Ant Group’s Transformation from Fintech to Consumer Finance Company Approved

3 Min. Read Time

May Services PMI Release Overview

The pace of service sector growth slowed in May versus April. The release was the thirteen-month of expansion for the Services PMI. The dip according to IHS Markit, who conducts the survey on behalf of Caixin, was related to foreign demand slipping due to the pandemic. Asia is China’s largest trade partner so the recent flare-ups and lockdowns in SE Asia and Japan could be a factor. Employment and business expectations rose though input prices rose as well. The PBOC is a central bank that is taking inflation seriously so today’s reading will be noted. Very few of our institutional brokers noted today’s release, indicating it was not a market-moving event.

Key News

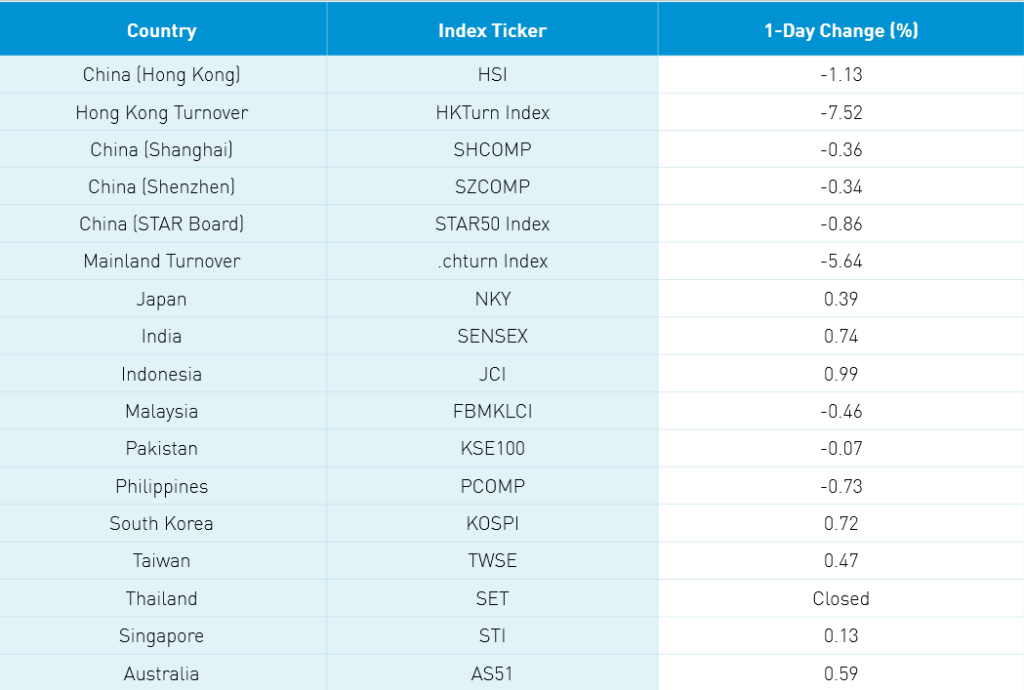

Asian equities were mixed today as Southeast Asia was largely off and North Asia gained though China and Hong Kong didn not get the message. The Biden administration announced the list of banned Chinese stocks will be reviewed and maintained by the Treasury Department’s Office of Foreign Assets Control and not the Defense Department going forward after two Chinese companies successfully challenged their presence on the list in court and won. The hastily thrown together Executive Order was exceedingly confusing for US asset managers due to the lack of transparency nor communication. We’ll see if things improve going forward.

Ant Group’s transition from an unregulated fintech to a regulated consumer finance company took a step forward as the CBIRC approved the new entity. The company will have to hold 30% of loans it helps originate, stop lending to college students, and lower the maximum loan amount to RMB 200,000. The move could accelerate an IPO, likely after a few quarters of new financials under the new regulations. It is interesting to note that EV battery maker CATL owns an 8% stake in Ant, according to the Wall Street Journal.

FTSE Russell’s pro-forma for its index rebalance was released with small changes to the FTSE A50 and China 50 indexes. This Friday is the Hang Seng Index inclusion of EV bus maker BYD among the three additions.

Huawei-related stocks were up after the company announced its new HarmonyOS smartphone. The market didn’t have a tone nor tenor/rhyme nor reason for trading action. One respected broker felt the market is consolidating after the strong run since May, which we noted yesterday.

