Growth Rebound Goes Global, JD.com’s Annual 618 Sales Event Kicks Off, Week in Review

4 Min. Read Time

Week in Review

- Asian equities began the week mostly higher on Tuesday following the market holiday in China on Monday and G-7 meetings over the weekend. However, the bull market was tempered by the PBOC’s slight tightening through open market operations Tuesday.

- China’s retail sales rose +12.4% year-over-year in May versus 17.7% in April, according to a Wednesday economic release. The slowdown can be mostly attributed to a stronger base of May 2020 versus April 2020.

- In an attempt to quell the recent surge in commodity prices, China will release strategic reserves and a large lithium miner will increase production, according to Thursday reports. This may alleviate the pressure on input prices for China’s industrial firms.

- Vice Premier Liu He announced that he would be leading the effort to make China self-reliant in the semiconductor industry on Thursday. His announcement sent semiconductor names among other growth stocks higher in both Mainland China and Hong Kong.

Friday’s Key News

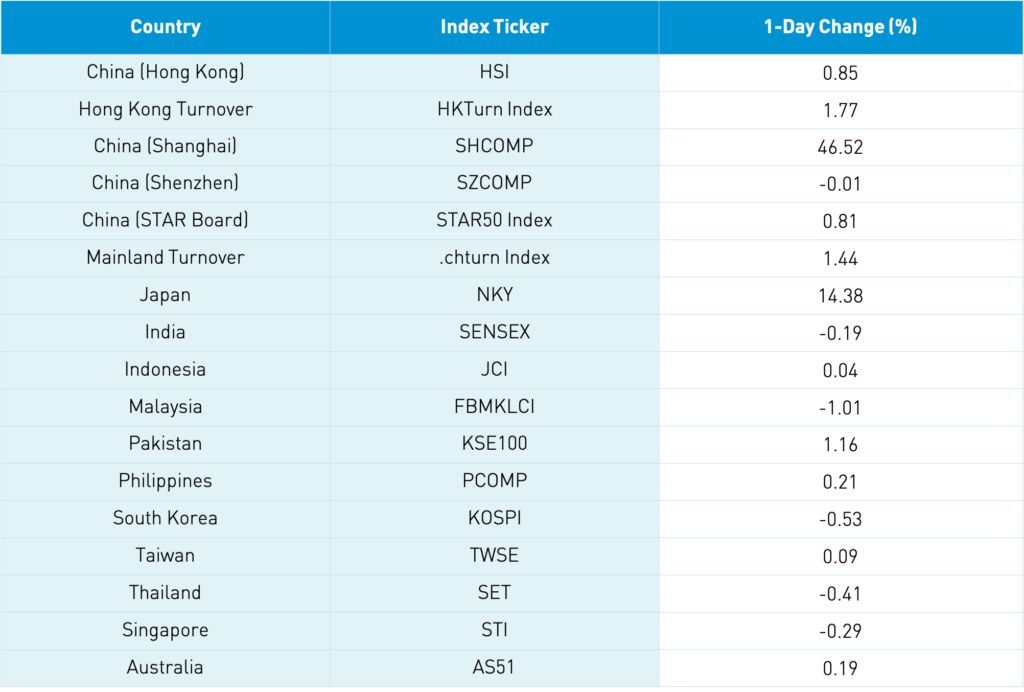

Asian equities were largely higher except for Japan, which was off. Today will be one of the largest trading days globally as both S&P Dow Jones and FTSE Russell indexes rebalance along with Quad Witching in the US (the expiration of stock and index futures and options). Asian volumes were up significantly as index providers dictate what passive managers buy and sell. Xiaomi was added back to FTSE indexes, gaining +1.77% as the most heavily traded stock in Hong Kong.

