MSCI’s Index Rebalance Review

3 Min. Read Time

Key News

Asian equities were largely higher on high volumes as today is the trade day for MSCI’s Semi-Annual Index Review (SAIR). Watch out for BEKE US and LI US today as they are significant net inflow stocks. I’m not predicting whether they will go up or down, but their volumes will skyrocket! We shouldn’t read too much into today’s trading due to the MSCI changes as Hong Kong’s volumes increased 52% from yesterday, which is 154% of the 1-year average. For instance, Tencent was off in Hong Kong due to media reports related to the regulatory-driven spin-off of its consumer lending unit, which is a very small part of the firm’s revenue. Tencent, similar to Alibaba, are net-sells in the MSCI rebalance as new holdings need to be funded from other holdings, especially the top holdings such as Alibaba, Tencent, Taiwan Semi (-0.5%), and Samsung (-0.25%).

MSCI is transitioning to Alibaba’s Hong Kong share class from the US share class today. Asset managers will convert their Alibaba US ADR shares after the close through the ADR custodian bank, which is Citibank. The #1 and #3 largest EM equity ETFs in the US and globally will convert their shares today following the #2 and #5 largest EM equity ETFs conversion, following FTSE Russell’s transition to the Hong Kong share class earlier this year. It will be interesting to see how the impact of this change affects the US’ ADRs volume going forward.

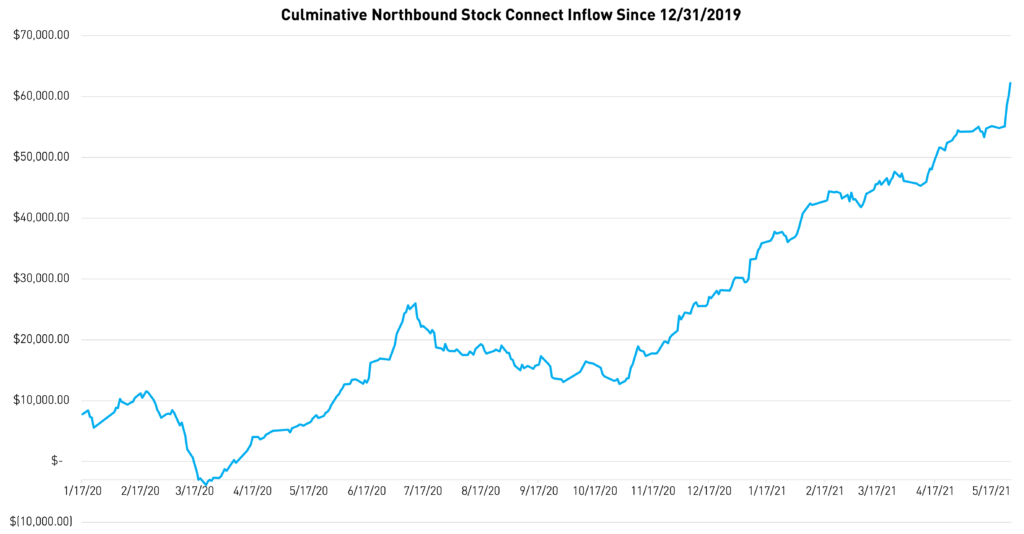

The WSJ noted the strong inflows into China’s equity market. I would disagree that it is driven by CNY’s appreciation versus the US $. Yes, CNY appreciated overnight to 6.37 versus the dollar, though recent flows into China are likely driven by MSCI’s rebalance as we had a healthy $2.294B invested today following Wednesday’s inflow of $1.424B and Tuesday’s $3.389B. YTD foreign investors have bought $31.204B of Mainland stocks and $62.209B since 12/31/2019. If you want to play the currency, one would buy bonds or buy the currency forwards.

US Trade Representative Tai spoke with her Chinese counterpart Vice Premier Liu He this morning. At least they are talking!

Mainland semiconductor stocks had a very strong day on shortage concerns. JD Logistics’ Hong Kong IPO tomorrow should be significant as the small retail allocation was oversubscribed 700X with the stock up nearly 30% in non-exchange/over-the-counter trading.

Foreign investors aren’t the only ones buying Chinese Mainland stocks recently. A Mainland-listed equity ETF holding large-cap stocks had its 2nd largest inflow day ever as investors invested $943mm into the ETF on Wednesday.

The first REITs will be launched on the Shanghai Stock Exchange soon.

