net inflow due to MSCI’s Semi-Annual Index Review tomorrow. I’m not predicting it will go up or down but volume will go through the roof as passive index funds and ETFs buy the stock. TAL Education (TAL US) jumped +18% yesterday on rumors of after school tutoring rules in Beijing turned out to be false. Shanghai Composite got through the 3,600 level intra-day but closed at 3,593 after blasting through the 3,500 level yesterday. Shenzhen Composite is approaching the 2,400 level. Foreign investors bought $1.424B of Mainland stocks following yesterday’s purchase of $3.389B. Wish we had some of that flow!

NetEase Music filed for a Hong Kong IPO in addition to the online gaming company spinning off Cloud Village according to Bloomberg.

Mainland media noted a US-China Business Council press conference in Shanghai on the release of the 2021 State Export Report. The release reported US exports to China grew 18% year over year in 2020 to $123B with Texas the largest state by export value at $16.9B/+56% YoY ahead of California’s $14.8B while Louisiana had the largest year over year growth rate at 120% as the #10 state by export. China is the third-largest destination for US exports nearly double #4 Japan while behind Canada and Mexico. I’d assume energy exports were the drivers. Total annual sales from US companies operating in China exceeded $700B. Midwest agriculture states saw increases as exports of oilseeds (not a clue!) and grains nearly doubled powering Illinois, Iowa, Kansas, Minnesota, and Nebraska. Service exports were off due to limited travel which also affected the number of jobs supported by US trade with China which fell to 916,000 from 1.1mm. The report was sponsored by Caterpillar, Amway, Cargill, Cheniere, ConocoPhillips, and Walmart.

MSCI’s Semi-Annual Index Review should lead to a strong day of trading on Thursday at the close.

Autohome (ATHM US) reports earnings Thursday, MOMO and Meituan report on Friday.

