WeChat/TikTok Reprieve as US-China Commerce Heads Talk

4 Min. Read Time

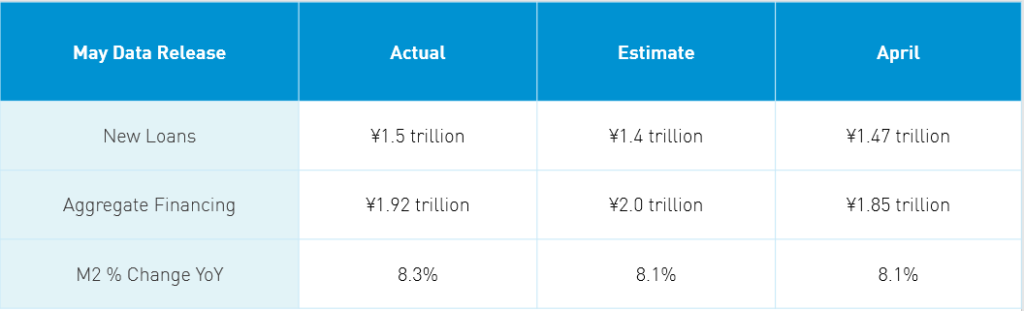

May Data Release

Takeaway: The economy is looking good! Numbers speak for themselves. Few brokers were focused on the release.

Key News

Asian equities were largely higher as investors cheered lower US Treasury yields in advance of this morning’s CPI release. News that President Biden canceled the previous administration’s ban on Tik Tok and Tencent’s WeChat was cheered by Mainland investors. However, they are not out of the woods yet as their data collection practices will be examined by the Commerce Department. I recall that Tencent was reported to be building European data centers, which I assume would house US users' WeChat data to accommodate US concerns. TikTok, which fired Alibaba’s cloud unit in Q1, likely has already done the same as I assume US users' TikTok data is now with Amazon’s AWS, Microsoft, or another US cloud provider.

US Commerce head, Gina Raimondo, spoke with China’s Commerce Minister Wang Wentao today on trade following recent calls with US Trade Rep Tai and Treasury chair Yellen. While bashing China polls well, there is clearly dialogue occurring behind the scenes. Maybe there is an understanding in the media we are going to throw each other under the bus but not really hurt one another. I am speaking with a DC insider today and hope to receive further insights.

PBOC head, Yi Gang, spoke yesterday at the Lujiazui Forum touching on China having to address demographic issues that will weigh on economic growth in the future. Addressing inflation, he stated high commodity prices have led to “short-term rise of global inflation has become a fact, but there are huge differences on whether inflation can continue for a long time.” The PPI is driven by the year-over-year comparison while CPI is expected to stay below 2%. Monetary policy should be “stable” ie no interest rate hikes. Very positive news! He also spoke about the need for green finance so China can meet carbon emission goals. Clean Tech stocks such as electric vehicles (EV), solar, wind, lithium, etc. had a strong day as CATL surged on reports Apple will rely on the company as well as BYD for its EV effort.

Chinese education stocks have been hammered this year on expectations that new rules may curtail the hours students can use tutors. The charts of TAL US and EDU US are painful to look at. The worst-case scenario is students won’t be allowed to use tutors (online or in-person) on the weekends, during school vacation days, or over the summer. One way to promote parents having more children is to cut the costs related to children. China’s rigorous education testing leads Chinese parents to spend a lot of money on tutoring which has increased focus on the tutoring space. The real problem is the testing regime and city living makes having kids expensive. I spoke yesterday with a top China Internet analyst who said if the worst case comes to fruition, the stocks might not be at their lows yet. At the same time, she did not believe this would come to fruition, which might make the stocks oversold. A government media release overnight stated the obvious: it’s not the tutoring, it's the testing. However, the release does highlight the lack of regulation in the tutoring space as a problem that needs to be addressed. In Hong Kong last night, EDU’s listing, 9901 HK, surged +19.3% as the worst-case scenario appears unlikely.