Autohome (ATHM US and 2518 HK), “the leading online destination for automobile consumers in China”, provided results before the US market open today. ATHM has underperformed fairly significantly as the company wants to sell more cars directly to consumers versus creating lead generation for dealers. The results were a slight beat versus analyst expectations, though the company announced that its co-President is resigning.

- Revenues increased 19.1% to $281.1mm (RMB 1.841B) versus analyst expectations of RMB 1.842B

- Operating profit was $86.5mm (RMB 56mm) versus Q1 2020’s RMB 585mm and analyst expectations of RMB 675mm

- Adjusted Net Income $112mm (RMB 734mm) versus Q1 2020’s RMB 646mm and analyst expectations of RMB 675mm

- Adjusted EPS $0.92 (RMB 6.06) versus Q1 2020’s RMB 5.40 and analyst expectations of RMB 5.84

- Cash on the books was $2.636B (RMB 16.83mm)

H-Share Update

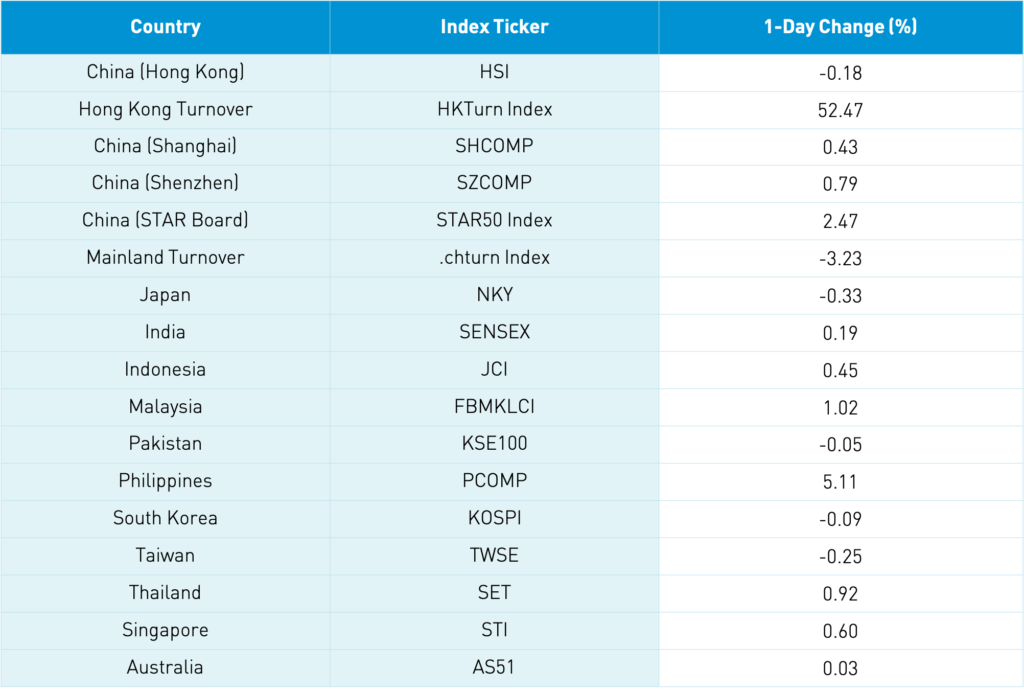

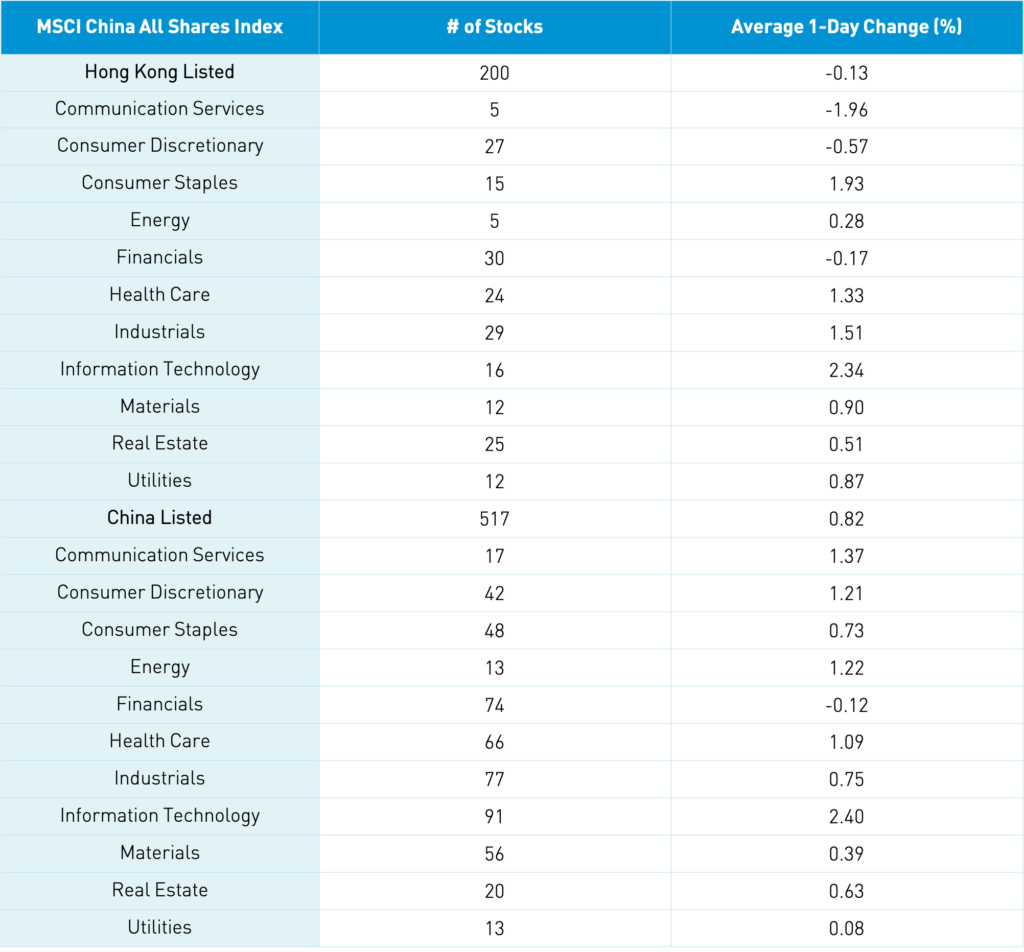

The Hang Seng was off -0.18% as volumes jumped 52% from yesterday driven by MSCI’s index rebalance, which is 154% of the 1-year average. The 200 Chinese stocks listed in Hong Kong within the MSCI China All Shares Index were off -0.14%, with tech up +2.33%, staples +1.92%, industrials +1.5%, and healthcare +1.32%, while communication fell -1.96%, and discretionary -0.57%. Hong Kong’s most heavily traded by value were Tencent, which fell -2.02%, Xiaomi, which rose +3.2% post yesterday’s strong financial results, Meituan, which fell -2.79%, Ping An, which rose +1.01%, Alibaba Hong Kong, which rose +0.87%, e-cigarrete company Smoore, which rose +3.42%, China Feihe, which rose +0.95%, ICBC flat, AIA, which fell -0.2%, and Chow Tai Fook Jewelry, which rose +1.27%. Southbound Connect volumes were moderate as Mainland investors sold $104mm of Hong Kong stocks as Southbound trading accounted for 8.7% of Hong Kong turnover.