H-Share Update

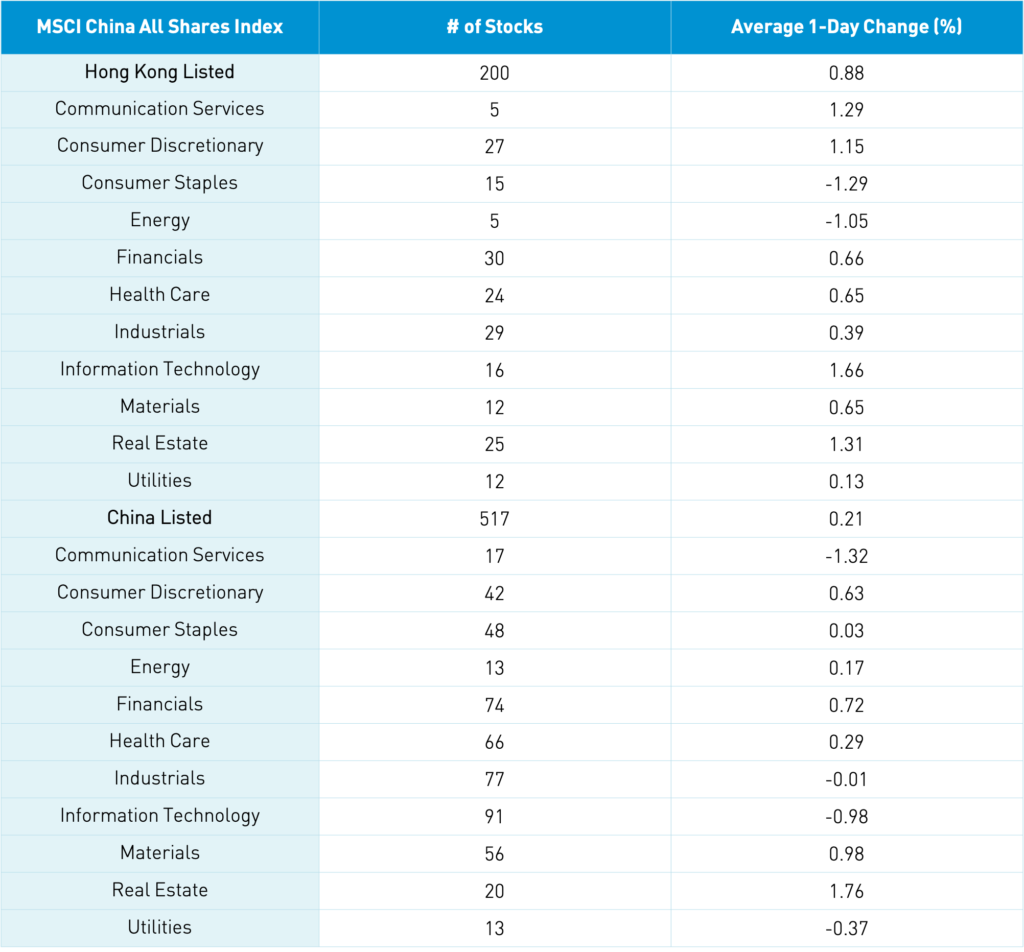

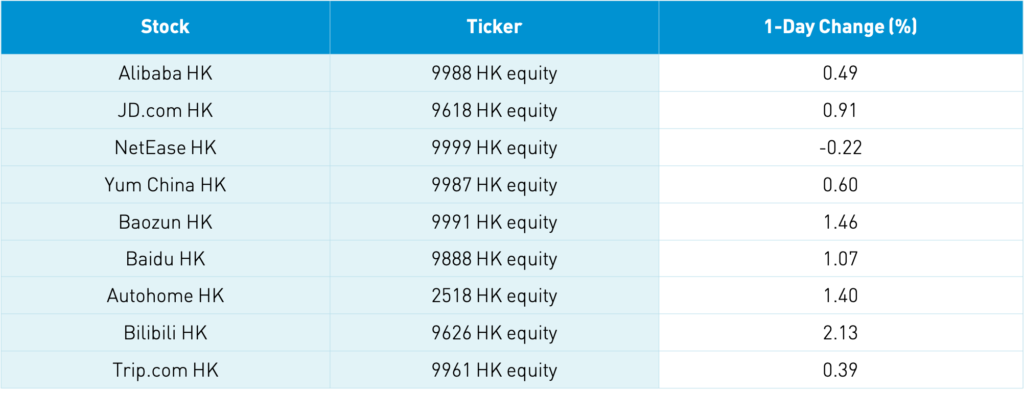

The Hang Seng gained +0.88% above the 29,000 level at 29,166 as volume declined -2% from yesterday which is 101% of the 1-year average. The 200 Chinese companies listed in HK within the MSCI China All Shares also gained +0.88% led by tech +1.66%, real estate +1.31%, communication +1.28%, and discretionary +1.15% while staples -1.29% and energy -1.05%. HK’s most heavily traded by value were Tencent +1.31%, Meituan +1.08%, Xiaomi +1.44% which reported strong results after the HK close, e-cigarette company Smoore -17.1% on weak results, Alibaba HK +0.49%, HK Exchanges +1.73%, Ping An +1.08%, Kuaishou Tech -0.39%, BYD Electronic +11.73% and Bank of China +0.32%. Southbound Connect volumes were above recent averages as mainland investors bought $104.996mm of HK stocks as Southbound trading accounted for 13.7% of HK turnover.

A-Share Update

Shanghai, Shenzhen, and STAR Board diverged +0.34%, -0.06%, and -0.44% on profit-taking following yesterday’s strong move. Volumes declined -4% from yesterday though still 107% of the 1-year average while breadth saw 2,389 advancers and 1,424 decliners. The 517 mainland stocks within the MSCI China All Shares gained +0.2% led by real estate +1.76%, materials +0.97%, financials +0.71% and discretionary +0.62% while communication -1.33%, tech -0.99% and utilities -0.38%. Semis were off today though I don’t see any news on why. The Mainland’s most heavily traded by volume were broker East Money -0.95%, Kweichow Moutai +1.16%, Fosun Pharma +8.01%, Sany Heavy Industry +1.68%, BYD -0.2%, liquor stock Wuliangye Yibin -1.25%, Industrial Securities +10% (our old friend Rex works there so hopefully he owns shares), COSCO Shipping -2.45%, Ping An -0.11% and Changan Auto +3.02%. Foreign investors bought $1.424B of mainland stocks today following yesterday’s $3.389B as Northbound trading accounted for 5.4% of mainland turnover. Copper was off -0.66%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.40 versus 6.41 yesterday

- CNY/EUR 7.82versus 7.85 yesterday

- Yield on 1-Day Government Bond 1.48% versus 1.53% yesterday

- Yield on 10-Year Government Bond 3.06% versus 3.09% yesterday

- Yield on 10-Year China Development Bank Bond 3.54% versus 3.52% yesterday

- Copper Price -0.66%