Tonight, MSCI will announce its country classification and global market accessibility reviews. This is an opportunity for MSCI to opine on two issues near and dear to me. The first is raising the inclusion factor of Chinese A-shares (the stocks within MSCI China A) within broader indexes such as MSCI Emerging Markets. Currently, the nearly five hundred large and mid-caps only have 20% of their potential weight included, representing 4.83% of the MSCI Emerging Markets (EM) Index. We know that, at full inclusion, these securities would represent 20% of MSCI EM which would raise China from nearly 40% to 50% of the index. We just don’t know the timing though tomorrow we will receive some clarity.

Due to the current state of US-China political rhetoric, I find it unlikely that MSCI will include them, though we could see an announcement on a year-long consultation. MSCI would then go and speak to their clients on the issue and get their thoughts. The other issue is MSCI potentially upgrading South Korea to developed market status out of emerging markets. Another consultation could be announced on this issue as Sout Korea handily meets GDP per capita criteria but the lack of an offshore currency is problematic.

H-Share Update

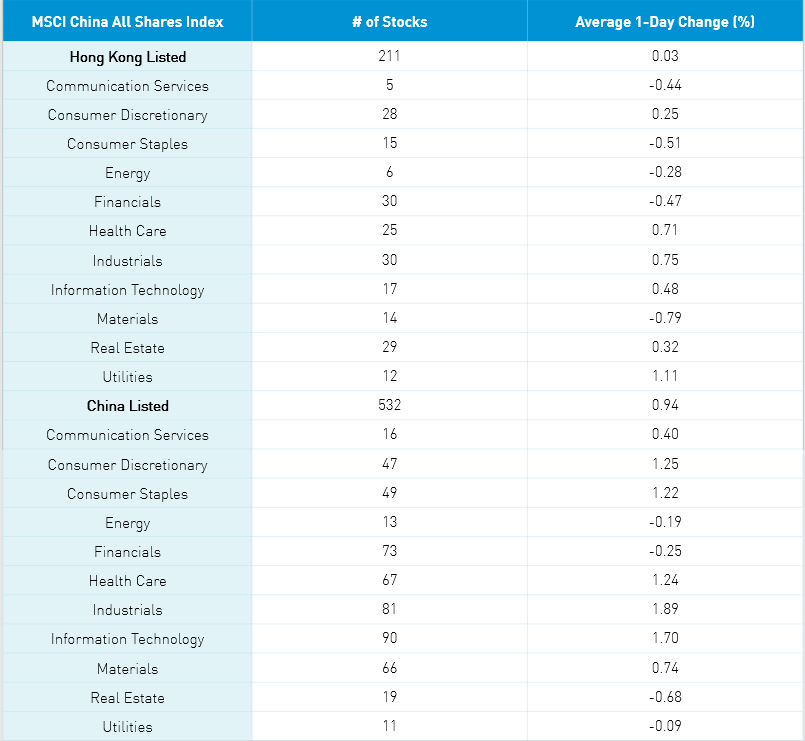

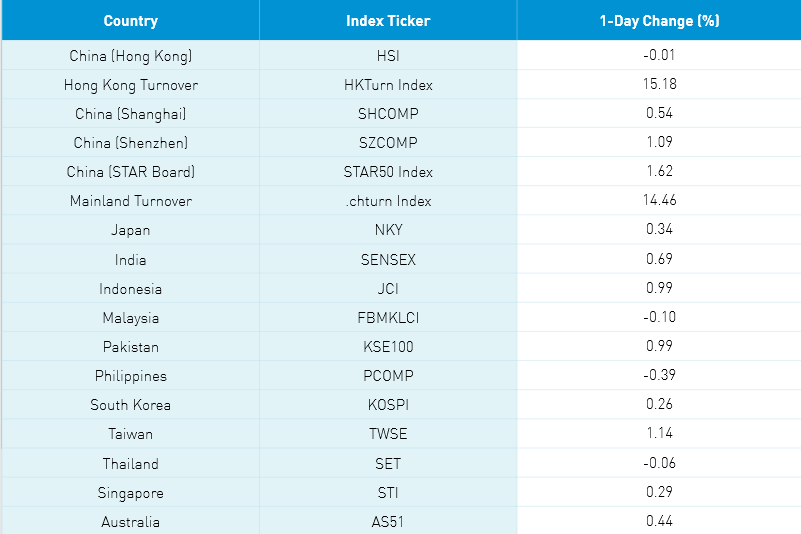

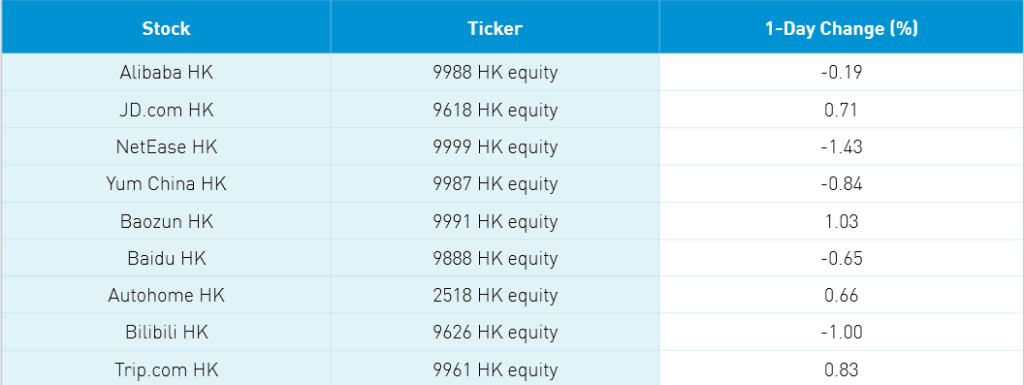

The Hang Seng Index and Hang Seng Tech Index came off morning gains to close -0.01% and -0.04% at 28,738 as volumes increased 15% from yesterday which is 82% of the 1-year average. The 211 Chinese companies listed in HK within the MSCI China All Shares gained +0.03% led by utilities +1.11%, industrials +0.75%, healthcare +0.71%, tech +0.48%, real estate +0.31% and discretionary +0.25% while materials -0.79%, staples -0.51%, financials -0.47%, communication -0.44% and energy -0.28%. HK’s most heavily traded by value were Tencent -0.41%, Meituan +1.64%, COSCO Shipping +11.63%, BYD +6.27%, Alibaba HK -0.19%, Xiaomi +0.9%, Chinasoft International +18.8%, Ping An -0.61%, Sunny Optical -1..8%, and Geely Auto +1.15%. Southbound Stock Connect volumes were moderate as mainland investors sold $210mm of HK stocks as Southbound trading accounted for 14.8% of HK turnover.

A-Share Update

Shanghai, Shenzhen, and STAR Board gained +0.54%, +1.09% and +1.62% as volume jumped +14.46% which is 109% of the 1-year average. The 531 mainland stocks within the MSCI China All Shares gained +0.94% led by industrials +1.89%, tech +1.7%, discretionary +1.25%, healthcare +1.24%, staples +1.22% and materials +0.74% while real estate -0.68%, financials -0.19% and energy -0.19%. The Mainland’s most heavily traded by value were Longi Green Energy +6.72%, broker East Money +2.93%, BYD +6%, COSCO Shipping +10.02%, CATL +6.17%, Sungrow Power +10.61%, Jiangsu Hoperun Software +20.01%, Kweichow Moutai +1.77%, Sany Heavy Industry -2.66% and Shede Spirits -10%. Northbound Stock Connect volumes were moderate as foreign investors bought $1.067B of mainland stocks as Northbound Stock Connect accounted for 6.5% of mainland turnover. CNY was basically flat, bonds rallied, and copper off -0.17%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.39 versus 6.39 yesterday

- CNY/EUR 7.78 versus 7.79 yesterday

- Yield on 1-Day Government Bond 1.65% versus 1.68% yesterday

- Yield on 10-Year Government Bond 3.10% versus 3.11% yesterday

- Yield on 10-Year China Development Bank Bond 3.52% versus 3.53% yesterday

- Copper Price -0.17% overnight