Grocery Delivery Company Missfresh Files for US IPO

3 Min. Read Time

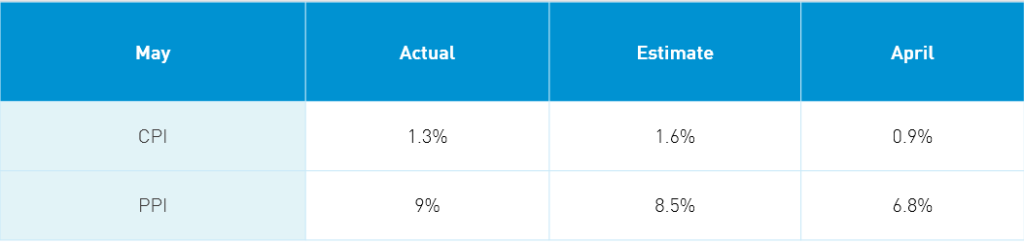

May YoY Consumer Price Index (CPI) & Producer Price Index (PPI) Release Overview

Takeaway: The PPI print was driven by mining’s +36.4%, raw materials +18.8% and manufacturing +7.4% driven by higher commodity prices. Higher commodity inputs are largely being eaten by manufacturers rather than being passed along to end consumers. CPI saw transportation and communication increase 5.5% YoY while food was a mild +0.8%.

The mid-morning release didn’t seem to be a market-moving event as the higher PPI print was largely expected. We should expect further efforts by the PBOC to talk down higher commodity prices but the laws of supply and demand are hard to overcome. This too shall pass as commodity suppliers ramp up production to meet demand though that doesn’t occur overnight.

Key News

Northern Asian markets were largely off, less China which posted a gain while Southern Asian markets were largely higher though volumes were off in advance of tomorrow’s US CPI release. The World Bank’s upgrade of their global GDP forecast garnered attention as China’s 2021 GDP forecast was raised to 8.5%.

The Senate passed the $250B bill which includes ~$50B for US semiconductor companies to compete with China (FYI – the big semi companies are in Taiwan and South Korea). The markets didn’t care as we’ve become somewhat numb to US-China political rhetoric. I stumbled upon an article titled “Playing the China Card” by a media outlet called Noema that I recommend. It highlights how politicians have used threats, real or imaginary, to push policies.

Mainland and Hong Kong energy stocks had a strong day as oil punched above $70 a barrel while PPI led material stocks higher. There was a touch of value outperforming growth but it was a quiet night. Healthcare outperformed as a coronavirus outbreak in Guangzhou has led to a local lockdown. Online education stocks were off again as investors worry about new tutoring rules. Alcohol stocks were off again though Kweichow Moutai did manage to post a small gain.

A lot of investors prefer active management for emerging market investing. I’m a believer in using both as there are pros and cons to active management just as there are pros and cons to passive investing. For China’s mainland market, I believe there is a strong case for one to hold beta/index exposure. There is some evidence of this. According to a Chinese data provider, the “big fund index”, comprised 3,968 mutual funds with CNY 6.1 trillion of assets--which is the largest category, has returned 5.07% year to date versus the MSCI China A Index return of 5.18%. The 1-year return for the “big fund index” was 37% versus the MSCI China A’s return of 51%. The MSCI index beat the active managers in these two time periods. I’ll do some more work here and report back.

Diving into the mainland manager data, I couldn’t help but notice that the 2,041 big growth funds manage RMB 3.511 trillion versus the 336 big value funds manage RMB 372B. The value/growth trade is a global phenomenon!

Tencent, Goldman Sachs and Tiger Global backed online grocery delivery company, Missfresh, filed its F-1 with the SEC yesterday in advance of a Nasdaq listing under the ticker MF. Missfresh operates 631 “distributed mini-warehouses” in 16 cities as of Q1 2021, allowing the company to source items from farmers directly. The company was founded in 2014 and now has 7.9mm users for the year ended Q1 2021, having sold RMB 7.6B worth of goods in 2020 with an average delivery time of 39 minutes. The company generated $915mm (RMB 5.999B) of revenue in 2020 and $227mm (RMB 1.492B) in Q1 2020. The company had a net loss of $251mm in 2020 and $93mm in Q1 2021. The filing is a big filing that I’m making my way through though the company is clearly disrupting the traditional grocery store model.

