Didi Files For US Listing, Week in Review

4 Min. Read Time

Upcoming Webinar:

Join us on Thursday, June 24th at 11:00 am EDT for:

What’s Driving the Global Carbon Allowance Rally?

Click here to register.

Week in Review

- China reported Monday that exports rose +18.1% year-over-year in May compared to an estimated +19.5%. While the reported figure missed a sky-high estimate, export growth may accelerate in the months ahead as the global economy continues to come back online.

- China’s Producer Price Index (PPI) for May was also released this week, indicating an average increase of +9% year-over-year in the prices that factories and other producers pay for their inputs. The strong increase reflects surging commodity prices that, in China’s case, have largely not been passed down to the consumer, considering the May CPI’s lackluster +1.3% increase.

- Missfresh, an online grocery delivery company based in China, filed for a US listing on Tuesday. The company is the latest to file for a US listing despite the perception of ballooning political headwinds US-listed Chinese companies.

- The Biden Administration has revoked the ban on China-based apps TikTok and WeChat in favor of a broad national security review of all software applications potentially connected to foreign governments.

Didi IPO Overview

Didi filed for a US IPO yesterday. For those not familiar with Didi, it is a ride-hailing app similar to Uber or Lyft though significantly larger financially. Didi generated revenues of $5.99 billion in Q1 2021 versus Uber’s $3.5 billion and revenues of $20.40 billion in 2020 versus Uber’s $11.10 billion. The company made a profit in Q1 2021 for the first time, though it was driven by an investment gain. Having met with Didi back in 2019, I came away very impressed with the company.

Investors will be intrigued by the company’s directors as they include Martin Lau, the president of Tencent, Kentaro Matsui of Softbank, Daniel Zhang, who is also the Chairman of Alibaba, and Adrian Perica of Apple. I suspect Apple’s electric vehicle efforts are farther along than the company has let on based on both chatter that Apple is collaborating with BYD and CATL and its association with Didi. Didi might be the only company globally that boasts both Tencent and Alibaba as shareholders. The two rivals tend to avoid one another.

The company’s filing articulates the opportunity set for the company. 70% of China’s population is projected to be living in cities by 2030. Furthermore, the high cost of car ownership in China is another factor driving current usage. Below are a few stats from the company’s filing:

- 493mm active annual users

- 15mm active drivers

- 41mm rides daily (not a typo)

The company’s filing begs the question of why would they list in the US?

1) Hong Kong’s market is large, but it is nowhere near the size of the US market. For instance, the value of trading in Alibaba’s US share class is $3.8 billion versus Alibaba’s Hong Kong listing’s $733 million.

2) Virtually none of our institutional brokers believe delisting driven by the Holding Foreign Companies Accountable Act (HFCA) will occur. There is too much money involved across US stock exchanges, investment bankers, lawyers, accountants, etc.

3) US private equity firms probably prefer a US listing, which allows them to exit their positions with ease. The other factor is the valuation premium that US tech shares command versus other global markets.

Key News

Asian equities had a mixed day in advance of a three-day weekend for Hong Kong, China, Australia, and Taiwan. Mainland China saw high trading volumes driven by domestic indexes rebalancing.

FTSE Russell’s pro-forma for its semi-annual index review was released last night, which appears to include a large inflow for Chinese stocks in Hong Kong.

Electric bus maker BYD did well, once again, as the CEO was interviewed at the Yabuli China Entrepreneur Forum, where he made some very confidant statements about the company’s outlook while taking a shot at Huawei’s electric vehicle (EV) efforts. The EV space was a top performer driven by the BYD comments along with May auto sales gaining +3.1% year over year. EV battery maker CATL is on fire as China EV sales grow along with chatter of Apple entering the space.

Liquor stocks were weak today as foreign investors sold Kweichow Moutai. Sell volume in the stock outpaced buy volume by 3 to 1. Yesterday’s news about a higher alcohol tax may have spooked foreigners.

MSCI released their Global Market Accessibility Review. Although it was not announced in this latest round of index review, whether South Korea will continue to be classified as an emerging markets country could be announced on June 24th. There was also no announcement regarding China A-share inclusion For the further inclusion of China A-shares to go forward, the foreign ownership limit of 30% is apt to be problematic. For South Korea to be upgraded to developed from emerging markets, the lack of an offshore currency forward and the implementation of a short-selling ban last year will be problematic.

Monday is a market holiday in both Hong Kong and Mainland China.