We saw significant outperformance in growth/tech today in both Hong Kong and China today as Shanghai (mega/large-cap value sectors) was down by -0.01% while Shenzhen (large/mid-cap growth sectors) was up +0.81% and the STAR Board (small-cap growth sectors) gained +1.44%. This was not limited to China as Hong Kong’s Hang Seng TECH Index gained +1.77% while the overall Hang Seng Index was up +0.85%, South Korea’s Kospi was up +0.09% versus the Kosdaq, which was up +1.21%.

Initial reports that JD.com and Alibaba's 618 (June 18th) sales events are going very well after selling a combined $136 billion worth of goods helped fuel the growth rally. 618 is JD.com’s response to Alibaba’s November Singles Day event. A strong 618 event should be good for Walmart, which owns 5.39% of the company and has historically promoted its goods on 618.

Hong Kong-listed sports and athletic apparel company Anta sports gained +6.18% after announcing that its net income may rise +110% in the first half of 2021, which led to several broker upgrades.

Value sectors were lower in China and Hong Kong as energy stocks were smashed. Kweichow Moutai was down -3.06%, which is a significant amount considering the lack of news about the company overnight.

There is chatter that the US FCC will ban Chinese-made security cameras, which, in theory, should have weighed on Hikvision though it gained +1.37%.

New Orient Education (EDU US) was dropped from FTSE Indexes, reminding me to always kick’em when they’re down as you’ll never get a better opportunity. Online education/tutoring stocks have been hammered by new regulations, though many brokers felt today could be the final flush as passive investors benchmarked to FTSE kick the stocks to the curb at today’s close. I agree with their thesis.

There has been chatter about China removing all birth restrictions, but the real issue is having children when you live in a city, which is expensive.

Former PCAOB head William Duhnke is being investigated by the SEC after being removed from his position. Why are we talking about this? Because Duhnke refused to discuss US-listed Chinese companies’ audits with his Chinese counterparts despite several olive branches from the latter. His replacement could, at a minimum, meet or speak with his Chinese counterparts, which could resolve the issue.

China’s first REITs will start trading on Monday.

The Financial Times is reporting that Indian mobile payment company Paytm is planning an IPO that would value the company at $29 billion.