H-Share Update

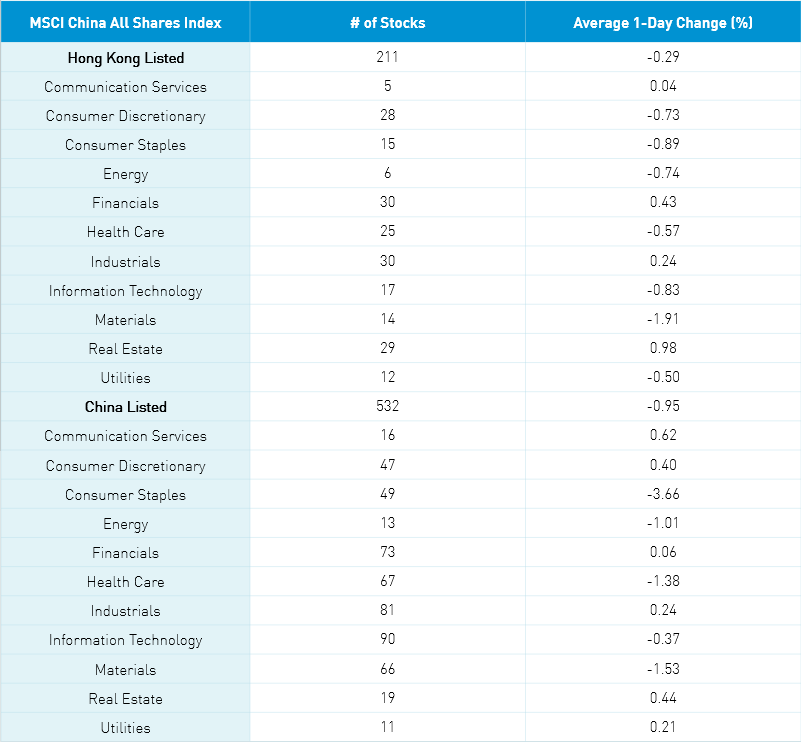

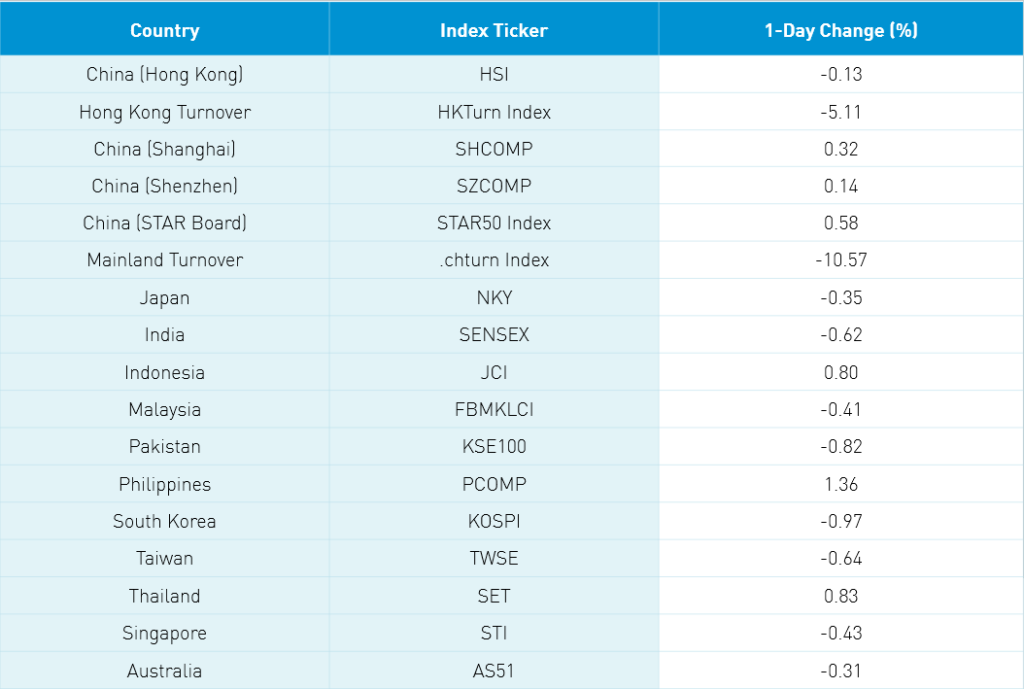

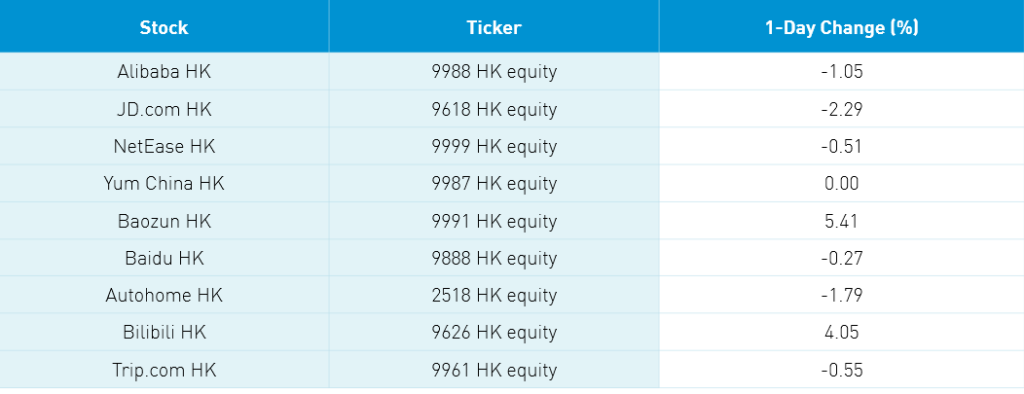

The Hang Seng bounced around the room, closing -0.13% at 28,742 as volume declined -5.1% from yesterday, which is only 71% of the 1-year average. The 211 Chinese companies listed in Hong Kong within the MSCI China All Shares were off -0.08% with energy +1.79%, healthcare +0.78%, utilities +0.56%, materials +0.45%, communication +0.34%, real estate +0.33% and staples +0.23% while discretionary -0.81%, financials -0.13% and tech -0.1%. Hong Kong’s most heavily traded were Tencent +0.33%, Meituan -1.28%, Alibaba HK -1.05%, Xiaomi -1.59%, China Feihe -6.6%, energy giant CNOOC +2.95%, BYD -1.04%, AIA -0.67%, JD.com HK -2.29% and Geely Auto -1.64%. Southbound Stock Connect volumes were moderate as mainland investors bought $138mm of Hong Kong stocks today as Southbound trading accounted or 13.8% of Hong Kong turnover.

A-Share Update