H-Share Update

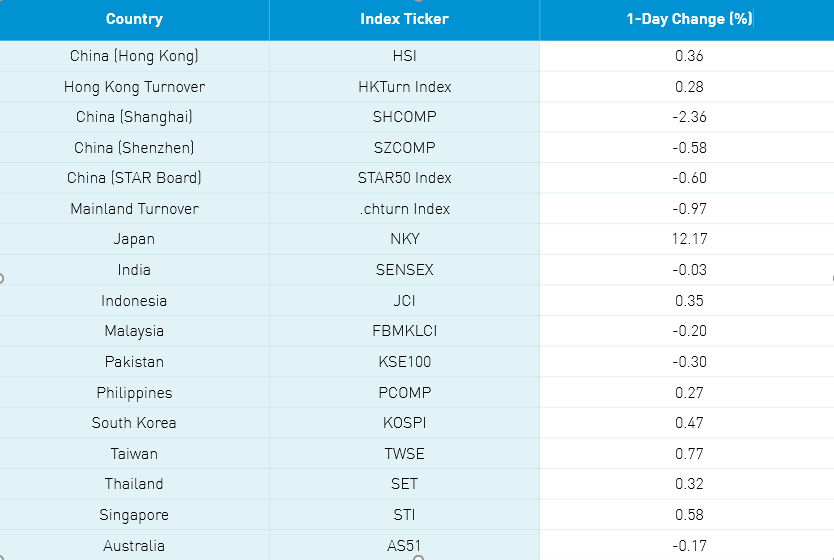

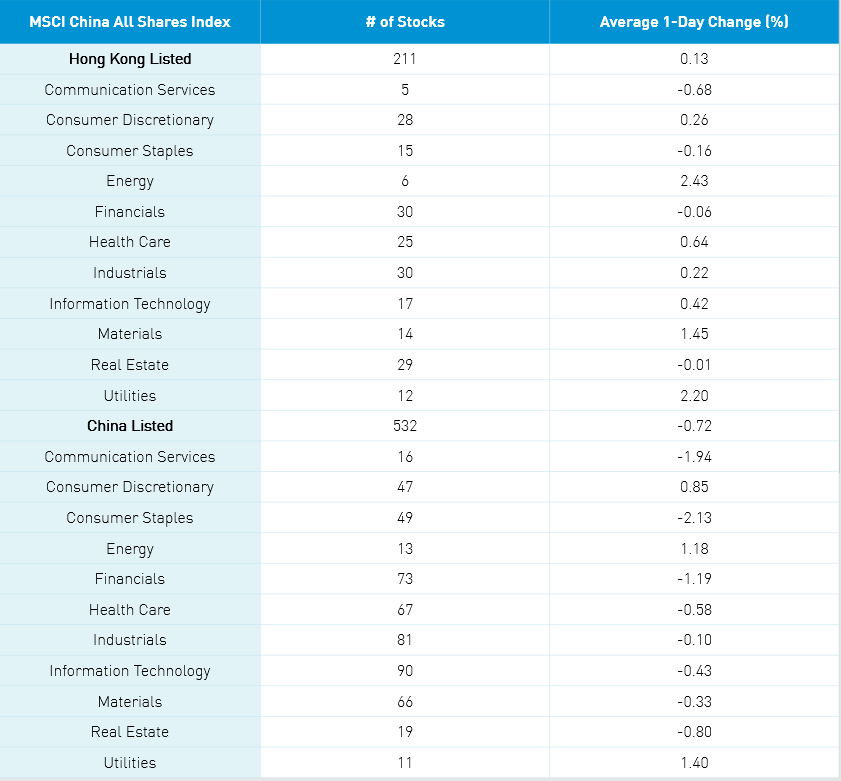

The Hang Seng Index and Hang Seng Tech Index gained +0.36% and +0.28%, respectively, as volume shrank -2.36% from yesterday, which is only 80% of the 1-year average. The 211 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index gained +0.13% led by energy +2.43%, utilities +2.2%, materials +1.44%, healthcare +0.63%, tech +0.42%, discretionary +0.26%, and industrials +0.21%. Meanwhile, communication -0.68%, staples -0.16%, and financials -0.16%. Hong Kong’s most heavily traded stocks by value were Tencent, which fell -0.75%, Meituan, which gained +3.09%, Alibaba HK, which fell -1.16%, BYD, which gained +1.13%, Xiaomi, which was flat, Ganfeng Lithium, which gained +4.59% following a private sale of stock, AIA, which was flat, Chinasoft, which fell -7.48%, energy stock CNOOC, which gained +1.33%, and Xinyi Solar, which gained +6.81%. Southbound Stock Connect volumes were moderate.

A-Share Update

Shanghai, Shenzhen, and the STAR Board were clipped by profit-taking off -0.58%, -0.6%, and -0.97%, respectively, as volume increased +12.17%, which is 122% of the 1-year average. There were 1,448 advancing stocks and 2,438 declining stocks. The 531 Mainland stocks within the MSCI China All Shares Index were off -0.72% with utilities +1.39%, energy +1.17%, and discretionary +0.84%. Meanwhile, staples -2.13%, communication -1.94%, financials -1.2%, real estate -0.81%, healthcare -0.58%, tech -0.44% and materials -0.34%. The Mainland’s most heavily traded stocks by value were Longi Green Energy, which gained +5.64%, BYD, which gained +6.03%, COSCO Shipping, which gained +3.4%, Jiangsu Hoperun Software, which gained +20%, CATL, which gained +3.99%, broker East Money, which gained +0.26%, Kweichow Moutai, which fell -2.67%, Sungrow Power, which gained +3.01%, Sany Heavy Industry -3.51% and Jiangsu Yanghe Brewery, which fell -10%. Northbound Stock Connect volumes were elevated as foreign investors sold -$474 million worth of Mainland stocks. CNY was basically flat, bonds were basically flat too, and copper was off -0.49%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 3.40 versus 3.39 yesterday

- CNY/EUR

- Yield on 1-Day Government Bond 1.50% versus 1.55% yesterday

- Yield on 10-Year Government Bond 3.13% versus 3.10% yesterday

- Yield on 10-Year China Development Bank Bond 3.54% versus 3.52% yesterday

- Copper Price -0.49%