A-Share Update

Shanghai, Shenzhen, and STAR Board gained +0.43%, +0.79%, and +2.47% respectively as Mainland turnover decreased -3.23% from yesterday, which is just above the 1 year average. There were 2,249 advancing stocks and 1,468 declining stocks. The 517 Mainland stocks within the MSCI China All Shares Index gained +0.82%, led by tech +2.33%, communication +1.3%, energy +1.15%, discretionary +1.13%, and healthcare +1.02% while financials were off -0.19%. The Mainland’s most heavily traded were Kweichow Moutai, which rose +1.13%, broker East Money, which rose +0.38%, Sany Heavy Industry, which rose +2.41%, Gree Electric Appliances, which rose +3.29%, liquor stock Wuliangye Yibin, which fell -0.26%, Kingfa Sci & Tech, which rose +2.03%, Changchun High & New Tech, which fell -2.83%, Industrial Securities, which fell -0.2%, EVE Energy Co, which fell -2.66%, and Longi Green Energy, which fell -0.88%. Northbound Stock Connect volumes were high as foreign investors bought $2.294B of Mainland stocks as Northbound trading accounted for 7.6% of Mainland turnover. CNY appreciated to 6.37 versus the US $, bonds and copper were off.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.37 versus 6.39 yesterday

- CNY/EUR 7.78 versus 7.82 yesterday

- Yield on 10-Year Government Bond 3.07% versus 3.06% yesterday

- Yield on 10-Year China Development Bank Bond 3.54% versus 3.54% yesterday

- Copper Price -0.14% overnight