Shanghai, Shenzhen and STAR Board gained +0.32%, +0.14% and +0.58% as volume declined -10.57% from yesterday to 95% of the 1-year average. The 531 mainland stocks within the MSCI China All Shares gained +0.34% led by energy +3.06%, Utilities +1.44%, materials +1.19, tech +1.03% and staples +0.44% while communication -1.24%, real estate -0.44%, financials +0.39% and discretionary -0.37%. The Mainland's most heavily traded by volume were COSCO Shipping +4.45%, broker East Money -1.52%, Inner Mongolia Yili +5.18%, BYD -0.4%, Shede Spirits -5.44%, Jiangsu Hoperun Software +20.01%, Kweichow Moutai +0.39%, Wuliangye Yibin -0.49%, China Baoan Group +5.33%, and Everbright Securities -6.89%. Northbound Stock Connect volumes were moderate as foreign investors bought $440mm of mainland stocks as Northbound Stock Connect trading accounted for 5.1% of mainland turnover. CNY appreciated versus the US $ slightly, bonds were flat and copper gained +0.31%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.39 versus 6.40 yesterday

- CNY/EUR 7.79 versus 7.79 yesterday

- Yield on 1-Day Government Bond 1.65% versus 1.68% yesterday

- Yield on 10-Year Government Bond 3.11% versus 3.11% yesterday

- Yield on 10-Year China Development Bank Bond 3.54% versus 3.54% yesterday

- Copper Price 0.31% overnight