H-Share Update

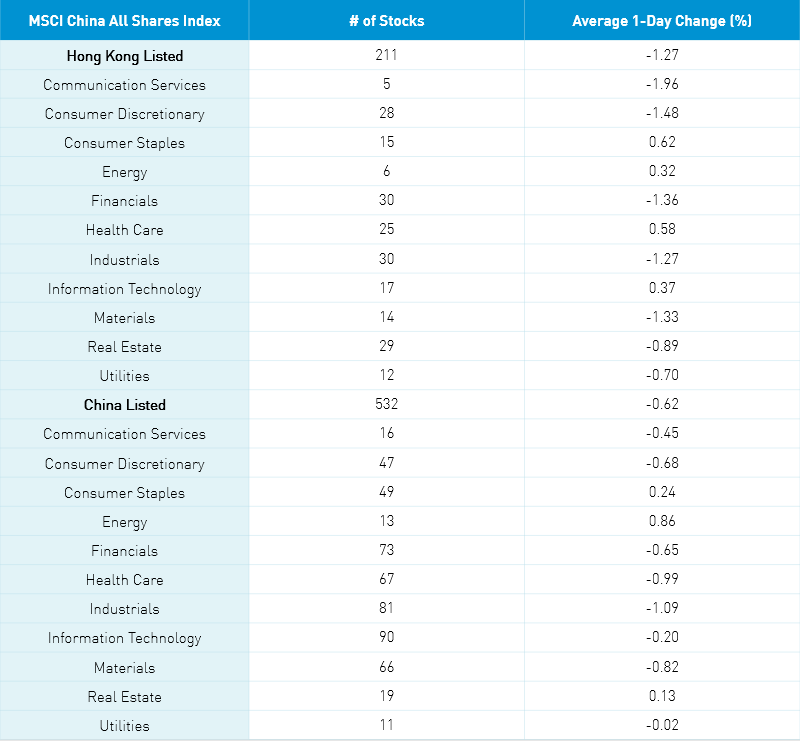

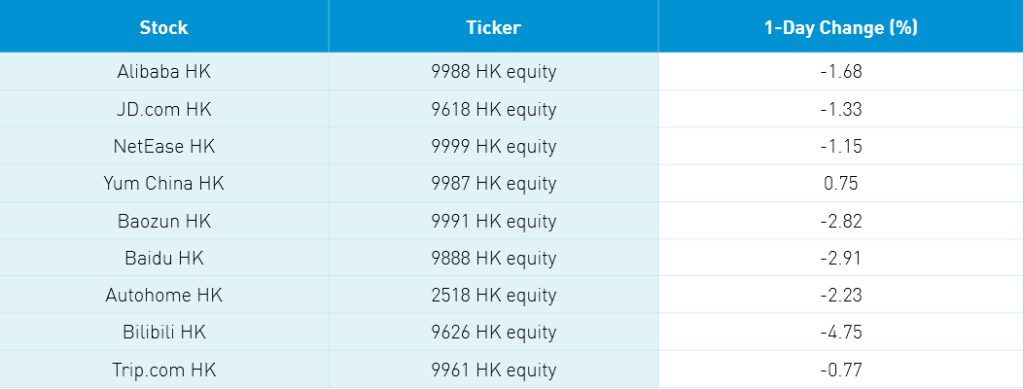

The Hang Seng opened higher but gravity took effect as the index dipped below the 29k level at 28,966 off -1.13%. Volume was off -7.5% which is 85% of the 1-year average. The 211 Chinese companies listed in HK within the MSCI China All Shares were off -1.27% with tech +0.37% and energy +0.32% while communication -1.96%, discretionary -1.48%, financials -1.36%, materials -1.33%, industrials -1.27% and real estate -0.89%. HK’s most heavily traded by value were Tencent -2.07%, Meituan -1.41%, Xiaomi +2.39%, Alibaba HK -1.68%, AIA -1.61%, Ping An -1.38%, China Construction Bank -2.06%, HK Exchanges -1.78%, Geely Auto -2.1% and AAC Tech +5.22%. Southbound Connect volumes were moderate with mainland investors buying $56mm of HK stocks today as Southbound Connect trading accounted for 13% of HK turnover.

A-Share Update

Shanghai, Shenzhen and STAR Board bounced around the room though slumped into the close-off -0.36%, -0.34% and -0.86%. Volumes were down -5.64% from yesterday which is 103% of the 1-year average while breadth saw 2,080 advancers and 1,747 decliners. The 532 mainland stocks within the MSCI China All Shares were off -0.71% as energy +0.76%, staples +0.14% and real estate +0.04% while tech -1.3%, industrials -1.18%, healthcare -1.09% and materials -0.92%. Mainland’s most heavily traded by value were broker East Money +0.72%, Longi Green Energy -4.53%, COSCO Shipping -4.38%, liquor stock Wuliangye Yibin +0.57%, ZTE +6.64%, Kweichow Moutai +0.01%, CATL -2.29%, Yihai Kerry +6.22%, China Northern Rare Earth +3.7% and BYD -1.39%. Northbound Stock Connect volumes were moderate as foreign investors bought $237mm of mainland stocks today as Northbound Connect trading accounted for 5.1% of mainland turnover. CNY was basically flat versus the US $, bonds appreciated and copper was off -1.23%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.39 versus 6.38 yesterday

- CNY/EUR 7.78 versus 7.80 yesterday

- Yield on 1-Day Government Bond 6.45% versus 1.70% yesterday

- Yield on 10-Year Government Bond 3.06% versus 3.07% yesterday

- Yield on 10-Year China Development Bank Bond 3.54% versus 3.52% yesterday

- Copper Price 1.23% overnight