H-Share Update

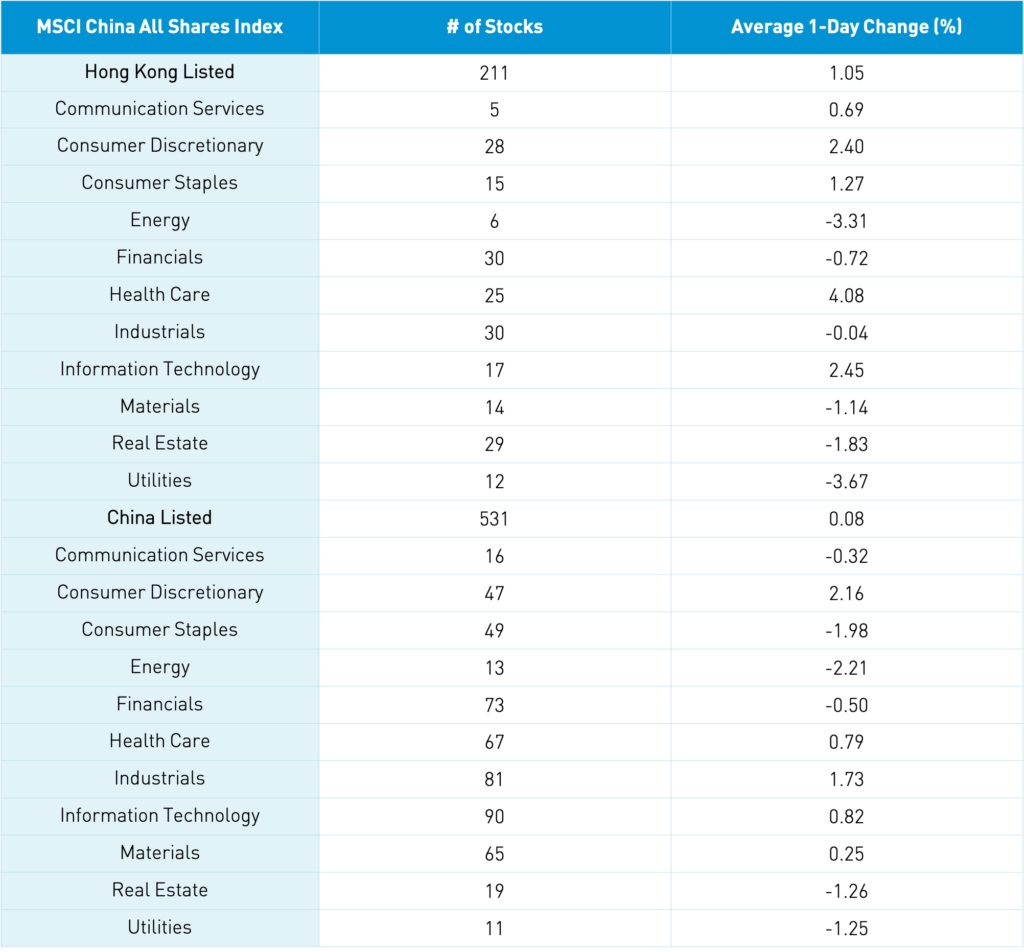

The Hang Seng Index and Hang Seng TECH Index opened higher and stayed there gaining +0.85% and +1.77%, respectively, as volumes increased +46% from yesterday, which is 125% of the 1-year average. The 211 Chinese companies within the MSCI China All Shares Index gained +1.05% led by healthcare +4.07%, tech +2.44%, discretionary +2.39%, staples +1.26%, and communication +0.69%. Meanwhile, utilities -3.68%, energy -3.32%, real estate-1.83%, materials -1.14%, and financials -0.73%. Hong Kong’s most heavily traded stocks by value were Xiaomi, which gained +1.77%, Tencent, which gained +0.67%, Alibaba HK, which gained +1.57%, Meituan, which gained +3.66%, BYD, which gained +4.22%, Geely Auto, which gained +5.26%, Wuxi Biologics, which gained +9.35%, Ping An Insurance, which fell -1.65%, Sunny Optical, which gained +6.92%, and Anta Sports, which gained +6.41%. Southbound Stock Connect volumes were moderate/high as Mainland investors bought approximately $154 million worth of Hong Kong stocks today.

A-Share Update

Shanghai, Shenzhen, and the STAR Board diverged -0.01%, +0.81%, and +1.44%, respectively, as volume increased +14% from yesterday, which is 111% of the 1-year average. The 531 Mainland stocks within the MSCI China All Shares Index were flat led by discretionary +2.07%, industrials +1.64%, tech +0.73%, healthcare +0.69%, and materials +0.16%. Meanwhile, energy -2.3%, staples -2.07%, real estate -1.35%, Utilities -1.34%, and financials -0.59%. The Mainland’s most heavily traded stocks by value were BYD, which gained +5.56%, Kweichow Moutai, which fell -3.06%, COSCO Shipping, which gained +1.62%, BOE Tech, which gained +3.96%, Longi Green Energy, which gained +3.81%, CATL, which gained +3.56%, broker East Money, which gained +1.92%, Will Semiconductor, which fell -7.83%, Sana Optoelectronic, which gained +3.29%, and Gigadevice Semiconductor, which gained +6.18%. Northbound Stock Connect volumes were moderate/high as foreign investors sold -$161 million worth of Mainland stocks.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.45 versus 6.45 yesterday

- CNY/EUR 7.65 versus 7.69 yesterday

- Yield on 1-Day Government Bond 1.51% versus 1.55% yesterday

- Yield on 10-Year Government Bond 3.14% versus 3.13% yesterday

- Yield on 10-Year China Development Bank Bond 3.52% versus 3.54% yesterday

- Copper Price -1.81%